Delve into the diverse world of buy-to-let mortgages in Ireland—uncovering the latest rates, borrower requirements, and options for individuals, pensions, and companies. Discover what it takes to secure the best deal in today’s dynamic property market.

Introduction to Buy-to-Let Mortgages in Ireland

In recent years, the Irish property market has seen a significant surge in interest from investors looking to capitalise on rental opportunities. However, understanding the best buy-to-let mortgage rates Ireland offers can be a daunting task, given the myriad options available to individuals, pension funds, and companies. Choosing the right mortgage can make a substantial difference in your investment returns, whether you’re an individual landlord, a pension investor, or operating through a Special Purpose Vehicle (SPV).

This guide aims to demystify the landscape of buy-to-let mortgages in Ireland, providing you with detailed insights into the current rates, application requirements, and financial considerations for each borrower type. By comparing these options, you can make informed decisions that align with your investment goals and maximise your rental income. Let’s delve into what buy-to-let mortgages entail and explore the best approaches for securing favourable rates in today’s market. Whether you’re a novice investor or a seasoned landlord, understanding these dynamics is crucial for navigating the complexities of the Irish property scene.

What is Buy-to-Let?

Buy-to-let refers to the practice of purchasing residential property with the intention of renting it out. This investment strategy has become increasingly popular as individuals seek alternative income streams beyond traditional employment. In Ireland, this type of investment attracts both new and seasoned investors due to its potential for steady cash flow and capital growth.

A buy-to-let mortgage is specifically designed for landlords who want to rent out their properties. Unlike standard residential mortgages, these loans often come with different eligibility criteria and higher interest rates. Lenders typically assess the potential rental income alongside the applicant’s financial profile when determining loan approvals.

With rising property values in urban areas across Ireland, many see buy-to-let as an avenue for long-term wealth building. However, understanding the nuances of this investment is crucial before diving in. From repayment options to leveraging pension funds or company structures, various routes can suit different investor needs.

Buy-to-Let Mortgage Benefits

Prospective landlords looking for the best buy to let mortgage rates in Ireland have a wealth of options to explore. Buy-to-let mortgages offer unique advantages that make property investment appealing.

These loans allow investors to leverage rental income as part of their financial strategy. With the right buy to let investment mortgage in Ireland, individuals can generate consistent cash flow while building equity over time.

Moreover, buy-to-let mortgages often come with flexible terms and competitive interest rates. This enables borrowers to tailor repayment plans according to their budget and investment goals.

For those considering long-term investments, fixed-rate options provide stability amid fluctuating market conditions. It’s an attractive proposition for both seasoned landlords and newcomers alike.

Additionally, leveraging pension funds or investing through a Special Purpose Vehicle (SPV) opens doors for strategic tax planning. These pathways enable varied approaches suited to different investor needs.

You might also like our post on Buy To Let Mortgage Rates Vs Spv Mortgage Rates In Ireland: A Complete Comparison.

3 Different Borrower Types

When it comes to buy-to-let mortgages in Ireland, potential borrowers can choose from three distinct types. Each offers unique advantages tailored to specific financial situations.

First, individual investors often find straightforward application processes and competitive rates. These borrowers typically rely on personal income to secure their loans.

Pension-based borrowing is ideal for those looking to diversify retirement funds through property investment. This option enables leveraging existing pension assets while enjoying tax benefits.

Companies looking at buy-to-let opportunities can opt for Special Purpose Vehicles (SPVs). These legal entities allow corporations to separate property investments from other business activities, reducing risk exposure and potentially enhancing yield.

Understanding these borrower types enables investors to tailor their approach effectively when navigating the Irish mortgage market.

Application Requirements for Buy-to-Let Properties

Property Requirement

When considering a buy-to-let mortgage in Ireland, property requirements play a crucial role. Lenders typically have specific criteria that properties must meet to qualify.

The property should be situated in an urban location with a population of at least 3,000 residents. This ensures demand from tenants and enhances investment security.

