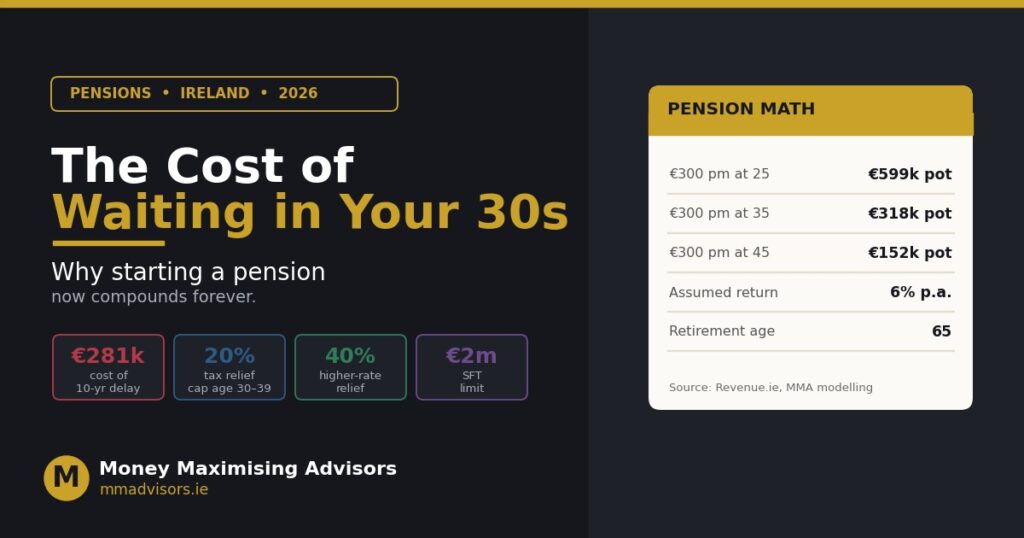

| ⚠ WHY THIS MATTERS NOW Three things changed for Irish pensions in 2026 that make starting one right now more valuable than ever. ▶ Auto-enrolment is live. Ireland’s My Future Fund launched on 1 January 2026 , if you’re an eligible employee without a workplace pension, you’re already being enrolled with employer + State top-ups. ▶ Standard Fund Threshold rising. The lifetime cap on tax-privileged pensions is scheduled to rise from €2m to €2.8m by 2029 , more headroom for early starters. ▶ Compounding runs on time, not effort. A 35-year-old starting today at €300/month retires with roughly €318,000 at 65 (6% assumed return). Wait ten years and the same contributions yield €152,000 , less than half. |

Starting a pension in Ireland is one of the most powerful , and most tax-efficient , financial decisions you will ever make. Yet most Irish adults don’t start one until they’re in their late thirties or early forties, quietly losing hundreds of thousands of euro in future retirement income to procrastination. This guide walks you through exactly how to start a pension in Ireland from a standing start , the five pension types available, the tax relief you’re entitled to, the minimum contribution levels that actually make a difference, and the practical steps from “I should probably do this” to “I have a live, tax-relieved pension”. At Money Maximising Advisors, we set up new private pensions in Ireland for clients in Dublin, Galway and every region in between , and our sister firms jcfc.ie (Donegal) and moneysense.ie (Kerry) do the same for the North West and South West.

The 6 questions every Irish pension starter asks

How do I start a pension in Ireland?

The practical steps are: (1) decide on your retirement age and target income, (2) choose your pension type (usually a PRSA if you have no employer scheme, or your employer’s occupational scheme if you do), (3) pick a provider based on charges and fund choice, (4) set a monthly contribution at a level that’s tax-efficient given your age and income, and (5) submit the application. From decision to a live, contributing pension is usually 2–4 weeks. An advisor can compress this to a single meeting.

Can anyone open a pension in Ireland?

Yes. Any Irish resident with earned income (employment, self-employment, or company directorship) can open a private pension in Ireland. You do not need employer support , a PRSA is entirely personal. Even non-earners (spouses at home with children, students) can now contribute to a PRSA in their own name, though tax relief requires earned income.

What is the best pension to start in Ireland?

For most first-time starters, a Personal Retirement Savings Account (PRSA) is the default best choice , flexible, portable and available to everyone. If your employer offers a scheme with matching contributions, join that first (the free money is unbeatable). Company directors should look at an Executive Pension for the corporate tax benefits. Self-employed workers usually use a PRSA or a self-employed personal pension.

