Before a single euro goes into an exchange-traded fund (ETF), there are five numbers on the fact sheet that deserve a proper look. Get into the habit of checking them and you turn a confusing two-page PDF into a clear decision. At Money Maximising Advisors, we help individuals and families across Ireland build savings and investment strategies that match their goals, their timeline and their appetite for risk. This pillar guide walks through exactly what to look for on an ETF fact sheet, and how that fits into a wider, tax-aware plan for your money in Ireland.

|

Having analysed the topic, this article sits squarely in the Savings & Investments category. ETFs are an investment vehicle, so the cluster of pages this guide supports includes Lump Sum Investments, Regular Saver Investment Plans, Execution Only Investing and Capital Protected Investments. |

")

The five checks every investor should run before buying an ETF.

What an ETF fact sheet actually tells you

An ETF fact sheet is the fund manager’s one or two page summary of a fund: what it holds, what it has returned, what it costs and how risky it is. It is not marketing fluff , it is the closest thing to a standardised “nutrition label” for an investment. Learning to read it is one of the most useful skills a new investor can build, and it is a recurring theme in our Beginner-Friendly Guide to Investing in Ireland. You can also watch our plain, English explainers over on the Money Maximising Advisors YouTube channel, where we break down investing concepts for an Irish audience.

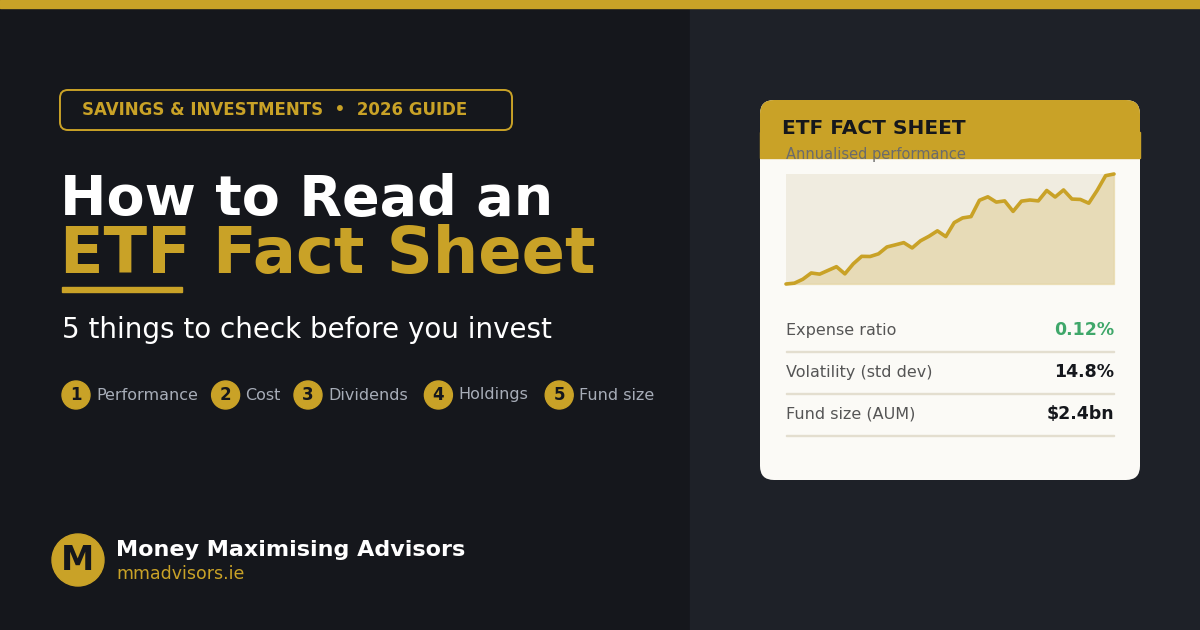

1. Annualised performance and standard deviation

Start with annualised performance. Past performance never predicts future returns, but it does show how a fund has behaved across different market conditions. A common benchmark is a broad S&P 500 tracker, which has delivered an average annual return of around 13.1% over the past five years. Comparing a fund against a recognised benchmark tells you whether you are being rewarded for the risk you take on.

While you are there, look at standard deviation the measure of how far returns swing away from that average. As a rule of thumb, roughly 15% is typical for the stock market. A figure above 20% signals a highly volatile fund, which may be fine for a long horizon but uncomfortable if you need the money sooner. Matching volatility to your timeline is exactly the kind of thing we map out in Pensions Advice and broader Retirement Planning Advice conversations.

")

Standard deviation in context: around 15% is average; above 20% flags a volatile fund.

2. Expense ratio — the cost you barely notice

The expense ratio (sometimes shown as the Total Expense Ratio, or TER) is the annual fee the fund manager charges simply for holding the fund. It is deducted automatically, so you will never see a separate line on your statement, which is precisely why it gets overlooked. For ETFs, anything below 0.20% is considered cheap, and many broad-market trackers sit between 0.05% and 0.30%. Over decades, the gap between a 0.10% fund and a 0.60% fund can quietly cost you thousands.

")

Where ETF charges typically fall — cheap, broad-market and higher-cost bands.

