Are you self-employed and grappling with the complexities of retirement planning? You’re not alone. The journey to secure your financial future can feel overwhelming, especially when tax liabilities come into play. But what if I told you that pensions could be your secret weapon for reducing those pesky taxes while building a solid nest egg?

Pensions for the self-employed offer a powerful way to enhance your savings while also reaping significant tax benefits. Whether you’re freelancing, running a small business, or consulting, understanding how to leverage pension contributions can transform the way you think about both retirement and tax efficiency.

Let’s dive into the world of pensions tailored specifically for self-employed individuals and explore how they can help you navigate through tax relief opportunities effectively. Your financial future awaits!

Understanding Tax Liabilities for Self Employed Individuals

Self-employed individuals face unique tax obligations that can often feel overwhelming. Unlike traditional employees, they are responsible for both income and self-employment taxes. This means calculating what you owe on your earnings is entirely up to you.

Your net profit influences how much tax you’ll pay. It’s essential to keep meticulous records of all business expenses as these can be deducted from your taxable income. Deductions directly reduce the amount of money that is subject to taxation, making them incredibly valuable.

Additionally, understanding estimated taxes is crucial. As a self-employed person, you’re required to make quarterly payments based on expected annual income. Failing to do so might lead to penalties and interest charges later—an unwelcome surprise.

Recognizing these responsibilities early can pave the way for smarter financial decisions down the line. Knowledge truly empowers when it comes to managing your finances effectively in self-employment scenarios.

Benefits of Using Pensions to Reduce Tax Liabilities

Using pensions as a self-employed individual offers significant financial advantages. One of the most notable benefits is tax relief on pension contributions. This means that your contributions effectively reduce your taxable income, allowing you to keep more of what you earn.

The impact can be substantial, especially for those with fluctuating incomes. By contributing to a pension plan, you gain immediate tax savings while simultaneously saving for retirement.

Moreover, growing funds within a pension are typically free from capital gains and income taxes. This allows your investments to compound over time without additional tax burdens.

Choosing this route also demonstrates long-term planning. It signals to potential clients or partners that you’re committed not just to immediate profits but also to sustainable financial health in the future.

Leveraging pensions aligns well with strategic financial management and helps create a nest egg while minimizing current taxation pressures.

Types of Pension Plans Available for the Self Employed

When it comes to pensions for self-employed individuals, several plan options can suit different needs and preferences.

- One popular choice is the Solo 401(k). This plan allows you to contribute both as an employee and employer, maximizing your contributions while enjoying significant tax relief on pensions.

- Another option is a Simplified Employee Pension (SEP IRA). It’s straightforward and allows for higher contribution limits compared to traditional IRAs. This makes it ideal for those who want flexibility in their retirement savings.

- Then there are Individual Retirement Accounts (IRAs), which include both Traditional and Roth options. While Traditional IRAs offer immediate tax benefits, Roth IRAs provide tax-free withdrawals in retirement.

- Consider setting up a Defined Benefit Plan if you’re looking for guaranteed income later. Although more complex, they can yield substantial pension tax relief in Ireland or elsewhere based on your earnings.

How to Choose the Right Pension Plan for Your Business

Choosing the right pension plan is crucial for self-employed individuals.

- Start by assessing your financial goals and retirement needs. Consider how much you can afford to contribute regularly.

