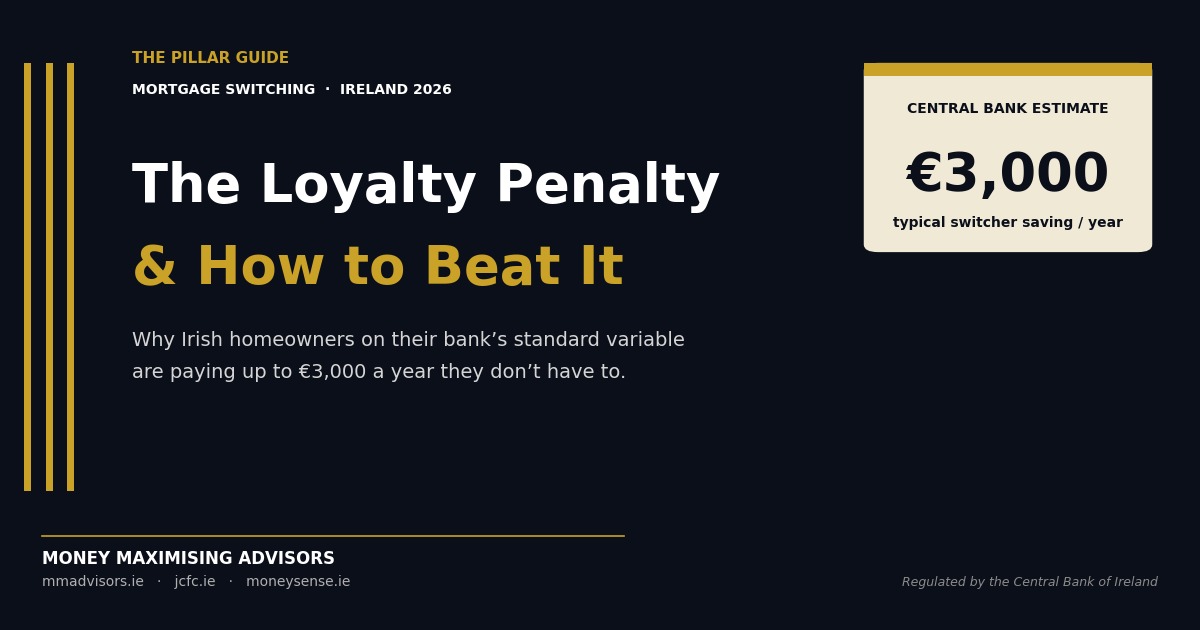

| AT A GLANCE €30,000 +The typical lifetime saving an Irish homeowner unlocks by switching from a legacy variable rate to a competitive fixed or green rate on a €200,000 mortgage. Yet, per Central Bank of Ireland data, most eligible switchers still don’t act. This 2026 guide walks you through when to switch, how the 6–8 week process actually works, and the mistakes that quietly cost people money, with real numbers, real timelines, and real regulatory rules from the CCPC and Central Bank of Ireland. |

| WHAT THIS GUIDE COVERS | |

| ✓ When switching your mortgage in Ireland is worth it ✓ The 6–8 week switching process, step by step ✓ Real savings numbers on a €200,000 mortgage ✓ Fixed vs variable vs green mortgage options | ✓ Central Bank of Ireland Consumer Protection Code rules ✓ Common switching mistakes (and how to avoid them) ✓ Costs: valuation, solicitor and mortgage protection ✓ How the three MMA Group offices can help |

Four numbers every Irish homeowner should sanity-check before they start a switcher application.

If you took out a mortgage in Ireland three, five or ten years ago, the odds are strong that you are paying more than you need to. Rates in the Irish market have moved significantly since 2022, competition among lenders is at its strongest in over a decade, and the mortgage comparison Ireland landscape now includes green rates, high-value discounts, cashback offers and BER-linked incentives that simply weren’t on the shelves when your original loan was drawn down. This pillar guide from the Money Maximising Advisors Group (mmadvisors.ie in Galway, jcfc.ie in Donegal and moneysense.ie in Kerry) walks you through when to switch, how the process actually works, what it costs, and how to talk to a mortgage broker Ireland homeowners regularly recommend.

For our full Mortgage Comparison Advice service, see the primary hub. Related pillars: Mortgages, Mortgage Protection, Public Sector Mortgages and Buy-to-let Mortgages.

The Quick Answer: 7 questions Irish homeowners ask before switching

What is mortgage switching in Ireland?

Mortgage switching is moving your existing home loan from your current lender to a new lender — usually to lock in a lower interest rate, a better fixed term, or a cashback incentive. Your mortgage debt, term and property don’t change; only the lender and the rate do. It is not the same as remortgaging (which typically means taking additional equity out). In Ireland, switching is governed by the Central Bank Consumer Protection Code and typically takes 6–8 weeks.

