Investing in property can be an exciting venture, especially for those eyeing the lucrative buy-to-let market in Ireland. With a growing demand for rental properties and shifting economic landscapes, many are eager to take the plunge into landlord life. But before you dive headfirst into this world of investment opportunities, it’s crucial to understand the costs involved—both upfront and ongoing.

Whether you’re a seasoned investor or a first-time landlord seeking guidance on funding your dream rental property in Ireland, this comprehensive breakdown will help demystify the complexities of buy-to-let mortgages. Get ready to unlock key insights that could save you money and maximise your return on investment!

Key Buy-to-Let Mortgage Costs in Ireland

When considering buy-to-let mortgages in Ireland, it’s essential to understand the various costs involved.

- Arrangement Fees: Charged by lenders; can range from a few hundred to several thousand euros.

- Valuation Fees: Required by lenders to assess the property’s value before approving the mortgage.

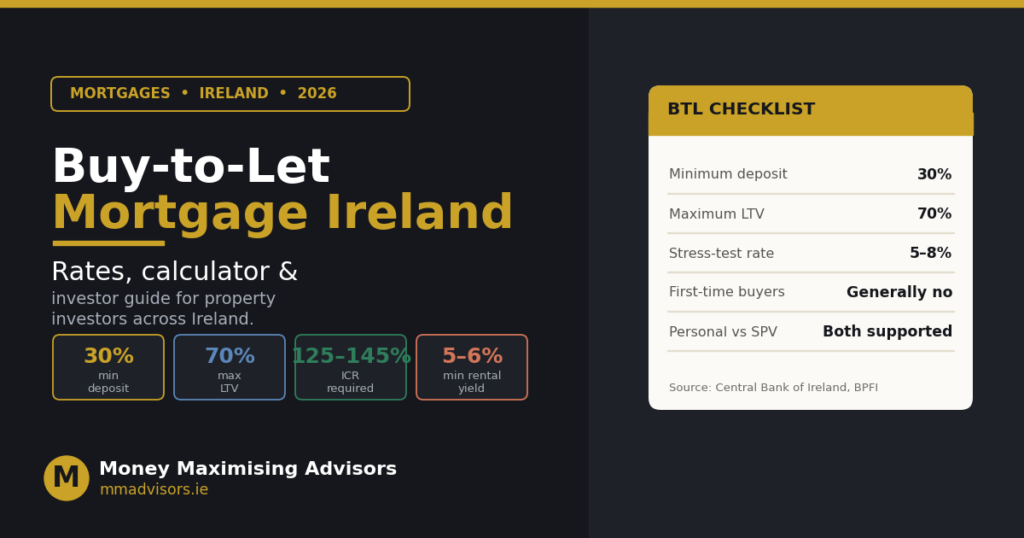

- Deposit Requirement: Typically 20%–30% of the property value for buy-to-let mortgages in Ireland.

- Property Management Fees: If using an agency, expect a percentage of your monthly rental income to go toward management.

- Insurance Costs: Landlord insurance is essential to cover property damage and liability risks.

Understanding these key costs will help equip you as a savvy investor in Ireland’s buy-to-let market.

Upfront Costs for Buy-to-Let Investors

When diving into the buy-to-let market, upfront costs can catch many investors off guard. Understanding these expenses is crucial for informed decision-making.

- First on the list is the deposit. Typically, lenders require at least 20-25% of the property’s value. This significant sum sets the foundation for your investment journey.

- Next comes stamp duty. This tax applies to property purchases and varies depending on price brackets, so it’s wise to budget accordingly.

- Another cost to consider is legal fees. Engaging a solicitor or conveyancer ensures all paperwork is managed correctly, but can add hundreds to your initial outlay.

- Don’t forget about survey fees either. A thorough inspection helps identify potential issues with the property that could lead to costly repairs down the line.

- Factor in any necessary renovations or furnishings needed before tenants move in; they play a vital role in attracting renters quickly.

