Are you looking for ways to protect your hard-earned savings from hefty inheritance taxes? Inheritance tax can be a significant financial burden on your loved ones after you’re gone. But fear not! With the right strategies and planning, you can minimize or even eliminate this tax liability.

Join us as we explore smart tactics and tools to safeguard your wealth through gift/inheritance tax savings plans in Ireland. Let’s dive in and secure a brighter financial future for generations to come!

What is Inheritance Tax?

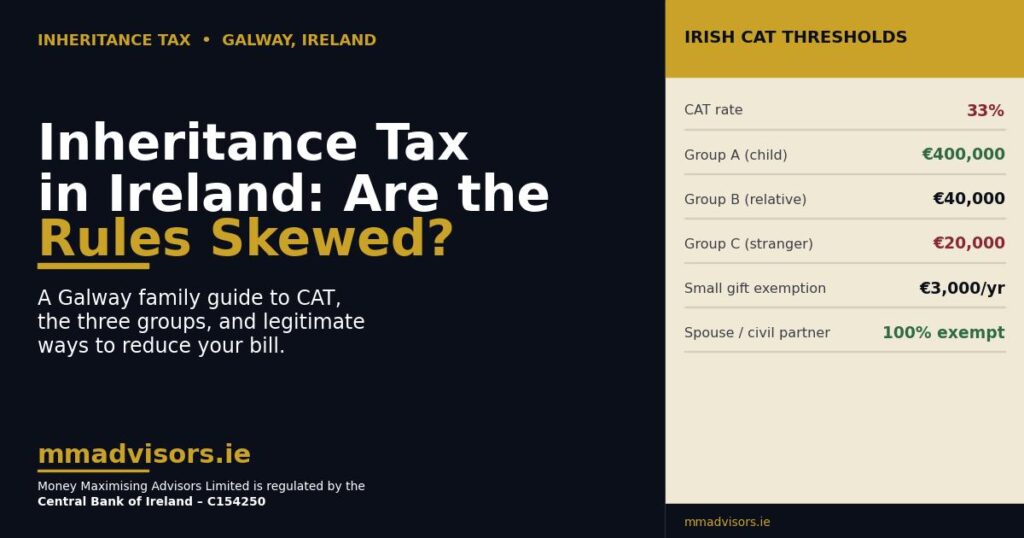

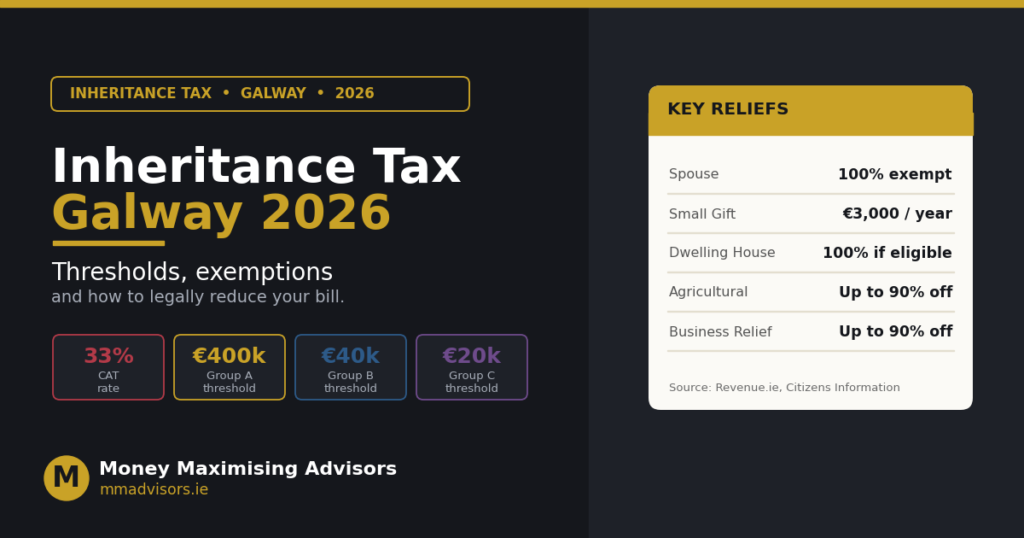

Inheritance tax, also known as estate tax or death duty, is a levy imposed on the assets transferred from a deceased person to their beneficiaries. Different countries have varying thresholds and rates for this tax. In Ireland, inheritance tax is charged on the value of an individual’s estate above a certain threshold upon their passing.

The main purpose of inheritance tax is to generate revenue for the government and prevent wealth accumulation across generations without contributing to society. It aims to promote fairness by ensuring that those inheriting significant assets contribute their fair share to the public coffers.

Many individuals seek ways to minimise their exposure to inheritance tax through strategic planning and financial manoeuvres. By understanding how this tax works and exploring legal avenues for savings, you can protect your wealth and ensure a smoother transfer of assets to your loved ones in the future.

Gift Tax vs. Inheritance Tax

When it comes to estate planning, understanding the difference between gift tax and inheritance tax is crucial. Gift tax is a tax on the transfer of assets during one’s lifetime, while inheritance tax applies to assets transferred after death.