When should I start paying into a pension?

The best time was ten years ago; the second-best time is today. Every year of delay in your twenties or thirties costs disproportionately more than a year of delay in your fifties. As a rough rule of thumb, halve your age and use that as your target contribution % , age 30 targeting 15%, age 40 targeting 20%, etc. If that’s not achievable, start anyway at whatever level you can afford; you can raise contributions annually.

How much money do I need to start a pension?

You can start a PRSA from as little as €50 per month, though most Irish providers set the practical minimum at €75–€100 per month. The key figure isn’t the euro amount , it’s the percentage of your earnings you can consistently commit for the next 20–40 years. Small monthly contributions started early beat large contributions started late, every time.

Is it worth starting a pension in Ireland?

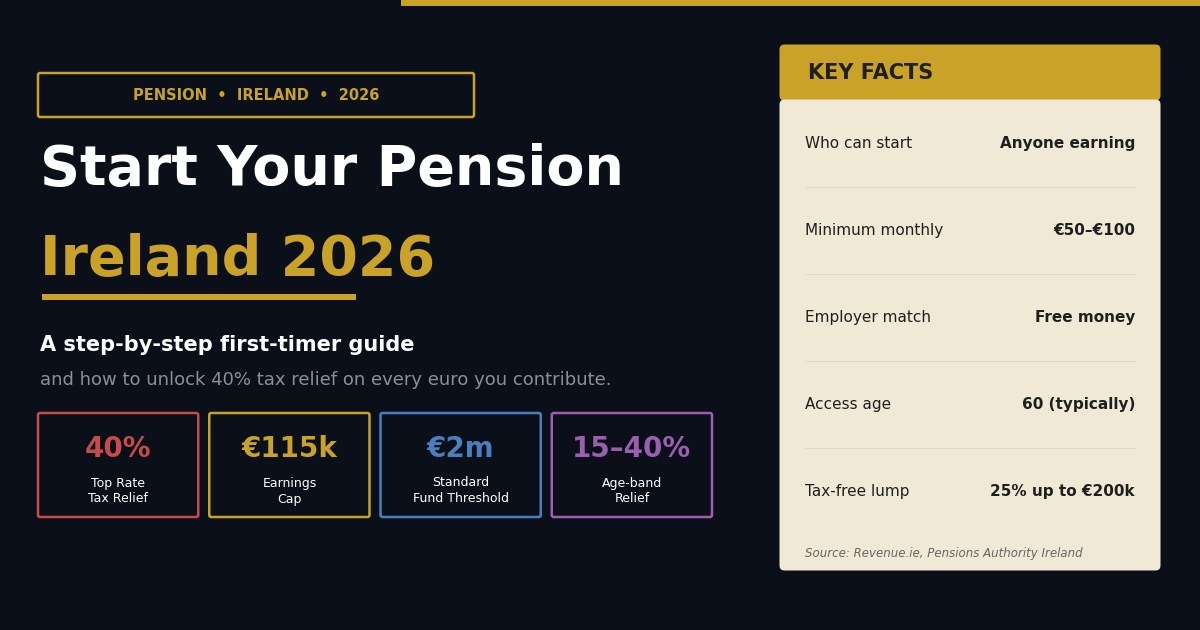

Almost always yes , the tax relief is the single biggest “instant return” available to Irish workers. A 40% higher-rate taxpayer contributing €300 per month effectively pays only €180 out of pocket , the taxman covers the rest. On top of that, pension investments grow tax-free until drawdown, and 25% (up to €200,000) can be taken as a tax-free lump sum at retirement.

Which pension type is right for you?

Five main routes into an Irish pension , the right one depends on how you earn.

PRSA (Personal Retirement Savings Account)

The most flexible and portable private pension Ireland residents can access. Available to everyone , employed, self-employed, or between jobs. Charges are capped by law on Standard PRSAs (5% of contributions plus 1% annual management fee), which keeps costs transparent. Auto-enrolment (My Future Fund) sits alongside PRSAs; you can hold both.

Occupational pension schemes

Employer-sponsored, and where employer matching contributions are available, this is almost always the first pension to fund. Every euro your employer contributes is essentially free money on top of the tax relief , a 40% taxpayer with a 5% employer match effectively gets €1.72 into their pension for every €1 they contribute out of pocket.