Ongoing Costs of Buy-to-Let Mortgages in Ireland

Ongoing costs associated with buy-to-let mortgages in Ireland can significantly impact your investment strategy. Monthly mortgage repayments are just the beginning of what landlords need to account for.

Property maintenance is another critical expense. Regular upkeep, repairs, and unexpected emergencies can quickly add up, requiring a dedicated budget.

Insurance also plays a vital role in safeguarding your property. Landlords typically need building insurance and may opt for landlord insurance to cover specific risks related to rental properties.

Let’s not forget about management fees if you hire an agency to handle tenant relations or property oversight. These costs vary but should be considered carefully when evaluating profitability.

You will have ongoing utility expenses unless they are covered by tenants directly. Understanding these factors helps ensure better financial planning for anyone considering buy-to-let investments in Ireland.

Interest Rates for Buy-to-Let Mortgages (2025 Trends)

As we look ahead to 2025, interest rates for buy-to-let mortgages in Ireland are poised for change. Economic indicators suggest a potential rise, reflecting broader market trends and central bank policies.

Many lenders may introduce more competitive options to attract investors amid shifting demand. This could result in varied pricing strategies across the board.

Fixed-rate mortgages might gain traction as landlords seek stability against fluctuating costs. Meanwhile, variable rate products could still appeal to those willing to take calculated risks with potentially lower initial rates.

Understanding these dynamics is crucial for navigating the mortgage landscape effectively. Investors should stay informed about changes and consult specialists like Money Maximising Advisors for tailored advice in this evolving environment.

Tax Considerations for Buy-to-Let Property Owners

Tax implications play a significant role for buy-to-let property owners in Ireland. Understanding these considerations can greatly influence your investment strategy.

Rental income is taxable, and you must declare it on your annual tax return. The current standard rate of income tax applies here, so keeping detailed records of all earnings and expenses is essential.

Property-related expenses such as maintenance, repairs, and even management fees are deductible. This means that savvy landlords can reduce their taxable income by effectively managing costs.

Capital Gains Tax (CGT) also comes into play when selling a rental property. A gain made from the sale will be taxed at 33%, so it’s wise to track all improvements made over time since they could potentially offset taxes owed upon sale.

Additionally, wear-and-tear allowances have been restructured in previous years. Familiarising yourself with these nuances ensures you’re not leaving money on the table come tax season.

Speak to Money Maximising Advisors today and get expert guidance on reducing your buy-to-let mortgage costs for 2025.

Buy-to-Let Eligibility & Lending Criteria in Ireland

When considering buy-to-let mortgages in Ireland, understanding eligibility is crucial.

- Age Requirement: Most lenders require borrowers to be at least 21 years old.

- Residency Status: You must typically be a resident of Ireland or the EU.

- Credit History: A strong credit score is preferred to qualify for competitive rates.

- Income Stability: Lenders look for stable income, whether from employment or investments.

- Rental Coverage Ratio: Rental income should usually cover at least 125% of mortgage payments.

- Deposit Requirement: Typically 20%–30% of the property’s value; higher deposits can secure better terms.

- Property Criteria: Some lenders prefer residential properties over commercial ones.

- Lender Variability: Eligibility criteria differ across lenders, so it’s important to check individual policies.

How Rental Yields Affect Your Mortgage Approval

Rental yields play a crucial role in the mortgage approval process for buy-to-let properties. Lenders want to ensure that your investment can generate sufficient income to cover mortgage repayments and other expenses.

A higher rental yield indicates a potentially profitable property. This can strengthen your application, as lenders will view you as a lower risk. They often calculate this yield by comparing your expected rental income against the property’s purchase price.

Conversely, if the projected rental yield is low, it might raise concerns about cash flow sustainability. In such cases, securing favourable terms may become challenging.

Understanding how much rent you can realistically charge is essential before applying for any investment property mortgage in Ireland. Tools like a Buy to Let Mortgage Calculator Ireland can help assess potential yields and guide your decision-making process effectively.