How do I switch my mortgage in Ireland?

Seven steps: (1) compare rates across the full Irish lender panel; (2) get Approval in Principle from your chosen new lender; (3) pay for a valuation from an approved valuer (~€150); (4) receive the formal Loan Offer (Central Bank rules require the lender to decide within 10 business days of a completed application); (5) engage a solicitor to handle the deed transfer; (6) assign your mortgage protection to the new lender; (7) draw down and clear the old mortgage. A mortgage advisor Ireland homeowners typically use, like the MMA Group, handles the paperwork end-to-end at no cost to you.

Is switching a mortgage worth it in Ireland?

Almost always, provided the rate difference is at least 0.5% and you have more than 5 years left on your term. On a €200,000 mortgage with 25 years remaining, switching from a 4.5% variable to a 3.0% green fixed saves around €160/month and roughly €49,000 over the remaining term, before switching costs. Even after mortgage switching costs (typically €1,500–€2,500 for valuation and legal fees), the net is well ahead — and many lenders offer cashback of 2–3% of the loan that more than covers those costs.

Can I switch my mortgage before my fixed rate ends?

Yes, but you may pay a break fee an early-repayment charge for exiting a fixed rate ahead of schedule. The fee depends on the difference between the interest rate you fixed at and current interbank market rates for the remaining fixed period. Sometimes the break fee is €0; sometimes it’s several thousand euro. A qualified mortgage advisor can request a written break-fee quote from your existing lender before you commit, and model whether the savings from switching still justify the fee. If your fixed rate is due to end within 6 months, you almost always wait, there’s rarely a break fee then.

How long does it take to switch a mortgage in Ireland?

Typically 6–8 weeks from initial application to full drawdown. The Central Bank’s Consumer Protection Code requires your new lender to give a decision within 10 business days of receiving a completed application, but the full timeline also includes valuation (1–2 weeks), solicitor deed transfer (2–4 weeks), and mortgage protection re-assignment. Some complex cases take longer — particularly older properties needing an engineer’s report.

What documents are required to switch a mortgage?

Six months of bank statements, three months of payslips, most recent P60 or Notice of Assessment (self-employed), evidence of any additional income (rental, bonus, guaranteed overtime), photo ID, proof of address, current mortgage statement showing the outstanding balance and rate, and BER certificate (particularly important if you’re applying for a green mortgage rate). Digital submission is now standard with most Irish lenders. Because you’ve already proven you can service a mortgage, switchers often require fewer supporting documents than a first-time application.

Can I switch my mortgage to another lender if I have a tracker?

You can, but you will permanently lose the tracker rate. Tracker mortgages (typically ECB + a low margin) are rarely worth surrendering because the ECB+margin structure is significantly cheaper than any current market fixed rate for most trackers. Always get advice before switching off a tracker — in most cases the correct answer is to stay put and switch other elements (like moving your mortgage protection to a cheaper insurer).

Chapter 1 :- When switching mortgages in Ireland actually pays off

Not every switch saves money. Before you begin the process, run through the three tests that determine whether a switch is genuinely worth it for you as a mortgage in Ireland holder.

Test 1 :- The rate gap test

Compare your current interest rate to the best mortgage rates Ireland lenders are offering to switchers on your LTV band. As of mid-2026, headline switcher rates in Ireland run from around 3.00% (PTSB 4-year fixed, LTV ≤60%, BER A/B) through to 4.70% for standard variable rates on higher-LTV loans. If your current rate is more than 0.5% above the best switcher rate available for your LTV and BER, you’re a candidate.

Test 2 :- The remaining-term test

Switching only pays off if you have enough remaining term to recover the switching costs and enjoy the savings. As a rule of thumb, if you have fewer than 5 years left on your mortgage, the switching costs may outweigh the savings. If you have 10, 15, 20 or more years left, the maths almost always favours the switch.

Test 3:- The LTV / BER improvement test

Your Loan-to-Value ratio (mortgage balance divided by house value) may have improved substantially since drawdown, either because you’ve paid down the loan or because your property has appreciated. Lower LTVs unlock cheaper rate bands with almost every Irish lender. Similarly, if you’ve upgraded your Building Energy Rating (BER) to A or B, you may now qualify for a green mortgage Ireland homeowners increasingly access at rates as low as 3.00–3.20%.

Chapter 2 :- The 6–8 week switching process, step by step

The Irish mortgage switching process is well-established and, once you’ve done the up-front comparison, largely administrative. Here’s exactly how the 6–8 weeks break down when you work with a mortgage broker Ireland homeowners can rely on:

The seven stages of a typical Irish mortgage switch — timelines assume responsive documentation.

