If you are planning to buy in Galway in 2026 city, county or the surrounding commuter belt, the national housing data tells you almost everything you need to know about the market you are about to enter. The story is one of resilient demand, very tight supply and steadier (but still rising) prices. At Money Maximising Advisors, we work with first-time buyers, movers and trader-uppers across Galway every week. This pillar guide pulls together the ten statistics we think every Galway buyer should have memorised before they sign anything, with practical advice on what each one means for your purchase.

| This article sits within our Mortgages hub and supports the pages our Galway buyers visit most, including Mortgage Comparison Advice, Public Sector Mortgages, Irish Ex-pat Mortgages and Buy-to-let Mortgages. |

Who is actually buying homes in Ireland in 2026?

The first thing worth understanding is the makeup of today’s buyer pool. First-time buyers are firmly in the driving seat, while existing homeowners looking to trade up or down are largely sitting on their hands. The shortage of “mover” mortgage products is one reason the market feels slower than the headline price growth suggests something we see clearly when we map a Galway household’s options through our Mortgage Comparison Advice process.

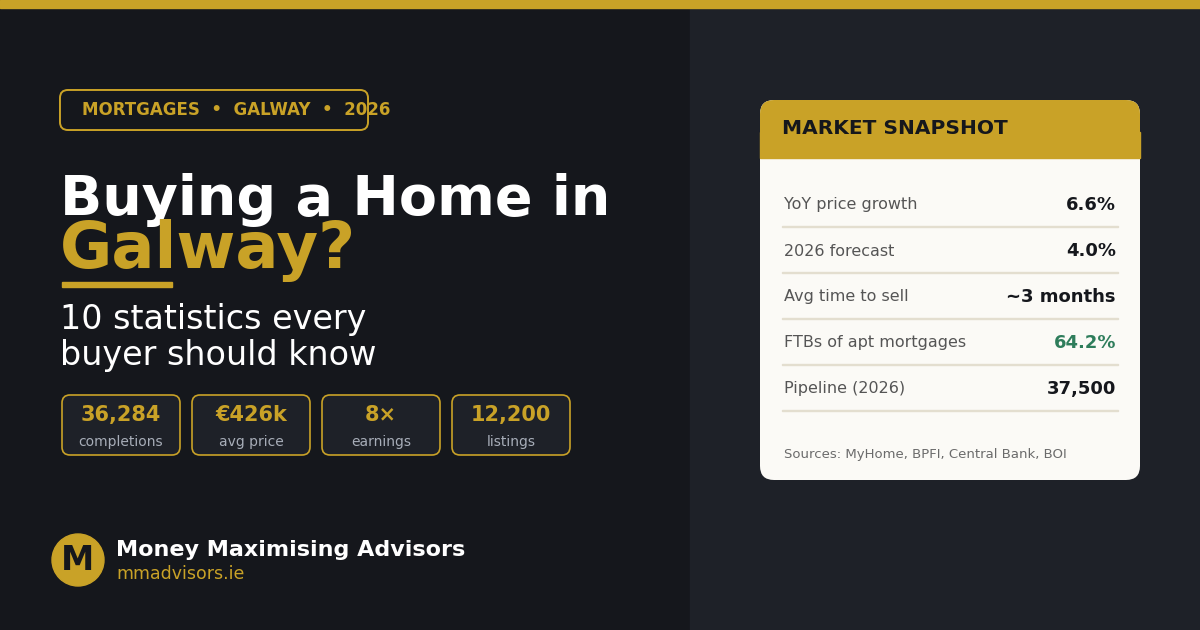

- Completions hit 36,284 in 2025 — the highest level since 2009.

Last year delivered the strongest building output the country has seen in well over a decade. For a Galway buyer that means more new-build options coming on stream than at any point in your adult life, although as you will see further down, supply still trails demand. New-build remains particularly attractive if you qualify for the Help to Buy scheme or the First Home Scheme.

- Apartment completions grew by roughly 40% year-on-year.

