If you are saving for your first home in Galway, the headlines around inflation and European Central Bank (ECB) rates can feel disconnected from the price tag on a three, bed in Knocknacarra or a terrace in the West End but the link is direct. Inflation shapes the rate the ECB sets; the ECB rate shapes what Irish lenders charge; and the rate on your loan determines what your mortgage will cost you every month for the next 25 or 30 years. At Money Maximising Advisors, we work with Galway first-time buyers every week. This pillar guide pulls the moving parts apart in plain English, explains where rates are right now, and shows what a small shift could mean for your repayments.

| Primary category: Mortgages

This article sits within our Mortgages hub and supports the cluster of pages Galway first-time buyers most often read, including our Mortgage Comparison Advice, Public Sector Mortgages, Irish Ex-pat Mortgages and Money Management Advice pages. |

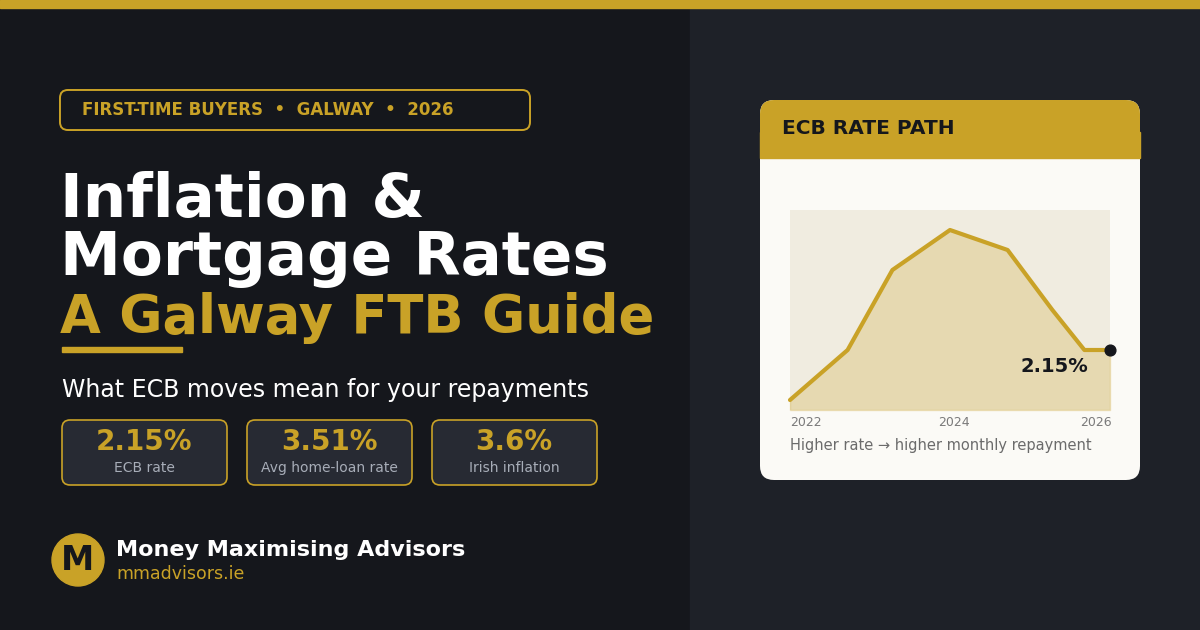

The ECB main refinancing rate climbed sharply in 2022–2024 and has settled at 2.15% since mid-2025.

How inflation drives the rate on your mortgage

Inflation — the rate at which prices are rising — is the single biggest variable the ECB watches when setting interest rates. The ECB has a clear mandate: keep euro area inflation close to 2% over the medium term. When inflation drifts meaningfully above target, the ECB has one main tool to cool things down: raising the cost of borrowing. When inflation undershoots, it can lower rates again. That is exactly the cycle we have lived through since 2022.

From early 2022 through to mid-2024, eurozone inflation surged well above target and the ECB responded with a sustained series of hikes, taking the main refinancing rate to its peak around the middle of 2024. As price growth eased, cuts followed, and the rate has held at 2.15% since mid-2025. For Irish borrowers the path is more than just a chart — every move at Frankfurt level eventually filters into the rates on offer at AIB, Bank of Ireland, PTSB and the non-bank lenders.

