| ▶ WATCH THE 60-SECOND EXPLAINER In this 60-second reel we take two identical applicants, same €80,000 salary, same clean credit history, same deposit; and run them past five active Irish mortgage lenders. The result is a €50,000 swing between the lowest and highest offer. The reason is not luck. It’s how each lender chooses to weight your income, your bonuses and your overtime. Reel: https://www.instagram.com/reel/DaBhYeqzSzp/ |

| IN THIS ARTICLE Why identical applicants get different mortgage approvalsQuick answers to the six borrowing questions every FTB asksHow each Irish lender treats bonuses, commission and overtimeThe Central Bank rules that set the floor; and the ceilingHow a broker uses the differences to unlock €50k moreThe mistakes that quietly cost applicants approval |

Same salary. Same credit. Same deposit. Five lenders. A €50,000 gap between the smallest and biggest approval.

Most first-time buyers in Ireland assume that mortgage borrowing capacity is a fixed number, a function of income, deposit and the Central Bank’s loan-to-income cap; and that where you apply doesn’t much matter. It matters enormously. Working with the right Mortgage Broker Ireland homebuyers routinely see a €30,000 to €50,000 gap between the lowest-offering Mortgage Lender Ireland and the highest-offering lender for identical applicants. The gap comes from how each bank calculates Mortgage Affordability Ireland rules and, crucially, how each treats non-basic income (bonuses, commissions, overtime, rental income, benefits-in-kind). This guide explains exactly how Mortgage Borrowing Ireland capacity varies across the market and how to structure your Mortgage Application Ireland for the maximum result. Explore our mortgage comparison advice service or book an appointment today.

Quick answers: six borrowing questions every Irish homebuyer asks

Why do mortgage lenders offer different borrowing amounts?

Because each lender applies its own income treatment rules on top of the same Central Bank framework. Two lenders can both look at your €80,000 salary but reach very different lending decisions because Lender A counts 100% of your €15,000 bonus while Lender B counts only 50%. Combine that with variations in stress-test rates, treatment of overtime, and how they weight rental income or BIK, and you get sizable differences in approval.

How do lenders calculate mortgage affordability?

Every Irish lender must apply two overarching Central Bank rules:

(1) a loan-to-income (LTI) cap :- 4× income for first-time buyers as standard, with exceptions available up to 5× in limited numbers; and

(2) a loan-to-value (LTV) cap :- typically 90% LTV for first-time buyers. Within those two limits, lenders apply their own affordability stress test, typically the loan repayment at an assumed rate 2 percentage points above the offered rate.

What is the difference between gross income and net income?

Gross income is your total pay before tax, USC and PRSI. Net income is what actually lands in your account. Irish lenders quote LTI multiples against gross salary, but their internal affordability calculations use net take-home to check that the stress-tested repayment leaves you enough for other outgoings. Both numbers matter, but LTI gross-based, is what determines the headline borrowing figure.

Which income do mortgage lenders use?

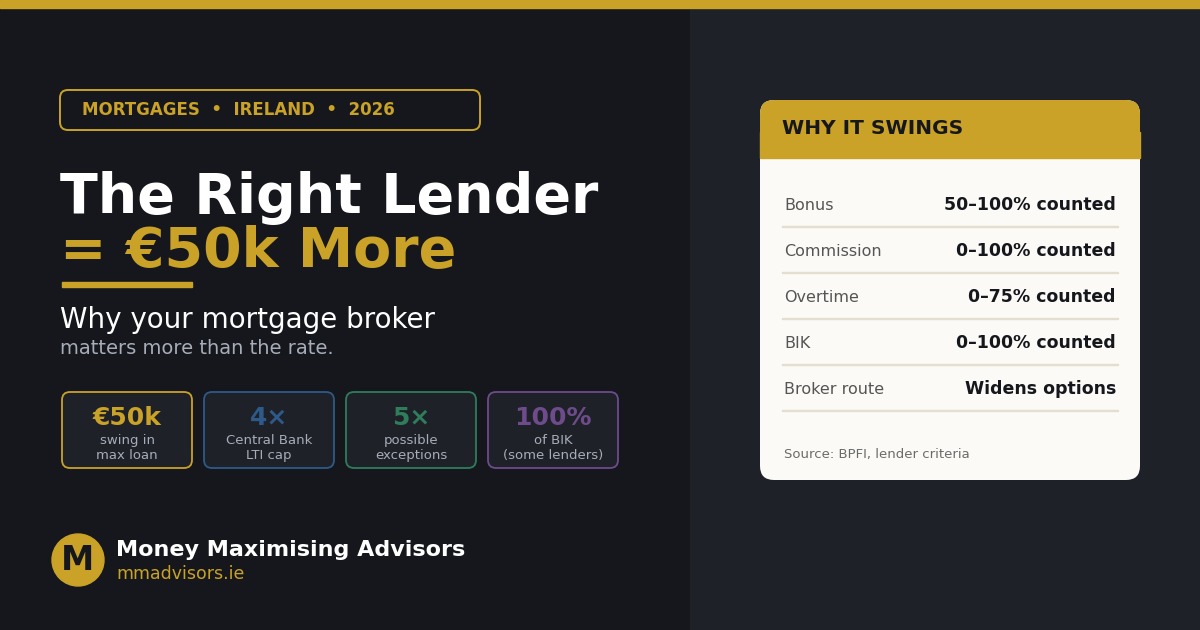

Basic salary is counted 100% by all lenders. Everything else varies: guaranteed bonuses are counted 50-100% depending on lender; discretionary bonuses 0-50%; commission 0-100%; overtime 0-75%; rental income 50-75%; BIK 0-100%. The specific treatment can shift borrowing by tens of thousands of euro. A broker who knows each lender’s current policy places you with the lender that treats your specific income mix most generously.