Apartment delivery has been the engine of that growth, with completions up approximately 40% on the previous year. In Galway, that pattern is most visible in the city and along the Salthill–Knocknacarra corridor, where higher-density schemes are reshaping the entry-level market. If a house has felt out of reach, a well-located A-rated apartment is increasingly a credible first step.

- Sole first-time buyers took out 64.2% of apartment mortgages in the year to June.

Almost two thirds of apartment loans in the most recent 12-month window were issued to sole first-time buyers, a single applicant, not a couple. That tells you exactly who the apartment market is for right now, and why competition for one-bed and two-bed units in Galway city remains intense. If you are buying solo, Mortgage Protection and Income Protection become especially important to lock in early.

- 37,500 new homes are forecast for 2026 — still not enough.

The pipeline points to another modest increase in delivery this year, but Ireland’s structural housing deficit means it is still well short of underlying demand. The practical translation: even with more new-build coming, you should expect competition on any half-decent property in Galway to remain firm through the year.

What buyers are paying — and what lenders will let you borrow

- The average Irish home cost €426,000 in 2025.

The headline national average has climbed to €426,000. Galway prices vary widely across the county, a three-bed semi in Knocknacarra, Renmore or Oranmore will pull noticeably above the national average the same house further out in east or north Galway can sit below it. Either way, this number sets the tone for what lenders are seeing across their books and how cautious they are likely to be.

- That price is now around 8× average earnings.

Average national home price vs average earnings — the affordability ratio Galway buyers are working against.

With average earnings sitting near €53,000, that puts the typical home at roughly eight times what the average person earns. The headline mortgage rule of thumb, borrowing up to four times income for a first-time buyer — explains why deposit size, second-income contribution and parental gifts have become so important to actually getting deals over the line. If a gift is on the table, talk to us about the wider planning angle too, including Small Gift Exemption Savings Plan and Inheritance Tax Advice.

- Fewer buyers are stretching beyond the 4× income lending limit.

Since 2023, the reliance on lending exceptions, those rare cases where banks lend above the standard four-times-income cap for first-time buyers, has fallen. In practical terms, more borrowers are now being approved cleanly within the standard limits rather than relying on the bank’s annual quota of exceptions. The flip side is that you cannot expect an exception to bail you out: get the numbers to work inside the rules from day one. Our Money Management Advice team can help you tidy up the run-in to your application.

Price inflation and supply: what the next twelve months look like

- Prices rose 6.6% year-on-year, with around 4% growth forecast for 2026.

Annual house-price inflation came in at 6.6%, and the consensus expectation is for that to ease to about 4% through 2026. “Easing” is the operative word prices are still expected to rise, just at a slower pace. For a Galway buyer that argues against trying to time the market: waiting six months is unlikely to make a property cheaper, but it could push it further out of reach if rates tick higher again. We model the trade-off between fixing and remaining variable in our blog Fixed or Variable Rate Mortgage: Which One Is Right for You?.

- Only 12,200 homes are currently listed on MyHome, well below pre-Covid levels.

New-build is rising, but the active resale stock remains historically tight.

The country-wide listing total has barely moved off historic lows, and new listings actually weakened in the final quarter of last year. In Galway, this is felt most sharply in the suburban resale market: family homes in the most sought-after estates can come and go before a viewing schedule is even published. The implications are practical, have your Approval in Principle in place before you start booking viewings, not after.

- Homes sell in roughly three months — and transaction volumes are flat.

Where stock does come to market, it does not hang around. The average sale-agreed to closing window sits at about three months, which is fast by any measure. At the same time, total transaction volumes in 2025 were barely above 2024, a clear signal that activity is being throttled by what is for sale, not by buyer appetite. For a Galway buyer, the lesson is simple: be ready to move quickly when something good appears.

What this all means for a Galway buyer in 2026

Stitch the ten statistics together and a coherent picture emerges. New-build supply is the highest it has been in fifteen years, but it remains short of the demand line. Prices are still rising but no longer at the breakneck pace of recent years. Lenders are being more disciplined inside the standard income rules. And the resale market continues to clear quickly because there simply is not enough of it.