Executive Pension (Company Directors)

For owner-directors of Irish limited companies, an Executive Pension allows the company to contribute pre-tax profits into a director-owned pension. Corporation tax relief applies to the employer contribution, and there’s no BIK on the employee side. Contribution limits are calculated by an actuary using your age, salary and years of service, and typically allow significantly higher contributions than a PRSA , particularly useful in the final 10–15 years before retirement.

Self-employed personal pensions

Also called Retirement Annuity Contracts, these are personal pensions for the self-employed. Since PRSAs became universally available, most self-employed people now default to PRSAs for simplicity, but a self-employed personal pension can still be useful in specific circumstances (larger contributions, specialist providers).

AVCs and PRSA-AVCs

If you’re already in an occupational scheme (public or private sector) but need to boost your retirement pot, Additional Voluntary Contributions (AVCs) are the natural tool. Public sector workers particularly benefit , an AVC can bridge the gap between the reduced-service pension and a full-service pension, or fund tax-free lump-sum planning.

Tax relief , the invisible engine of every Irish pension

The reason starting a pension in Ireland is so financially powerful comes down to one word: relief. The government effectively subsidises your pension contributions by refunding the income tax on every euro you contribute, up to strict limits. Understanding these limits is the difference between an OK pension and an optimised one.

Age-based earnings-relief caps

Revenue caps how much of your earnings you can contribute with tax relief. The percentages rise with age, on the (correct) assumption that older workers need to save faster:

- Under 30: 15% of net relevant earnings

- 30–39: 20% of net relevant earnings

- 40–49: 25% of net relevant earnings

- 50–54: 30% of net relevant earnings

- 55–59: 35% of net relevant earnings

- 60+: 40% of net relevant earnings

On top of these age-band percentages, there’s an overall earnings cap of €115,000 , relief applies only to the first €115,000 of earnings, no matter how much you earn above that.

The Standard Fund Threshold

The lifetime cap on tax-privileged pension savings , called the Standard Fund Threshold , is currently €2 million, scheduled to rise incrementally to €2.8 million by 2029. For most starters, this is a distant ceiling, but it’s worth being aware of if you’re a high earner with an occupational pension plus an Executive Pension via a company you own.

| Not sure which pension type fits your situation? A 15-minute call with our team will tell you exactly which route to take , and what to contribute.→ Enquire Now | → Book an Appointment | → Contact Us |

Where you are in Ireland changes things , slightly

Pension rules are national, but access to advice, provider panels and local knowledge is regional. The MMA group covers the whole island through three complementary brands, and if you’re starting a pension, you can begin with whichever team is closest to you:

| MMA GROUP | IRELAND-WIDE COVERAGE Same regulated firm, same standards , three brands covering different regions of Ireland. |

FLAGSHIP | NATIONAL mmadvisors.ie Head office Tuam, Co Galway. Full product suite, national coverage. NORTH WEST IRELAND jcfc.ie Joe Coyle Financial Consultants, Mountcharles, Co Donegal. Business-owner and family specialists. SOUTH WEST IRELAND moneysense.ie Money Sense, Killarney, Co Kerry. 40+ years serving Munster families and pre-retirees. |

From “I should start” to “I have a pension” , 6 practical steps

The practical path from decision to a live, contributing Irish pension.

Step 1 , Set the target

Decide your target retirement age (State Pension age is 66; you can start drawing private pensions from 50 in some circumstances, 60 as standard). Model a rough monthly income you’d want in retirement , for most Irish households, €30–€50k gross per year is the comfort range for a couple.

Step 2 , Pick the pension type

PRSA if you have no employer scheme; occupational if you do (and take the match). Company directors: Executive Pension. Self-employed: usually PRSA.

Step 3 , Check your tax relief entitlement

Match your age-band % of earnings to what you can realistically contribute. Higher-rate taxpayers get 40% back; standard-rate taxpayers get 20%.

Step 4 , Choose provider and fund

Compare charges (management fee, contribution fee), fund choice (default lifestyle strategy vs self-selected), and platform quality. For most starters, a diversified default fund from a mainstream Irish provider is the right choice.

Step 5 , Set contributions and payment date

Regular monthly direct debits work best. Start at whatever level you can commit to; you can always increase later.