Can switching lenders increase my mortgage approval?

Yes — whether you’re a first-time buyer choosing between initial applications, a mover selling and buying, or a switcher moving an existing mortgage, the choice of lender materially changes the amount you can borrow. It also changes the rate you pay, the cashback available and the fixed-rate options you can access. Two decisions worth making with expert help.

Why do banks have different lending criteria?

Because each lender balances credit risk appetite, funding cost, product strategy and Central Bank exception allowances differently. A retail bank focused on volume may be more generous on straightforward salaried applicants; a specialist lender may lean into self-employed applicants or those with variable pay; a challenger bank may compete on rate or LTV. Understanding each lender’s current stance is what separates a good mortgage outcome from an average one.

Same applicant, five lenders — the €50,000 gap

Illustrative approvals for a single €80,000-salary applicant across five active Irish lenders in 2026.

The chart above shows what an €80,000-salary first-time buyer with a €10,000 guaranteed bonus and €5,000 overtime might be offered across five different lenders currently active in the Irish market. All five apply the same Central Bank 4× LTI base cap. All five see identical documentation. Yet the offers vary from around €320,000 at the strictest lender to close to €370,000 at the most generous a €50,000 swing on the same person.

The difference comes almost entirely from three variables:

- Bonus treatment. Lender A counts guaranteed bonuses at 50% (adds €5,000 to income), Lender E counts them at 100% (adds €10,000).

- Overtime treatment. Lender A ignores overtime entirely; Lender E counts 75% (adds €3,750).

- Central Bank exceptions. Some lenders reserve their 5× LTI exception allowance for strategic applicants; others release them earlier in the year.

How each type of income is treated

Seven income categories — and the range across which Irish lenders currently value each one.

Base salary

Universally counted at 100%. This is the single biggest driver of borrowing capacity for most applicants.

Guaranteed bonuses

A contractually guaranteed bonus, typically the bonus paid to all employees regardless of performance, and documented in the offer letter; is treated at 50-100% depending on lender. Two years of P60 evidence is usually required.

Discretionary bonuses and commission

The most variable category. Some lenders ignore discretionary pay entirely; others count up to 100% subject to a two- to three-year averaged track record. This is where the biggest lender-to-lender gaps open up for anyone in sales, tech or professional-services roles.

Overtime and shift premium

Regular overtime paid consistently over two years may be counted at 50-75%. Occasional overtime is often ignored. Critical income category for healthcare workers, Gardaí and shift-based public-sector applicants.

Rental income

Typically counted at 50-75% for existing rental properties, netted for a notional void allowance. Not usable at all if the property is jointly owned with a non-applicant or subject to arrears.

Benefits-in-kind (BIK)

Company car, medical insurance and share incentives may be counted at 0-100% depending on lender. Cash equivalent, taxable BIK is more likely to count than in-kind benefits.

Where to get advice — the Money Maximising Advisors group

| MONEY MAXIMISING ADVISORS GROUP — NATIONAL COVERAGEThe article you are reading is from mmadvisors.ie, the flagship of the Money Maximising Advisors group. Two sister brands now form part of the same Central Bank-regulated group and provide localised advice across Ireland • mmadvisors.ie — Money Maximising Advisors Limited (Tuam, Co Galway) — national coverage, HQ for the group. Full product range across mortgages, pensions, protection, savings, investments and inheritance tax. • jcfc.ie — Joe Coyle Financial Consultants (Mountcharles, Co Donegal) — North West Ireland specialists, with a particular focus on business-owner protection, pensions and succession advice. • moneysense.ie — Money Sense Financial Services (Killarney, Co Kerry) — South West Ireland family-run advisory, over four decades of experience across financial planning, mortgages, protection and retirement. |

Real-world scenario: a Dublin first-time buyer couple

| CASE STUDY: FIRST-TIME BUYERS, DUBLIN 15, JOINT INCOME €120,000 Emma (Software Engineer, €80k base + €12k guaranteed bonus + RSU vesting) and David (Nurse, €48k base + regular unsocial-hours premium of €6k) approach three high-street banks directly. Bank 1 offers €420,000 (counts bonus at 50%, ignores RSUs, counts unsocial-hours at 50%). Bank 2 offers €395,000 (stricter on RSUs and premium). Bank 3 offers €410,000. Working with a broker, they submit instead to a lender that counts guaranteed bonus at 100%, unsocial-hours premium at 75%, and vested RSUs at 60%; for a final approval of €465,000. Same couple, same P60s, €45,000 to €70,000 additional buying power, enough to move from a two-bed apartment to a three-bed semi. |

The Central Bank rules that set the floor — and the ceiling

The 4× loan-to-income (LTI) cap

First-time buyers can borrow up to 4× gross annual income as a starting cap. Second and subsequent buyers are limited to 3.5×. A worker earning €80,000 can therefore borrow €320,000 as a floor, the number goes up as lenders treat additional income favourably.