For a Galway buyer, three things follow. First, preparation matters more than ever — your file should be tidy, your deposit sized properly, and your mortgage approval live before you fall in love with a property. Second, flexibility on property type and area widens your options significantly: an A-rated apartment in the city or a new build in Athenry or Tuam can outperform a tired older home in a popular suburb on both price and energy cost. Third, get protection in place early, most lenders expect Mortgage Protection, and depending on your job, products such as Public Sector Salary Protection or Serious Illness Cover are worth considering at the same time.

| Buying in Galway and not sure where to start? Book Now for a free consultation, or Enquire Now and one of our advisors will be in touch within one working day. |

Common mistakes Galway buyers should avoid

The patterns we see most often when a deal falls apart late in the process:

- Viewing before getting Approval in Principle. In a market this tight, you forfeit any chance of moving quickly on a property you love.

- Underestimating closing costs. Stamp duty, legal fees, valuation and survey costs typically add 2–3% on top of the purchase price.

- Ignoring the BER rating. It affects both your monthly running costs and your eligibility for a green mortgage rate.

- Stretching to the absolute borrowing maximum. Leaving headroom for rate movements is more important than ever as fixed periods roll off.

- Leaving life cover until the last minute. Lenders insist on it at drawdown; arranging it under pressure rarely produces the best policy.

Most-read mortgage guides

If you found this useful, these are the most-read guides we send to Galway buyers:

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

- Help to Buy Scheme Ireland 2026: Complete Eligibility Guide

- Fixed or Variable Rate Mortgage: Which One Is Right for You?

- First Time Buyer Mortgages: How Much Can First Time Buyers Borrow in Ireland?

- 10 Things to Know Before Applying for a Mortgage in Ireland

- How to Choose the Best Mortgage Lender in Ireland

Explore our full range

This guide is part of our wider Mortgages hub. You can also explore our Pensions, Protection, Public Sector, Savings & Investments and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- First Time Mortgage Buyers in Galway: Inflation and Its Impact on Interest Rates

- Mortgage Broker in Dublin: How to Get My BER Certificate (2026 Guide)

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords

Frequently asked questions

How much can a first-time buyer borrow in Galway?

The standard Central Bank rules allow first-time buyers to borrow up to four times their gross income, with a 10% minimum deposit. A small number of exceptions above that ratio are available each year, but lenders are using them less than they used to. For a tailored estimate of your specific borrowing capacity, Book Now and we will model it across multiple lenders.

Are Galway prices rising as fast as the national average?

Galway broadly tracks national price inflation, with the urban centres typically running a fraction ahead of the average and rural areas slightly behind. The 6.6% national figure is a useful directional guide; your specific area, property type and BER rating will move you up or down from that headline.

Should I buy now or wait for prices to drop?

Forecasters expect price growth to slow to around 4% in 2026 rather than reverse. Combined with a very tight stock of available homes, the market consensus is that waiting is unlikely to produce a cheaper home, and could expose you to higher interest rates. The right question is usually “am I ready?”, not “is the market ready?”.

Do I need life insurance to get a mortgage?

Yes, lenders generally insist on Mortgage Protection being in place before drawdown. Joint applicants will typically need cover on a dual-life basis. We arrange both single-life and dual-life cover alongside any application.

Buying in Galway? Let’s talk.

Whether you are a first-time buyer, an Irish ex-pat moving home, or a public sector worker eligible for our Public Sector Mortgages, our team handles the full process end-to-end. Book Now for a free consultation, or visit Money Maximising Advisors to learn more about how we work.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: You may have to pay charges if you pay off a fixed-rate loan early. All statistics cited in this article relate to the Irish national housing market in 2025–2026 and are sourced from MyHome, BPFI, the Central Bank of Ireland and Bank of Ireland reporting. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. Lending criteria, terms and conditions apply. You should seek personalised advice from a Qualified Financial Advisor before making any financial decision.