Gift tax typically involves making large gifts above a certain threshold, which may be subject to taxation. In contrast, inheritance tax is imposed on the total value of an individual’s estate upon their passing.

Strategically gifting assets before death can help minimise potential inheritance taxes for your beneficiaries. By taking advantage of annual gift exclusion limits and lifetime exemptions, you can reduce the overall taxable amount passed down.

It’s essential to consult with financial advisors or legal professionals like Money Maximising Advisors Limited who specialise in estate planning to determine the most effective strategies for managing both gift and inheritance taxes.

Strategies to Avoid Inheritance Tax on Savings

One effective strategy to avoid inheritance tax on your savings is to set up a trust fund. By transferring your assets into a trust, you can ensure that they are not subject to inheritance tax upon your passing. Trusts offer flexibility and control over how your wealth is distributed to beneficiaries.

Another way to minimise inheritance tax is by gifting assets before death. By giving away assets during your lifetime, you can reduce the overall value of your estate that is subject to taxation. Be mindful of gift tax implications and seek advice from financial experts to navigate this process effectively.

Consider making charitable donations as part of your estate planning strategy. Donating to charity not only benefits causes you care about but also reduces the taxable value of your estate. It’s a meaningful way to leave a legacy while potentially lowering the burden of inheritance tax for your loved ones.

Explore these strategies with professional guidance tailored to your specific financial situation and goals for maximising savings and minimising tax liabilities associated with inheritance.

Setting Up a Trust Fund

Setting up a trust fund can be a strategic way to safeguard your assets and minimise inheritance tax liabilities. By establishing a trust, you transfer ownership of your assets to the trust itself, rather than leaving them directly in your estate. This means that when you pass away, those assets are not subject to inheritance tax because they technically no longer belong to you.

One benefit of setting up a trust fund is the ability to dictate how and when your beneficiaries receive their inheritances. You can outline specific conditions or timelines for distributions, ensuring that your wealth is managed according to your wishes even after you’re gone.

Trust funds also offer privacy advantages since they typically do not go through probate like traditional wills. This means that details of the trust arrangement remain confidential and are not part of the public record.

Moreover, trusts can provide protection against creditors or legal claims since the assets within the trust are considered separate from personal ownership. This additional layer of security can offer peace of mind knowing that your hard-earned savings are shielded from unforeseen circumstances.

Gifting Assets Before Death

When it comes to avoiding inheritance tax on your savings, gifting assets before death can be a strategic move. By transferring assets to your loved ones while you’re still alive, you can reduce the value of your estate and potentially lower the tax liability for your beneficiaries.

One way to do this is by utilising the annual gift allowance – in Ireland, each individual can gift up to a certain amount annually without incurring gift tax. This can be a tax-efficient way to pass on wealth while you are still around to see its impact.

Another option is making use of small gifts exemptions which allow for smaller gifts under a specified threshold without triggering any tax implications. It’s essential to plan these transfers carefully and consider seeking advice from financial experts or legal professionals specialised in inheritance tax matters.

By gifting assets before death, you not only have the opportunity to support your loved ones financially but also potentially reduce the burden of inheritance taxes they may face down the line.

Charitable Donations

When it comes to avoiding inheritance tax on your savings, charitable donations can be a valuable strategy. By leaving a portion of your estate to charity in your will, you can not only support causes that are important to you but also reduce the overall value of your estate subject to inheritance tax.

Charitable donations are exempt from inheritance tax, so by including them in your estate planning, you can effectively lower the taxable value of your assets. This means more of your hard-earned money goes towards making a positive impact through charitable organisations rather than being paid out in taxes.

In addition to reducing the burden of inheritance tax on your beneficiaries, making charitable donations allows you to leave behind a lasting legacy that reflects your values and beliefs.

Whether you choose to support education, healthcare, environmental conservation, or any other cause close to your heart, charitable giving is a meaningful way to make a difference even after you’re gone.

FAQs About Inheritance Tax

Can I completely avoid paying inheritance tax on my savings?

While it’s not always possible to entirely avoid inheritance tax, there are strategies available to minimise the impact and potentially reduce the amount owed.

Is setting up a trust fund a viable option for saving on inheritance tax?

Setting up a trust fund can be an effective way to protect your assets from hefty taxation. However, it’s essential to seek professional advice to ensure it aligns with your overall financial goals.

Are charitable donations a reliable method for reducing inheritance tax liability?

Yes, making charitable donations can not only benefit worthy causes but also help lower your inheritance tax bill by utilising exemptions and reliefs available.

Conclusion

Planning ahead and implementing effective strategies can help you avoid inheritance tax on your savings. By setting up a trust fund, gifting assets before death, or making charitable donations, you can minimise the impact of inheritance tax and ensure that more of your hard-earned money goes to your loved ones.

It’s essential to seek advice from financial experts like Money Maximising Advisors Limited in Ireland to navigate the complexities of gift and inheritance tax laws and make the most of available savings plans.

With careful planning and professional guidance from Money Maximising Advisors Limited, you can protect your wealth for future generations and leave a lasting legacy.

Talk to us at +353 91 393 125

Mail us at office@mmadvisors.ie

Visit our office at Unit 3, Office 6, Liosban Business Park, Tuam Rd, Galway, Ireland

Related Terms- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?