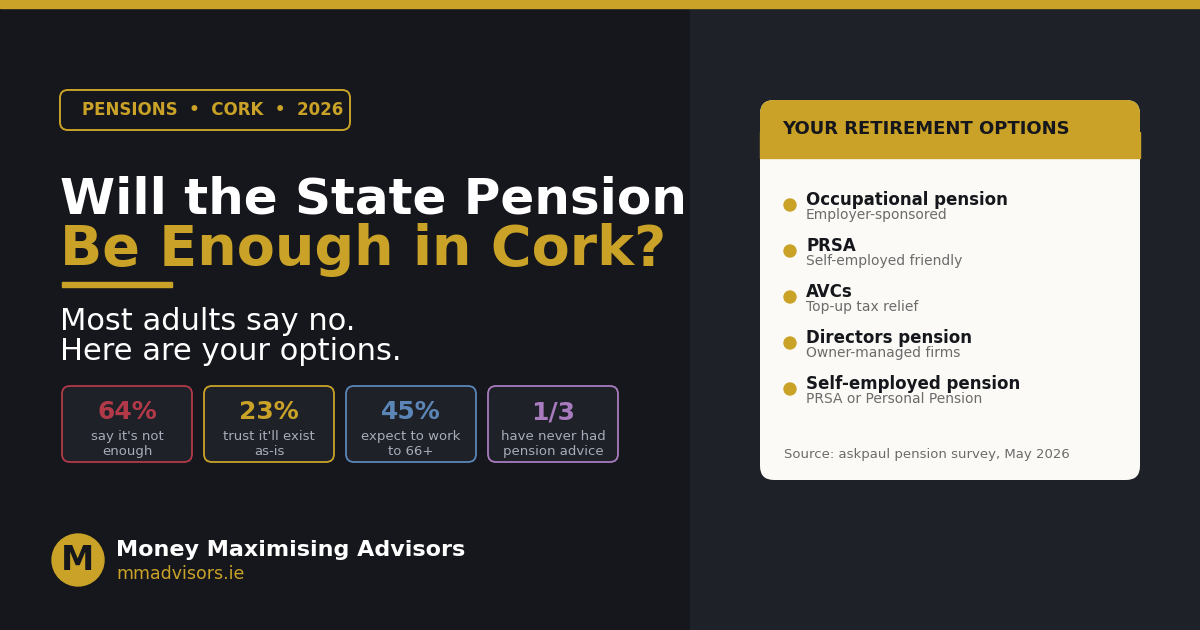

- Next, look into the different types of pension plans available. Each has unique features that may align with your business model or personal preferences. Options like a Personal Retirement Savings Account (PRSA) or a Self-Invested Personal Pension (SIPP) might suit varying risk appetites.

- Research providers carefully. Compare fees, investment options, and customer service reviews to find one that matches your expectations.

- Don’t hesitate to seek advice from experts in tax-efficient retirement planning for the self-employed—like Money Maximising Advisors—to better navigate complexities.

- Keep flexibility in mind. A plan that adapts as your income fluctuates will serve you better over time.

Steps to Setting Up a Pension Plan as a Self Employed Individual

Setting up a pension plan as a self-employed individual may seem daunting, but it can be straightforward.

- Start by assessing your financial goals. Determine how much you want to save for retirement and what kind of lifestyle you envision.

- Next, research different types of pension plans available for the self-employed. Options like Personal Retirement Savings Accounts (PRSAs) or Self-Invested Personal Pensions (SIPPs) might suit your needs.

- Once you’ve chosen a plan, gather necessary documents such as proof of income and identification. Contact providers to discuss terms and contributions.

- After selecting your provider, set up automatic contributions if possible. This makes saving easier and more consistent over time.

- Revisit your plan periodically to ensure it aligns with any changes in your business or personal circumstances. Keep track of tax relief on pensions that can help maximize savings while effectively.

Other Tax Reduction Strategies for the Self Employed

Self-employed individuals have various avenues for reducing tax liabilities beyond pensions. One effective strategy is to maximize allowable business expenses. This includes costs like office supplies, travel, and even a portion of your home if you work from there.

Another approach involves contributing to retirement savings accounts that offer tax benefits. Exploring options such as the Simplified Employee Pension (SEP) or Solo 401(k) can provide significant advantages while also enhancing long-term financial security.

Utilizing tax credits is another smart move. Certain expenditures related to research and development may qualify for deductions, lowering taxable income substantially.

Keeping meticulous records can pay off. Proper documentation ensures you claim every eligible expense without error when filing taxes, potentially saving you money down the line. Each of these strategies plays a critical role in maintaining a healthy financial outlook as a self-employed individual.

Conclusion

Pensions for self-employed individuals offer a strategic avenue to reduce tax liabilities while securing financial stability for the future. Understanding how pensions work and the associated tax relief can empower you as a self-employed professional.

The landscape of tax liabilities is complex, but leveraging pension contributions is an effective way to ease your financial burden. By investing in a suitable pension plan, you not only prepare for retirement but also benefit from reduced taxable income—an essential strategy in today’s economy.

Whether you’re considering a personal pension or setting up a more tailored solution like a Small Self-Administered Scheme (SSAS), there are various options available. It’s vital to choose the right plan that aligns with your business’s cash flow and long-term goals.

Setting up your pension might feel daunting, but breaking it down into manageable steps simplifies the process significantly. Additionally, exploring other tax reduction strategies can further enhance your financial position.

For those navigating this journey, seeking guidance from Money Maximising Advisors can provide personalized insights tailored to your unique circumstances and aspirations. Embracing these tools creates opportunities not just for today but lays down solid foundations for tomorrow’s success in both life and business management.

Talk to us at +353 91 393 125

Mail us at office@mmadvisors.ie

Book an appointment: Click here to Book now

Visit our office at Unit 3, Office 6, Liosban Business Park, Tuam Rd, Galway, Ireland