Stage 1–2 Comparison and Approval in Principle

Week one is about assessing whether you should switch at all. Your broker (or you directly) runs quotes across all active Irish lenders — currently AIB, Bank of Ireland, PTSB, Haven, EBS, Avant Money, ICS Mortgages, Finance Ireland and (increasingly) high-value/green specialists. The comparison uses your current LTV, BER, income and household budget. If a switch stacks up, an Approval in Principle application follows in week two.

Stage 3–4 Valuation and Loan Offer

Your new lender requires a fresh valuation from one of their approved panel valuers. Cost: ~€150. Valuations are valid for 4 months. Once the valuation is in, the lender issues a formal Loan Offer, the Central Bank Consumer Protection Code requires this decision within 10 business days of receiving a completed application, and the offer sets out the exact rate, term, monthly repayment and conditions.

Stage 5–6 Solicitor and mortgage protection

Your solicitor handles the legal fees for switching mortgage homeowners can expect to see — typically €1,200–€1,800 all-in including outlays, deed transfer, Tailé Éireann registration and land registry fees. Simultaneously, your existing mortgage protection policy needs to be reassigned to the new lender (or, if you’ve been overpaying for years, a fresh policy taken out at a better price).

Stage 7 Drawdown

Once the new lender has the signed offer, the assigned mortgage protection and the solicitor’s undertakings, funds transfer between lenders. Your old mortgage is cleared, your new one begins, and your next monthly repayment goes to the new lender. Total elapsed time: usually 6–8 weeks, sometimes longer if lender panels are backed up or documents are slow returning.

| READY TO SPEAK TO AN ADVISOR? Whichever region you live in, the Money Maximising Advisors Group can connect you with a Central Bank of Ireland regulated advisor for a free, no-obligation consultation. Choose your next step: → Enquire Now — 15-minute callback within one working day. → Book an Appointment — 30-minute in-person or online consultation. → Contact Us — general enquiries and callback requests. |

Chapter 3 :- Switching costs, cashback offers and net savings

The full sweep of mortgage switching costs in Ireland in 2026 is straightforward and predictable:

- Valuation fee: ~€150 (paid to an approved valuer of the new lender).

- Solicitor fees: €1,200–€1,800 including outlays and registration.

- Break fee (if applicable): €0 to several thousand euro, depending on interbank rate movements.

- Structural engineer report: ~€300–€500 for properties over 100 years old, rare.

- Broker fee: €0 with the MMA Group, lenders pay the broker directly.

Most switchers see all-in costs of around €1,500–€2,500. Against that, many Irish lenders offer switcher cashback of 2–3% of the mortgage, on a €200,000 switch, that’s €4,000–€6,000 straight to your bank account, more than covering the switching costs and often leaving €2,000+ in your pocket before the monthly saving even starts.

| MONEY MAXIMISING ADVISORS GROUPTalk to a local, Central Bank of Ireland regulated advisor in your region. | ||

| TUAM · GALWAY mmadvisors.ie National coverage Flagship group HQ, full mortgage, pension, protection and inheritance advice across Ireland. | MOUNTCHARLES · DONEGAL jcfc.ie North West Ireland Joe Coyle Financial Consultants business-owner and family finance specialists. | KILLARNEY · KERRY moneysense.ie South West Ireland Money Sense Financial Services, family-run, over 40 years of Irish financial experience. |

Real-world scenario A Galway couple who saved €48,000 by switching in 2026

A married couple in Galway city took out a €260,000 mortgage in 2020 on a 30-year term with Bank of Ireland at 3.20% fixed for 3 years. At the end of the fixed period in 2023, they rolled onto a variable rate of 4.40%. In late 2025 they retrofitted the property to a BER B2 rating (attic insulation, external wall insulation, heat pump). In February 2026 they approached MMA Advisors.

Their remaining balance was €232,000 with 24 years left. Their LTV had fallen from 90% at drawdown to 66% (house price appreciation plus repayments). Their new BER qualified them for a green fixed rate.

MMA arranged a switch to PTSB’s green 5-year fixed at 3.10%, with 2% cashback. Monthly repayment fell from €1,290 to €1,124, a saving of €166/month. Over the remaining 24 years, that’s roughly €47,800 in interest saved. PTSB’s €4,640 cashback more than covered the €1,900 in valuation, solicitor and admin fees, so they were €2,740 in the black on day one, before the monthly savings started.