The 5× LTI exception

Each lender is allowed to grant a limited number of exceptions above 4× LTI in any calendar year — typically to 5× income for well-qualified first-time buyers with stable, growth-oriented income. Broker relationships with lenders often determine access to these allocations.

The 90% loan-to-value (LTV) cap for FTBs

First-time buyers can borrow up to 90% of the property value — requiring a 10% deposit. Second and subsequent buyers face a 20% deposit requirement (80% LTV) in most cases. Green mortgages on high-BER-rated properties sometimes access preferential terms.

Affordability stress testing

Every lender is required to stress-test your ability to make repayments at rates 2 percentage points above the offered rate. The stress test uses your net income and current outgoings — which is why lenders scrutinise your last three to six months of bank statements for regular commitments (car finance, personal loans, subscriptions, gambling activity).

| READY TO TALK TO A CENTRAL BANK-REGULATED ADVISOR?Wondering which of the eight active Irish mortgage lenders will maximise your borrowing on your specific income mix? Our mortgage team runs affordability models for every FTB, mover and switcher free. → Enquire Now | → Book an Appointment | → Contact Us |

Common mortgage application mistakes that quietly cost approval

- Applying to only one lender. Costs you the entire lender-to-lender range often €30,000 to €50,000 in borrowing capacity.

- Missing income evidence for variable pay. Two years of P60s and payslips showing the variable pay are usually required. One year is rarely enough.

- Untidy bank statements. Overdraft usage, gambling transactions, missed direct debits and unexplained large cash movements all hurt.

- Recent short-term debt. A personal loan taken out in the six months before application, particularly for the deposit, is a red flag. Plan the deposit build-up 12+ months in advance.

- Applying without pre-qualifying. A failed application shows up on future credit checks. Always model affordability first and choose the right lender before submitting.

Related reading

| Related post | Category | Read more |

|---|---|---|

| Mortgage Broker in Dublin: Switching Mortgage — How to Get My BER Certificate 2026 Guide | Mortgages | Read article |

| First Time Mortgage Buyers in Galway: Inflation and Its Impact on Interest Rates | Mortgages | Read article |

| 10 Things to Know Before Applying for a Mortgage in Ireland | Mortgages | Read article |

| Public Sector Mortgage Ireland: What Do I Need to Apply for a Mortgage? | Public Sector | Read article |

Frequently asked questions

Does using a mortgage broker cost me more?

In most Irish market cases, the broker is paid a commission by the lender for placing the loan there is no direct fee to you. The rate and terms you are offered are the same as if you had approached the lender directly. Any broker fee should be disclosed in writing before you engage under the Central Bank Consumer Protection Code.

How long does the mortgage application take?

Approval-in-principle takes 1-2 weeks with a well-packaged application. Full loan offer follows valuation and legal steps, typically 4-8 weeks from application to loan offer. Drawdown depends on the vendor and your solicitor add another 4-12 weeks.

Can self-employed applicants access the same LTI multiples?

Yes, but lenders require two to three years of certified accounts, and average the last two years’ profits (after tax add-backs) as “income.” The specific lender panel that engages well with self-employed applicants is different from the panel best for PAYE applicants broker guidance matters here.

About the author

| REVIEWED BY: MONEY MAXIMISING ADVISORS This guide is reviewed by advisors at Money Maximising Advisors Limited, a Qualified Financial Advisor firm regulated by the Central Bank of Ireland. Our team holds QFA, CFP®, RPA and Specialist Investment Adviser qualifications and works alongside our sister brands jcfc.ie (Donegal) and moneysense.ie (Kerry) to deliver advice across every county in Ireland. Every recommendation is documented in a written Statement of Suitability. |

Ready to see your maximum borrowing?

| READY TO TALK TO A CENTRAL BANK-REGULATED ADVISOR? We model every active Irish lender against your income mix and show you exactly which lender maximises your borrowing before you commit to a property. No obligation. → Enquire Now | → Book an Appointment | → Contact Us |

Important information

WARNING: Your home is at risk if you do not keep up payments on your mortgage.

WARNING: The cost of your monthly repayments may increase.

WARNING: If you do not meet the repayments on your loan, your account will go into arrears. This may affect your credit rating, which may limit your ability to access credit in the future.

Central Bank of Ireland mortgage measures (4× LTI for FTBs, 3.5× for SSBs, 90% LTV for FTBs, 80% LTV for SSBs, exception allowances up to 5× LTI) and lender income-treatment ranges referenced in this article reflect Irish market practice as at June 2026. Actual borrowing capacity depends on your individual circumstances, credit history, evidenced income, deposit source and lender underwriting policies at time of application. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial or legal advice.