Additionally, the condition of the property is important. Most lenders will only consider habitable dwellings—meaning no major repairs are needed before renting out.

Related read: Buy To Let Mortgages In Ireland: Find Our Best Rates.

The minimum value for eligible properties usually starts at €115,000. Owners should also note that special approvals may be necessary depending on the type or size of the rental unit.

Meeting these requirements sets you up for smoother mortgage approval while maximising your returns as an investor.

Curious about buy-to-let mortgages? Enquire now and let us guide you through your investment journey.

Applicants

Applying for a buy-to-let mortgage in Ireland often involves multiple applicants. Up to four individuals can be included on a single application, increasing flexibility and sharing the financial burden.

Ready to take the next step? Book a consultation now and speak with our mortgage experts.

At least one applicant must reside in Ireland. This requirement helps lenders assess eligibility based on local economic conditions.

Each person’s income is crucial. Combined incomes should generally meet or exceed €40,000 per annum. Lenders scrutinise these figures closely during the approval process.

Joint applicants must provide thorough identification and proof of address documents. These steps ensure transparency and compliance with legal requirements.

Understanding these criteria can streamline your journey toward securing favorable buy-to-let mortgage rates in the Irish market.

Borrowings and Deposits

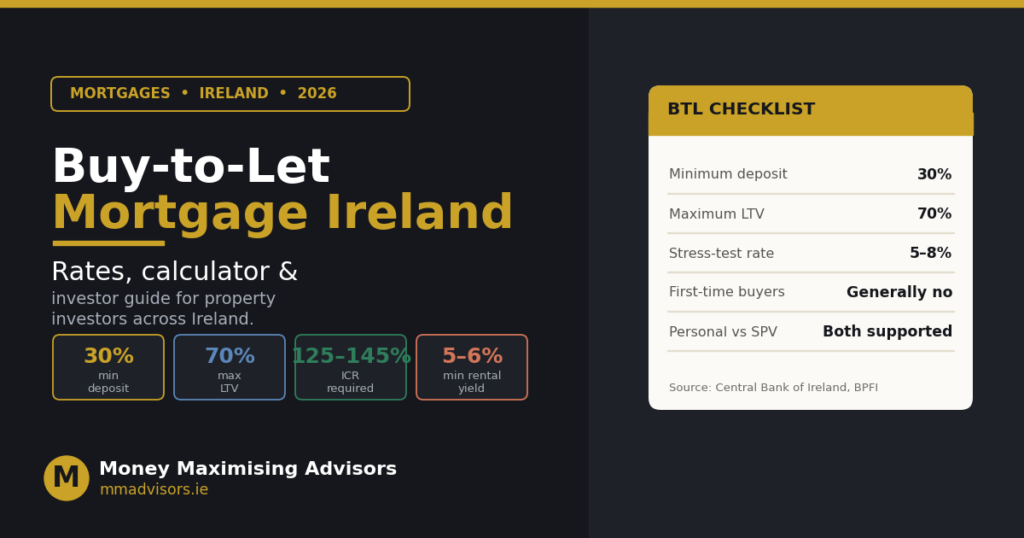

When considering a buy-to-let mortgage in Ireland, understanding the borrowing and deposit requirements is crucial. Lenders typically offer up to 70% of the property’s value as a maximum loan.

Recommended: Buy To Let Mortgage Costs In Ireland: Full Breakdown For 2025.

This means you’ll need a minimum deposit of 30%. Your ability to provide this amount can significantly influence your mortgage options.

If you’re a first-time investor or purchasing multiple properties, lenders may scrutinise your financial situation even more closely. They often assess rental income alongside other sources of revenue.

It’s also important to note that interest rates on buy-to-let mortgages are usually higher than those for residential properties. This difference can affect your overall repayments over time.

A strong credit history can improve your chances of securing favourable terms. Being prepared with documentation and clear financial records will help streamline the application process.

Terms

One crucial aspect to consider when seeking a buy-to-let mortgage in Ireland is the loan term. The duration you choose can significantly impact your repayments.