Where eurozone and Irish inflation stand in 2026

After hitting the ECB’s 2% target in December 2025, eurozone inflation has been bumpy in early 2026: 1.7% in January, 1.9% in February and 2.6% by end March according to Eurostat. The reacceleration has been driven in part by geopolitical pressure the Iran conflict has pushed up energy prices and disturbed global supply chains — with effects that are unlikely to fade overnight even if the underlying disruption settles.

Ireland’s number sits higher still. Annual Irish inflation is currently around 3.6%, placing us among the higher inflation economies in the eurozone. Many analysts expect the ECB to weigh up another rate move at its meetings around late April and into the summer (June and July are both on the radar). For a Galway first-time buyer about to draw down a 30-year loan, the direction of travel matters more than today’s headline number.

Why this matters more for Galway first-time buyers

Galway’s market has been one of the tighter ones outside Dublin for several years — strong jobs growth, a steady inflow of students and graduates, and limited new supply have all kept prices firm. For first-time buyers, that means tighter loan-to-income ratios, larger deposits and a longer wait between exchange and closing. A 0.25% or 0.50% move in rates lands harder on someone borrowing a higher multiple of their income.

Two State supports are worth lining up before you ever pick a rate. The Help to Buy scheme can refund up to €30,000 of income tax and DIRT toward your deposit on a new build, and the First Home Scheme can equity share part of the gap between your mortgage and the price of the property. Combined, they can take serious pressure off your monthly repayment from day one. Our Mortgage Comparison Advice service walks Galway FTBs through both and matches you to the lender best placed to approve you.

Fixed, variable or split: what most Irish borrowers actually choose

Roughly two-thirds of Irish mortgages by value are on a fixed rate, with only a small slice fixed beyond five years.

Looking across the value of all outstanding Irish mortgages, 66% are on a fixed rate and 34% on a variable rate — either a tracker (mostly legacy products) or a standard variable, with some SVRs still running as high as 5.15%. What is striking is that of the fixed-rate book, only around 9% is fixed for longer than five years. Irish borrowers, in other words, lean heavily toward shorter-term fixes.

In an environment where the next ECB move could go either way, a fixed rate offers something valuable: certainty. You lock your monthly repayment for the agreed period and insulate the household budget from short-term turbulence. A variable rate keeps you exposed to changes in both directions — cheaper if cuts come, dearer if hikes do. Many of the FTBs we advise opt for a fixed rate of three to five years for exactly that reason, especially in the early years when the deposit savings buffer is leaner.

Choosing between lenders matters as much as choosing between rate types. The gap between the cheapest and most expensive new mortgage rate on offer in Ireland currently stands at 1.95 percentage points — worth roughly €112 a month per €100,000 borrowed over a 30-year term. On a typical Galway first-time buyer mortgage, that is the difference between a comfortable budget and a constant squeeze.

The maths: what a 0.5% rate move feels like

Monthly repayment impact of a 0.5% rate rise across common mortgage sizes.

The Central Bank’s latest retail interest rate report puts the average new lending rate for house purchase at 3.51%. On that rate, every €100,000 you borrow over 30 years costs you roughly €450 a month. If your rate rises by 0.5 percentage points to 4.01%, those repayments climb by about €28 a month for every €100,000.

Apply that to the average new home loan drawn down in 2025 — around €350,000 — and a half-point increase translates to roughly €98 extra each month, or close to €1,200 a year. Over a full 30-year term, that single rate move costs the household around €35,000 in additional interest. Locking in the right rate, with the right lender, on the right term is genuinely a four or five figure decision for a Galway FTB.

| Buying your first home in Galway? Book Now for a no-obligation consultation, or Enquire Now and a member of our team will be in touch to walk you through your options. |

Smart moves for first-time buyers in Galway

A few practical steps tip the odds in your favour, whatever direction rates take next:

- Treat your deposit as a target with a date. Use a structured plan; our advisors model monthly saving against typical Galway property prices.

- Get Approval in Principle (AIP) early. It tells you exactly what you can offer on, and it shortens the chain when the right property appears.