Common switching mistakes vs the right way to do it

| RED FLAGS ✗ Cancelling old mortgage protection before the new one is assigned. ✗ Ignoring the break fee — not requesting a written quote before applying. ✗ Comparing rates only, not APRC (which includes fees and reversion rate). ✗ Choosing the highest headline cashback without checking the rate. ✗ Switching off a tracker rate — almost always a mistake. ✗ Waiting past the 60-day CPC notice with no comparison shopping done. | GREEN FLAGS ✓ Start the comparison 3–6 months before your fixed rate expires. ✓ Get a written break-fee quote in hand before committing to switch. ✓ Compare APRCs across the full Irish lender panel, not just headline rates. ✓ Model cashback + rate combined over the fixed term (not just year 1). ✓ Reassign mortgage protection only after the new policy is in force. ✓ Use a Multi-Agency broker — access to all lenders at no direct cost. |

Explore related MMA Group hubs

This guide sits within our Mortgage Comparison Advice service pillar. Related hubs: Mortgages, Mortgage Protection, Buy-to-let Mortgages, Public Sector Mortgages, Irish Ex-pat Mortgages and Equity Release Mortgages. Learn more about us, or explore our sister firms Joe Coyle Financial Consultants (Donegal) and Money Sense Financial Services (Kerry).

Related posts

| Related Post | Focus | Read More |

|---|---|---|

| Mortgage Broker in Dublin: Switching Mortgage — How to Get My BER Certificate (2026 Guide) | BER certificates for switchers | Read more → |

| First Time Mortgage Buyers in Galway: Inflation and Its Impact on Interest Rates | FTB inflation impact | Read more → |

| 10 Things to Know Before Applying for a Mortgage in Ireland | Pre-application checklist | Read more → |

| Public Sector Mortgage Ireland: What Do I Need to Apply for a Mortgage? | Public sector applicants | Read more → |

Frequently asked questions about switching mortgages in Ireland

How much does it cost to switch a mortgage in Ireland?

All-in switching costs typically run €1,500–€2,500 (valuation ~€150 + solicitor €1,200–€1,800 + admin outlays). Broker fees are €0 with a Multi-Agency Intermediary like the MMA Group. Many lenders offer 2–3% cashback that fully offsets these costs.

Do I have to switch my mortgage protection when I switch lender?

No. Your existing mortgage protection policy can be reassigned to the new lender via a short administrative letter. However, this is a good moment to shop the market — premiums have moved, and most Irish homeowners on legacy policies are overpaying by 30–50%. Never cancel the old policy until the new one is fully in force.

Will switching affect my credit rating?

Not negatively, provided the new mortgage is drawn down before the old one is cleared. Lenders search the Central Credit Register during the application, which is a normal, routine footprint. Missing repayments during the switch process would damage credit — keep paying the old mortgage until drawdown day.

Can I switch mortgage if I’m self-employed in Ireland?

Yes. Self-employed applicants typically need two years of Notices of Assessment, current tax clearance, and up-to-date accounts. Several Irish lenders have improved their self-employed underwriting recently, so switching is realistic if your business income is stable or growing.

| REVIEWED BY THE MONEY MAXIMISING ADVISORS GROUP Content reviewed by Qualified Financial Advisors at Money Maximising Advisors (Tuam, Co Galway), Joe Coyle Financial Consultants (Mountcharles, Co Donegal) and Money Sense Financial Services (Killarney, Co Kerry). All three firms operate as part of the Money Maximising Advisors Group, regulated by the Central Bank of Ireland and authorised as Multi-Agency Intermediaries across the main Irish lenders, life insurers and pension providers.Every recommendation we make is documented in a written Statement of Suitability under the Central Bank Consumer Protection Code. |

Ready to check what you’d save by switching?

Every Irish homeowner’s switching maths is different — your rate, your LTV, your BER and your remaining term. The Money Maximising Advisors Group runs live quotes across all active Irish lenders and takes you from first comparison through drawdown at no direct cost.

| READY TO SPEAK TO AN ADVISOR? Whichever region you live in, the Money Maximising Advisors Group can connect you with a Central Bank of Ireland regulated advisor for a free, no-obligation consultation. Choose your next step: → Enquire Now — 15-minute callback within one working day. → Book an Appointment — 30-minute in-person or online consultation. → Contact Us — general enquiries and callback requests. |

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it. WARNING: The cost of your monthly repayments may increase. If you do not meet the repayments on your credit agreement your account will go into arrears. This may affect your credit rating which may limit your ability to access credit in the future.

Content correct as of June 2026. Rates, exemption thresholds and regulatory rules referenced in this article are subject to change. The Money Maximising Advisors Group (Money Maximising Advisors Limited, Joe Coyle Financial Consultants and Money Sense Financial Services) is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. You should always seek personalised advice from a Qualified Financial Advisor before making any decision.