In the world of property investment, unlocking the hidden potential within your assets can lead to exciting opportunities. If you own a buy-to-let property, there’s a good chance you’ve built up some equity over time. So, what does that mean for you? Imagine being able to tap into that value and use it to fund new ventures or enhance your lifestyle. This is where remortgaging a buy-to-let to release equity comes in—a powerful financial tool that allows homeowners like you to release equity from their properties.

Whether you’re looking to invest in more rental properties, fund renovations on an existing one, or simply need extra cash for other investments, understanding how buy-to-let equity release works is crucial.

In this guide, we’ll dive deep into the process of remortgaging a buy-to-let property and explore all aspects of releasing equity efficiently and effectively. Get ready to discover how smart financial moves can help you maximise your real estate investments!

Contact Money Maximising Advisors now to see how much equity you could unlock from your buy-to-let property.

What Is Equity and How Does It Work?

Equity represents the portion of your property that you truly own. It’s calculated by subtracting any outstanding mortgage balance from your home’s current market value. For instance, if your property is worth $300,000 and you owe $200,000 on your mortgage, your equity stands at $100,000.

As property values rise or fall over time, so does the amount of equity you hold. This fluctuation can occur due to changes in the housing market or improvements made to the home itself.

Homeowners can tap into their equity for various purposes—like funding renovations or consolidating debt—by utilizing methods such as remortgaging to release equity. Essentially, it serves as a financial asset that can aid in achieving broader financial goals while offering flexibility through potential borrowing options.

What Does Remortgaging to Release Equity Mean?

Remortgaging to release equity involves taking out a new mortgage on your property, often at a different lender or with revised terms. This process allows homeowners to access the value they’ve built up in their property over time.

When you purchase a home, its value increases as you pay down the mortgage and as market conditions change. The difference between what you owe and your property’s current worth is known as equity. Remortgage buy-to-let release equity taps into this value.

The funds released can be used for various purposes, such as funding renovations, consolidating debts, or investing in additional properties like buy-to-let ventures.

This approach is particularly appealing for investors looking to maximize returns by leveraging existing assets while maintaining manageable financial obligations.

Reasons to Remortgage and Release Equity

Remortgaging a buy-to-let to release equity can be a powerful financial strategy.

- One common reason is to fund home improvements. Upgrading your property not only enhances your living space but can also increase its market value.

- Another motivation could be consolidating debt. By using the cash released, you may pay off higher-interest debts, simplifying finances and potentially saving money in interest payments.

- Investing in additional properties is another compelling reason. If you’re considering expanding your portfolio, releasing equity from house for buy-to-let can provide the necessary capital for new acquisitions.

- Furthermore, some homeowners seek extra cash for life’s milestones—be it financing education or planning a dream vacation. The flexibility of BTL equity release allows you to tailor funding according to personal goals and aspirations without sacrificing long-term investments.

Enquire now with Money Maximising Advisors to learn how you can benefit from equity release.

How Much Equity Can You Release?

The amount of equity you can release from your property depends on several factors. Primarily, it hinges on the current market value of your home and the remaining balance on your mortgage.

Typically, lenders allow you to borrow up to 75% of your property’s value when remortgaging. However, this varies depending on individual circumstances and lender policies. You’ll need a Buy-To-Let Equity Release Calculator to get an accurate estimate based on specific details.

Your financial situation plays a crucial role as well. Lenders assess income stability and creditworthiness before approving equity release buy-to-let mortgage requests.

Remember that any existing debts or liens against the property can affect how much equity is available for you to leverage through remortgaging a buy-to-let to release equity. Knowing these variables will help in making informed decisions.

Steps to Remortgage and Release Equity

- To remortgage to release equity buy-to-let starts with assessing your current mortgage. Gather all relevant documents, such as your mortgage statement and property valuation.

- Next, research available lenders. Compare rates and terms that suit your needs. Many online tools can help you find the best deals tailored for buy-to-let equity release.

- Once you’ve found a suitable lender, prepare to apply. This may involve providing proof of income, rental agreements, and any other financial documentation they require.

- After submitting your application, the lender will conduct a valuation of your property. This step is crucial in determining how much equity you can access.

- If approved, carefully review the new terms before signing anything. Ensure you’re comfortable with all fees associated with this process to avoid surprises later on.

Costs and Considerations

When considering equity release on buy-to-let, it’s crucial to account for various costs. These can include valuation fees, legal expenses, and potential early repayment charges on your existing mortgage.

Valuation fees vary depending on the lender and property type, so it’s wise to get estimates beforehand. Legal costs often arise when transferring mortgages; hiring a solicitor is essential but can add another layer of expense.

Additionally, if you’re switching lenders or products mid-term, check for any penalties associated with early repayment. This might eat into the profits from releasing equity.