Step 6 , Review annually

Every year, review contribution level (up if pay rose), fund performance and any new tax relief you’re entitled to. If you get a bonus, consider a single-premium AVC top-up before Revenue’s 31 October deadline.

| CLIENT STORY How Aoife, 32, in Dublin started her first pension in 3 weeks Aoife works for a Dublin tech company that doesn’t offer a pension scheme. She was earning €72,000 and had been putting off starting a pension for four years “because it seemed complicated”. Her situation , no employer scheme, no dependants, higher-rate taxpayer , pointed directly at a PRSA. We ran the numbers together. At age 32, her tax-relief cap is 20% of earnings, giving her up to €14,400 of tax-relieved contributions per year. She committed to €500 per month (€6,000/year), well within cap. Because she’s at the 40% higher rate, her real out-of-pocket cost is €300 per month , the taxman covers the other €200 through her end-of-year tax return.Projected outcome at 65 (6% assumed net return): €635,000. If she’d waited until 42 to start, the same contributions would yield less than €300,000. The three-week set-up saved her hundreds of thousands in future retirement income. |

Common mistakes new pension starters make

✗ Waiting for the ‘right time’ to start. There isn’t one , the compounding math always favours starting now.

✗ Skipping the employer match. If your employer offers matching contributions, joining the scheme should be the first move.

✗ Contributing below the tax-relief cap without knowing. A 40% taxpayer under 30 leaving relief on the table is losing 40 cents per euro they could have claimed.

✗ Picking a pension based on brand alone. Charges and fund quality matter more than logo recognition. A 0.5% higher annual fee costs six figures over 30 years.

✗ Setting and forgetting. An annual review keeps contributions rising with income and fund choice matched to age.

✓ Starting small and building. A €100/month pension started at 25 outperforms a €400/month pension started at 45 , do what you can, when you can.

Reviewed by qualified financial advisors

| REVIEWED BY MONEY MAXIMISING ADVISORS This guide has been fact-checked and reviewed by the advisory team at Money Maximising Advisors Limited , a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland and authorised as a Multi-Agency Intermediary across the main Irish pension providers, life insurers and lenders.Our advisors hold QFA, RPA, FA and Specialist Investment Adviser (SIA) qualifications, maintain annual Central Bank-mandated CPD, and document every recommendation in a written Statement of Suitability. Verify our authorisation on the Central Bank public register at registers.centralbank.ie. Regional partners in the MMA group: jcfc.ie (Donegal / North West) and moneysense.ie (Kerry / South West). |

Related reading

| Related post | Category | Link |

|---|---|---|

| Standard Fund Threshold 2026: What It Means for Your Pension in Ireland | Pensions | Read more → |

| How Pension Advice in Ireland Saves Tax & Grows Wealth | Pensions & Tax | Read more → |

| Pension Tax-Free Lump Sum at 50 Ireland , All You Need To Know | Retirement | Read more → |

| Pension Tax Relief in Ireland: Maximise Your Benefits | Pensions | Read more → |

Before you leave , quick FAQ

Can I start a pension in Ireland if I already have an old one from a previous employer?

Yes , you can either leave the old pension where it is, or consolidate it into your new PRSA (or into a Personal Retirement Bond). Consolidation usually makes ongoing management simpler. See our Previous Pension Advice page for the specifics.

Do I still qualify for the State Pension if I have a private pension?

Yes , the State Contributory Pension is based entirely on your PRSI record, not on private pension savings. Most Irish retirees rely on both.

What happens to my pension if I move abroad?

Your Irish pension stays in Ireland and continues to grow. Depending on where you move, there are options to transfer it into an overseas equivalent scheme. Talk to our Overseas Pension Advice team before making any move.

Ready to start your Irish pension?

| Book your no-obligation pension setup consultation Our advisors will walk you through the exact steps, contribution levels and provider choice for your situation.→ Enquire Now | → Book an Appointment | → Contact Us |

Important information

Money Maximising Advisors Limited is regulated by the Central Bank of Ireland and authorised as a Multi-Agency Intermediary. All figures, tax thresholds, State Pension rates and regulatory references in this article are correct as at June 2026, based on Revenue.ie, the Pensions Authority and the Central Bank. This article is for general information only and does not constitute financial, tax or legal advice. Individual circumstances vary; you should seek personalised advice from a Qualified Financial Advisor before making any pension, protection, investment or estate-planning decision. Pension projections are illustrative only and depend on contribution level, investment performance and charges. Past performance is not a reliable indicator of future results. The value of pension investments can go down as well as up.