Most lenders offer terms ranging from 25 to 40 years. This flexibility allows borrowers to align their financial strategy with long-term investment goals.

The choice of term also affects eligibility and affordability. While longer terms lead to lower monthly payments, they may also result in higher overall interest costs.

Lenders often require proof of pension entitlement if the term extends beyond age 68. This ensures stability for both parties involved in the transaction.

You might also like our post on Everything You Need To Know About Using A Spv Company For Buy To Let Property.

Understanding these terms helps optimise your approach toward securing a buy-to-let mortgage that fits both immediate and future plans.

Interest Rate

Interest rates play a crucial role in buying a property. For buy-to-let mortgages, the rates can significantly impact your monthly repayments and long-term investment returns.

In Ireland, interest rates for buy-to-let properties often range between 5.35% to 5.85%. These figures can fluctuate based on various factors, such as market conditions and lender policies.

The type of mortgage you choose also affects the rate offered. Fixed-rate options provide stability by locking in the same monthly payment over an agreed period, while variable rates may change according to market trends.

Comparing different lenders is essential when seeking the best deal. Many financial institutions offer slightly different rates that could save or cost you thousands over time.

Secure your future investment. Book a consultation today to explore your buy-to-let mortgage opportunities.

Stay informed about current market trends as these will affect your borrowing costs significantly.

Unsure which buy-to-let mortgage suits you? Enquire today for personalised options tailored to your needs.

Financial Assessment

When applying for a buy-to-let mortgage in Ireland, financial assessment plays a crucial role. Lenders scrutinise your income to ensure you can cover repayments comfortably.

Most lenders require rental income equivalent to at least 1.2 times the mortgage repayment. This safety margin helps reduce risk for both parties involved.

Related read: Step By Step Guide: How To Get An Investment Property Mortgage In Ireland (Using An Spv).

If you’re an individual borrower, personal finances are key factors in approval. Your credit history and existing debts will impact what rates you qualify for.

For those considering pensions or SPVs, the focus shifts slightly. Here, it’s about demonstrating adequate investment returns and future sustainability rather than just immediate earnings.

Accuracy is vital during this stage; providing clear documentation will streamline your application process significantly.

How We Help You Secure Buy-to-Let Mortgages in Ireland?

Navigating the intricacies of buy-to-let mortgages can be daunting. At Mortgages.ie, we simplify the process for you. Our team of experts provides tailored advice based on your unique situation.

We help you assess various lender options to find the best rates available. By understanding current market trends, we guide you toward informed decisions that optimise your investment returns.

Our professionals assist with documentation and application processes, ensuring a smooth journey from start to finish. We clarify eligibility criteria and work closely with lenders on your behalf.

We provide ongoing support throughout the mortgage lifecycle. This commitment ensures our clients stay updated about potential refinancing opportunities as their circumstances evolve over time.

FAQs

1. What are the current best buy-to-let mortgage rates in Ireland?

Buy-to-let mortgage rates in Ireland can vary widely based on factors such as the lender, the amount borrowed, the borrower’s creditworthiness, and the loan-to-value (LTV) ratio. Generally, the best rates tend to start from around 3.5% for fixed-rate deals, but rates can go higher depending on your circumstances.

Recommended: Unlocking The Path To Homeownership: Demystifying Mortgage Rates In Ireland.

Top Providers: Banks like AIB, Bank of Ireland, and Permanent TSB often offer competitive rates.

Comparison Tools: Use online mortgage comparison tools to stay updated on the latest rates.

2. How do buy-to-let mortgages work in Ireland?

Buy-to-let mortgages are designed for individuals who want to purchase properties to rent out. Key points include:

LTV Ratio: Typically, lenders require a lower LTV ratio for buy-to-let mortgages, often around 70%.

Interest Rates: Buy-to-let mortgage rates tend to be higher than those for residential properties.

Rental Income: Lenders will assess the potential rental income to ensure it covers the mortgage repayments.