If you prefer a low-cost, self-directed route, Execution Only Investing may suit you. If you would rather have a strategy built and reviewed for you, our Lump Sum Investments and Regular Saver Investment Plans services do exactly that.

| Not sure which fund or platform fits your goals? Book Now for a no-obligation consultation, or Enquire Now and one of our Qualified Financial Advisors will be in touch. |

3. Dividend frequency: distributing vs accumulating

ETFs come in two flavours. Distributing funds pay your dividends out in cash, which can suit investors who want a regular income. Accumulating funds reinvest those dividends straight back into the fund automatically. Many long-term investors lean towards accumulating funds because they capture the full benefit of compounding without any manual effort. The right choice depends on whether you need income today or growth for tomorrow, a question we explore in Savings & Investments in Ireland: How Investment Funds Work. It is worth noting that Irish investors should also weigh the tax treatment of fund distributions, which we cover below.

4. Top allocations and holdings

The top allocations section lists the largest holdings that drive most of a fund’s performance. Knowing which sectors, companies or regions dominate tells you whether a fund is genuinely diversified or quietly concentrated in, say, a handful of US technology names. Concentration is not automatically bad, but it changes the amount of risk you are carrying. If you want a deeper dive on building a balanced portfolio, What Are the 4 Main Investment Strategies? is a useful next read, and our Corporate Investments service helps business owners diversify company cash sensibly.

5. Fund size and age

Finally, check fund size and age. Look for AUM, assets under management. As a rule of thumb, favour funds with at least $100 million in assets; smaller funds run a higher risk of being closed by the manager if they are not profitable, which can force an inconvenient (and sometimes taxable) exit. On age, aim for a fund that is at least three years old, giving you enough data to see how it has behaved across different market conditions. If a fund closes, knowing your options for redeploying a lump sum or rolling proceeds into Approved Retirement Funds (ARF) at retirement keeps you in control.

Watch our walkthrough of these five checks on the Money Maximising Advisors YouTube channel for a visual, step-by-step version of this guide.

Common mistakes to avoid

Even with the five checks in hand, a few habits trip up new investors again and again. Keep these in mind before you commit:

- Chasing last year’s winner. Strong recent performance often reflects a hot sector that may already be fully priced. Look at the longer track record, not just the headline number.

- Ignoring the currency. A fund priced in US dollars adds a layer of currency risk for euro-based investors. Check the base currency and any hedging on the fact sheet.

- Overlapping funds. Holding three “different” ETFs that all track the same large US companies is not diversification. Read the top holdings of each before buying.

- Forgetting the tax timeline. In Ireland, the eight-year deemed disposal rule can trigger a tax charge even if you have not sold. Plan for it rather than being surprised by it.

If any of these feel familiar, a short conversation with a Qualified Financial Advisor can save you far more than it costs.

How ETFs fit into an Irish savings and investments plan

Reading the fact sheet is only half the job. In Ireland, the tax treatment of ETFs matters just as much as the fund’s quality. Many funds are subject to exit tax and the eight-year “deemed disposal” rule, and the right structure can make a meaningful difference to your net return. That is where tailored advice pays for itself. Before you invest, it is also worth getting your foundations right: clearing expensive debt, holding an emergency fund — see How Much Should I Have in Savings in Ireland? and making sure protection such as Income Protection and Life Insurance is in place.

From there, your investment can sit alongside the rest of your financial life: pensions through Additional Voluntary Contributions (AVCs) or a Directors Pension, tax-efficient gifting via a Section 73 Policy Savings Plan, and longer-term goals such as College Education Savings. For a side-by-side view of approaches, see Lump Sum Investing vs Regular Savings & Investments and Investing in Ireland vs Offshore: Tax Implications You Must Know.

Most-read guides on Savings & Investments

These are among our highest-performing pages with Irish savers and investors, a natural next step from this pillar:

- Best Savings Accounts in Ireland: Complete Comparison

- How Much Should I Have in Savings in Ireland?

- Beginner-Friendly Guide to Investing in Ireland

- Capital Protected Investments

- Savings and Investments in Ireland: Is Investing Right for You?

Explore our full range

This guide is part of our wider Savings & Investments hub. You can also explore our Pensions, Mortgages, Protection, Public Sector and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- Savings & Investments in Ireland: How Investment Funds Work

- Achieve Financial Growth in 2026 with Tailored Savings and Investment Solutions

- A Simple Financial Planning Framework for Ireland in 2026

- How Irish Savers Can Benefit from the New Capital Gains Tax Investment Scheme

Frequently asked questions

What is a good expense ratio for an ETF?

For ETFs, anything below 0.20% is generally considered cheap, and many broad-market trackers fall between 0.05% and 0.30%. The lower the ongoing charge, the more of your return you keep over the long run.

Should I choose a distributing or accumulating ETF?

It depends on your goal. Distributing funds pay dividends as cash income, while accumulating funds reinvest them to maximise compounding. Irish tax treatment also matters, so it is worth discussing your situation through our Money Management Advice service.

How much should an ETF hold in assets under management?

As a rule of thumb, look for at least $100 million in AUM and a track record of three years or more. Smaller, newer funds carry a higher risk of closure.

Are ETF gains taxed in Ireland?

Many funds available to Irish investors are subject to exit tax and the eight-year deemed disposal rule. Because the rules are nuanced, personalised advice is sensible — Enquire Now to discuss your circumstances.

Ready to put your plan in place?

Whether you are investing a lump sum, starting a regular plan, or simply want a second opinion on a fund you are considering, our team is here to help. Book Now to arrange your consultation, or visit Money Maximising Advisors to learn more.

Disclaimer

Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, investment or tax advice. The value of investments can fall as well as rise, and past performance is not a reliable indicator of future returns. You should seek personalised advice from a Qualified Financial Advisor before making any financial decision.