Tips to Reduce Your Buy-to-Let Mortgage Costs

- Shop Around for the Best Deals: Mortgage rates vary across lenders, so comparing offers can lead to major savings.

- Consider a Fixed-Rate Mortgage: Provides payment stability and protects you from rising interest rates.

- Increase Your Deposit: A larger deposit reduces monthly repayments and improves your chances of securing better terms.

- Check Government Schemes: Some incentives support property investors and can offer financial relief.

- Review Your Mortgage Regularly: Market changes may create opportunities to remortgage at a lower rate.

- Stay Updated on Market Trends: Being informed about Ireland’s buy-to-let trends can help you make smarter financial decisions.

Common Mistakes Investors Make (and How to Avoid Them)

Underestimating Ongoing Costs

Many investors focus only on mortgage payments and overlook expenses like repairs, maintenance, and property management fees.

Ignoring Location Dynamics

Choosing properties based solely on price can be risky; high-demand areas typically offer better rental returns.

Lack of Proper Research

Not analysing market trends or tenant demographics can lead to poor investment choices and reduced profitability.

Overlooking Legal Responsibilities

Understanding landlord obligations and local tenant laws is essential to ensure compliance and protect your investment.

Rushing Into Financing Decisions

Failing to compare mortgage options or seek professional advice can be costly. Using a Buy to Let Mortgage Calculator Ireland helps estimate expenses before committing.

Why Choose Money Maximising Advisors for Your Buy-to-Let Mortgage?

When navigating the complex world of Buy-to-Let mortgages in Ireland, having expert guidance can make all the difference. Money Maximising Advisors specialise in tailoring mortgage solutions that fit your unique financial situation.

Our deep understanding of the market allows them to identify the best deals available, ensuring you don’t miss out on competitive rates and favorable terms. Whether you’re seeking fixed or variable rate options, our insights streamline your decision-making process.

With a focus on transparency and customer service, we take time to explain intricate details. This builds confidence as you embark on your investment journey.

Additionally, their access to a range of lenders means you have more choices at your fingertips. You’ll discover bespoke advice tailored specifically for first-time landlords or seasoned investors alike.

Choosing Money Maximising Advisors empowers you with knowledge and support every step of the way in securing your ideal Buy-to-Let mortgage deal.

FAQ’S

What is a buy-to-let mortgage?

It’s specifically tailored for those looking to invest in rental properties. These loans differ from standard residential mortgages due to their focus on income generation.

How much deposit do I need?

Typically, a minimum of 20% is required. However, this can vary depending on the lender and property type.

Are there age restrictions?

Most lenders allow applicants aged 18 and older but may have upper age limits based on repayment terms.

Can I remortgage my buy-to-let property?

Yes, many landlords consider remortgaging to access better rates or additional equity for further investment opportunities.

Do all lenders provide the same interest rates?

No, rates fluctuate significantly among providers. It’s wise to compare them using a dedicated calculator or consult with experts like Money Maximising Advisors for tailored advice.

Conclusion

Navigating the landscape of buy-to-let mortgages in Ireland can seem overwhelming at first. However, by understanding the various costs associated with these investments, you will be better equipped to make informed decisions. Understanding upfront and ongoing costs is crucial for any investor looking to maximise their returns.

Eligibility requirements also vary among lenders. Knowing what each lender looks for can save time and reduce frustration during your application process. It’s important to consider how rental yields impact mortgage approval—you want to ensure that your property generates enough income to cover your financial commitments.

For those keen on minimising expenses, there are strategies available that could significantly lower your total mortgage costs over time. Avoiding common mistakes made by new investors can lead to more successful experiences in the buy-to-let sector.

Choosing Money Maximising Advisors means partnering with experts who understand the nuances of buy-to-let mortgages in Ireland, ensuring you find deals tailored specifically for you.

Call Money Maximising Advisors to secure the best mortgage rates and maximise your rental returns.