3. What is a buy-to-let investment mortgage?

A buy-to-let investment mortgage is specifically tailored for investors seeking to buy property for rental income. These mortgages usually require:

Higher Deposits: You’ll typically need a deposit of at least 25-30% of the property value.

Tax Considerations: Rental income is taxable, but you can offset certain expenses.

4. Can I get a buy-to-let mortgage through my pension?

Yes, it’s possible to use your pension to invest in property through a self-administered pension scheme. This approach allows you to leverage your retirement savings for property investment while potentially enjoying tax benefits.

5. What are SPVs, and how do they relate to buy-to-let mortgages?

Special Purpose Vehicles (SPVs) are companies created solely for holding property investments. Using an SPV can provide several advantages:

Tax Efficiency: An SPV structure may offer better tax treatment, especially for higher-rate taxpayers.

Flexibility: It allows easier transfer of ownership and could facilitate raising additional finance.

6. What is the process for securing a buy-to-let mortgage in Ireland?

Securing a buy-to-let mortgage involves several steps:

Financial Assessment:

Lenders will assess your financial situation, including income, credit score, and existing debts.

Property Valuation:

The property will be evaluated to determine its value and potential rental income.

Application Requirements:

Be prepared to provide documentation such as proof of income, identification, and details of other properties you own.

7. What are the key differences between buy-to-let and residential mortgages?

Purpose: Residential mortgages are for properties intended for personal use, while buy-to-let mortgages are for properties intended to be rented out.

Lending Criteria:

Lenders typically require higher deposits (usually around 40%) and may apply stricter affordability checks based on expected rental income.

Interest Rates: Buy-to-let mortgages often come with higher interest rates than residential loans due to increased risks.

8. Can I live in a buy-to-let property?

A buy-to-let mortgage is specifically for properties that are rented out. Living in such a property would violate your mortgage terms. If circumstances change and you wish to move into the property, it’s essential to:

Notify Your Lender: Inform your lender of your intentions as they may require you to switch to a residential mortgage.

Review Conditions:

Understand any penalties or conditions involved in making this transition.

9. What is a let-to-buy mortgage, and how does it differ from a buy-to-let mortgage?

A let-to-buy mortgage allows you to rent out your current home while purchasing a new one. This can be beneficial if:

Transitioning Homeownership: It enables you to move without selling your existing property immediately.

Rental Income: The rental income from your old home can help cover the new mortgage repayments.

Complexity: It involves managing two mortgages simultaneously, which can be more complicated than traditional buy-to-let arrangements.

10. What documentation is required for a buy-to-let mortgage application?

Proof of income (e.g., payslips or tax returns)

Bank statements

Identification (passport or driver’s license)

Details of existing property portfolio (if applicable)

CONCLUSION

Navigating the landscape of buy-to-let mortgages in Ireland can be both exciting and overwhelming. With various borrower types and options available, it’s essential to carefully evaluate your financial situation and investment goals. Whether you’re an individual looking to diversify your portfolio, leveraging a pension for property investment, or operating through a company structure like an SPV, understanding the nuances is crucial.

Application requirements vary but generally emphasize a substantial deposit, sound financial standing, and meeting property criteria. These elements form the foundation that lenders consider when assessing your eligibility for favourable rates. As interest rates fluctuate, staying informed about market trends can significantly impact your decision-making process.

Ultimately, securing a buy-to-let mortgage requires careful planning and strategic thinking. By equipping yourself with knowledge about current rates and terms tailored to different borrower profiles, you position yourself for successful investments in Ireland’s dynamic real estate market. The journey may be intricate but rewarding for those who approach it with diligence and foresight.

To achieve success in this venture, it’s essential to work with professionals who understand the intricacies of the mortgage market. You must assess various lender options to find the best rates available, and stay informed about your choices. This commitment ensures you stay updated about potential refinancing opportunities as your circumstances evolve over time. If you’re ready to explore buy-to-let mortgage options tailored to your needs, contact us today at Money Maximising Advisors for expert guidance and a seamless application process.