Keep an eye on interest rates as well. A lower rate could mean significant savings over time but remember that this may affect your monthly payments too.

Book a consultation with Money Maximising Advisors today to assess the full cost-benefit analysis of your remortgage.

Alternatives to Remortgaging to Release Equity

If remortgaging isn’t the right fit for releasing equity, there are several alternatives worth considering.

One option is a home equity loan. This allows you to borrow against your property’s value without changing your existing mortgage. It provides a lump sum that can be used for various expenses.

Another route is selling part of your property through shared ownership schemes. This lets you retain some control while accessing funds from the sale of shares.

You might also explore personal loans or lines of credit based on income and savings, which don’t rely on property value but provide immediate cash flow.

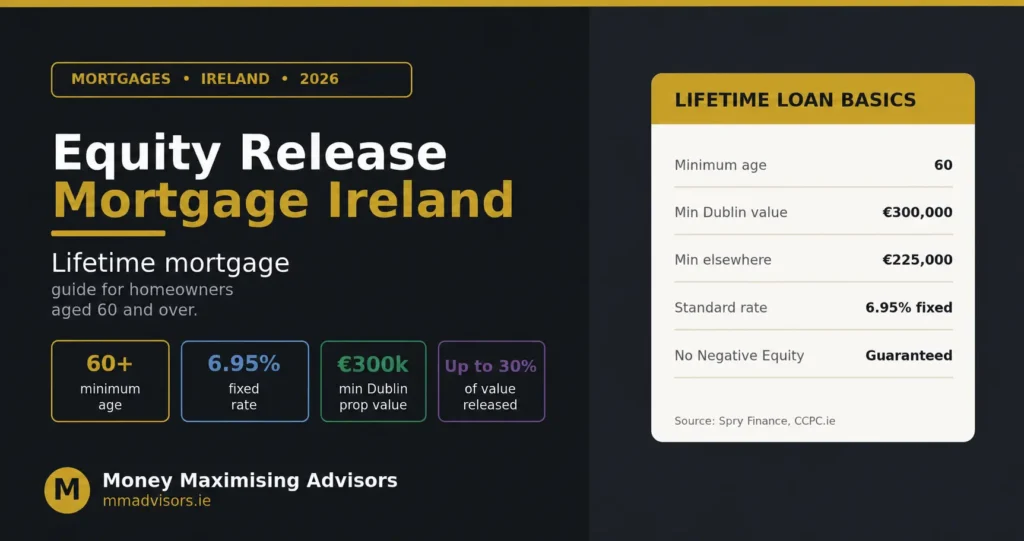

Consider lifetime mortgages aimed primarily at older homeowners. These allow you to access equity while staying in your home until later stages in life.

When Is the Right Time to Remortgage?

Timing can be everything when it comes to remortgaging a buy-to-let to release equity. It’s essential to monitor interest rates closely. If they dip significantly below your current rate, that could signal an ideal moment.

Your personal financial situation also plays a key role. A stable income or an increase in property value might encourage you to explore buy-to-let mortgage equity release options.

Market conditions are another factor. If demand for buy-to-let properties is high, now may be the time to capitalise on increased valuations.

Moreover, changes in your life circumstances might prompt you to reassess your mortgage needs.

Contact Money Maximising Advisors now for personalised guidance on timing your remortgage.

FAQs About Releasing Equity via Remortgaging

Q: Can I release equity from a buy-to-let property?

A: Yes, many lenders offer specific products for buy-to-let equity release.

Q: Will my monthly mortgage payments increase?

A: Possibly. Since you’re borrowing more, your monthly payments may rise.

Q: What are the eligibility requirements?

A: Credit score, income, rental income, and property value are all key factors.

Q: Are there tax implications?

A: Typically, no immediate taxes apply, but always consult a financial advisor.

Q: How much equity can I expect to release?

A: It depends on your property value and mortgage balance. Use a Buy-To-Let Equity Release Calculator to estimate.

Conclusion

Understanding how to remortgage to release equity buy-to-let can empower you financially. Whether you’re looking to fund home improvements, invest in additional properties, or consolidate debt, accessing the equity in your buy-to-let is a strategic move.

By comprehensively evaluating your mortgage terms and understanding the market dynamics, you can make informed decisions aligned with your financial goals. Engaging with Money Maximising Advisors will ensure you navigate this process effectively while considering all available options.

With the right knowledge and support, releasing equity through remortgaging may open doors for future investments or personal growth opportunities. Remember to assess each step carefully and utilise tools like a Buy-To-Let Equity Release Calculator for accurate, tailored figures.

Enquire now with Money Maximising Advisors and start unlocking the full potential of your property!