- Compare on the All In Cost. Headline rate, cashback, term, conditions and exit fees — a 0.20% difference can be eaten by a poor structure.

- Stress test your repayment. If a 0.5% rise would derail you, choose a longer fix or a smaller loan now.

- Put protection in place. Mortgage protection is required at drawdown; income protection and serious illness cover are smart to layer in.

On that last point, every Irish mortgage needs Mortgage Protection before drawdown. Many Galway FTBs also add Income Protection and Serious Illness Cover so a job loss or major illness does not turn a manageable repayment into a crisis.

Common mistakes to avoid

- Chasing the lowest sticker rate. A two-year fix at a knockout rate can roll onto a far worse standard variable; check the rollover terms before signing.

- Underestimating soft costs. Legal fees, stamp duty, valuation, surveyor and protection premiums all need to be on your spreadsheet.

- Ignoring the BER rating. A B3 or higher property typically unlocks a green rate, often 0.10–0.30 pp lower than the standard product.

- Going it alone with non-bank lenders. Non-bank funders rely on wholesale funding, which moves more closely with ECB rates than traditional deposit-funded banks. Understand the difference.

- Forgetting your future self. Your career, your family plans and even your move from Galway to elsewhere all matter — build flexibility into the term you choose.

Most-read mortgage guides

Reading next? These pillar and cluster pages have been the most popular with Irish home buyers and switchers:

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

- Fixed or Variable Rate Mortgage: Which One Is Right for You?

- Help to Buy Scheme Ireland: Complete Eligibility Guide

- First Time Buyer Mortgages for Public Sector Workers: A Complete Guide

- How to Choose the Best Mortgage Lender in Ireland

- Tips on How to Calculate Mortgage Repayments in Ireland

Explore our full range

This guide is part of our wider Mortgages hub. You can also explore our Pensions, Protection, Public Sector, Savings & Investments and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords

- Effective Mortgage Repayment Hacks to Clear Debt Faster

- Is It Worth Switching to a Fixed-Rate Mortgage?

- 10 Things to Know Before Applying for a Mortgage in Ireland

- How to Remortgage to Release Equity from Your Property

Frequently asked questions

Is the ECB going to raise rates again in 2026?

No one can call it with certainty. With Irish inflation running near 3.6% and eurozone inflation back above target by end March, another move is plausible at the ECB’s April, June or July meetings. Plan as if a move could happen — hope it does not.

Should I fix my rate as a first-time buyer in Galway?

For most Galway FTBs, a three to five year fixed rate strikes a sensible balance between certainty and flexibility. The right answer depends on your loan size, term and life plans — a quick call with our Mortgage Comparison Advice team will model the options against your numbers.

How much could a 0.5% rate rise add to my repayments?

Roughly €28 a month for every €100,000 borrowed over 30 years. On the average new mortgage drawn in 2025 of around €350,000, that is about €98 extra per month — or close to €1,200 a year.

Will non-bank lenders pass on every ECB move?

Non-bank lenders rely on wholesale funding rather than customer deposits, so their cost of funds tracks market rates more directly. As a rule, ECB moves tend to flow through to non-bank mortgage rates faster than to traditional bank rates.

Are there schemes that help reduce the impact of high rates?

Yes — the Help to Buy scheme can refund up to €30,000 of income tax and DIRT toward your deposit, and the First Home Scheme can shrink the size of the mortgage you actually need. Both directly reduce how much rate exposure you carry. Enquire Now and we will check what you qualify for.

Ready to take the next step?

Whether you are saving your deposit, weighing up Help to Buy, or already at AIP stage and shopping for the right lender, our team handles the application from start to finish for first-time buyers across Galway, Mayo, Roscommon and beyond. Book Now for a free consultation, or visit Money Maximising Advisors to learn more. Plain English explainers on rates and the Irish mortgage market are also available on our YouTube channel.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: You may have to pay charges if you pay off a fixed-rate loan early.

Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. Inflation, interest rates and lender pricing change frequently — figures referenced in this article are accurate at the time of writing and may have moved since. This article is for general information only and does not constitute financial, tax or legal advice. Lending criteria, terms and conditions apply.