Inheritance tax in Ireland affects far more families than many people realise — and for blended families in particular, the rules can come as a genuine shock. Understanding the inheritance tax Ireland categories and how Capital Acquisitions Tax Ireland (CAT) applies to different relationships is essential for anyone thinking about estate planning or protecting the financial future of their loved ones.

At Money Maximising Advisors Limited, our team of expert financial advisers works with families across Dublin, Galway, and throughout Ireland to help them navigate the often complex and emotionally charged area of inheritance tax planning. Whether you’re from a traditional family structure or a blended one, understanding your obligations — and your opportunities — is the first step to protecting what you’ve worked hard to build.

What Is Capital Acquisitions Tax (CAT) in Ireland?

Capital Acquisitions Tax Ireland is the tax payable on gifts and inheritances received above certain tax-free thresholds. When someone receives an inheritance or substantial gift, Revenue assesses whether the value exceeds the applicable threshold based on the relationship between the giver and the recipient. If it does, CAT tax Ireland is applied at a flat rate of 33% on the excess amount.

The key to understanding inheritance tax Ireland is knowing which Irish inheritance tax categories you fall into — because this determines your tax-free threshold and therefore how much tax you may be liable to pay.

What Are the Inheritance Tax Categories in Ireland?

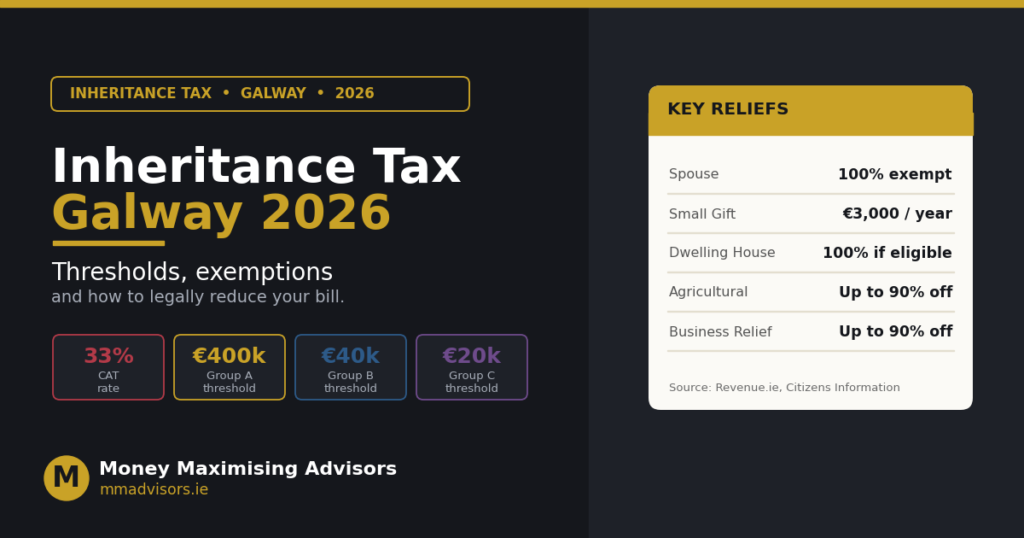

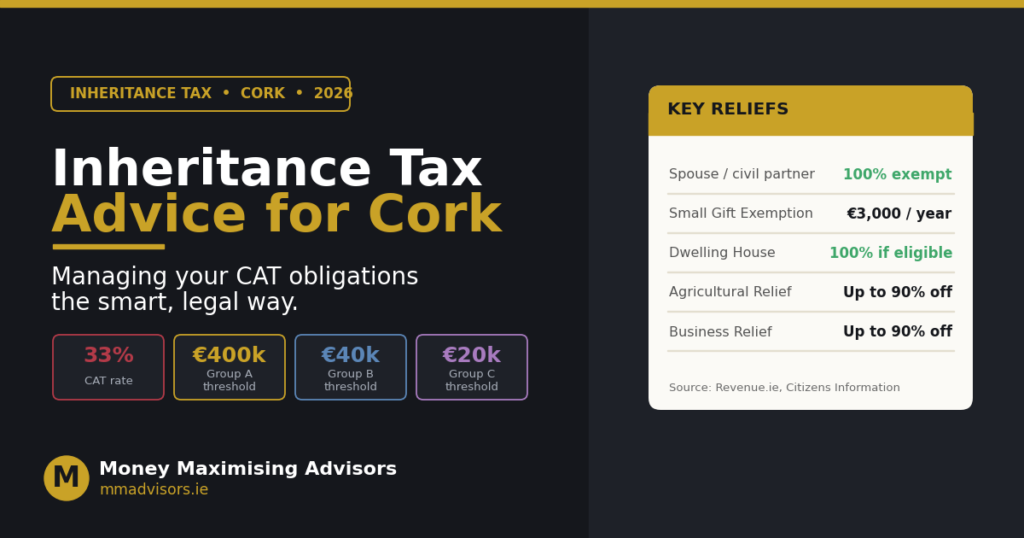

Irish inheritance tax divides beneficiaries into three distinct groups, each with its own tax-free threshold. These Irish inheritance tax categories are known as Group A, Group B, and Group C.

Group A — Parents to Children (Including Certain Step-Children)

Group A has the most generous Irish inheritance tax thresholds and applies primarily to inheritances from a parent to a child. The current Group A threshold is €335,000 (as of 2024). This means a child can inherit up to €335,000 from a parent entirely free of CAT tax Ireland.

Importantly, in some circumstances, a foster child, an adopted child, or even a stepchild may qualify for Group A thresholds — but this depends on specific legal and factual criteria. This is one of the areas where specialist inheritance tax Ireland advice is absolutely essential.

Group B — Relatives (Siblings, Nieces, Nephews, Grandchildren, etc.)

Group B applies to a broader range of family relationships, including brothers, sisters, nieces, nephews, grandchildren, and lineal ancestors other than parents. The Group B threshold is €32,500 — considerably lower than Group A, which can result in significant CAT tax Ireland liabilities for beneficiaries in this category.

For large estates, beneficiaries falling into Group B can face substantial tax bills. Proactive estate planning with the right Irish inheritance tax strategy can help mitigate this considerably.

Group C — All Others

Group C covers everyone who doesn’t fall into Groups A or B — including non-family beneficiaries, close friends, and in many cases, cohabiting partners who are not married or in a civil partnership. The Group C threshold is just €16,250.

This is particularly relevant for blended families and non-traditional family structures, where the relationships between beneficiaries and the deceased may not align neatly with the legal categories Revenue uses.

Further reading: Demystifying Inheritance Tax in Ireland: Rules and Calculations.

Inheritance Tax for Blended Families in Ireland

Blended families — those involving step-parents, stepchildren, and half-siblings — face some of the most complex inheritance tax Ireland scenarios. The inheritance tax on stepchildren Ireland rules, in particular, can create unexpected and significant tax liabilities.

Do Stepchildren Pay Inheritance Tax in Ireland?

This is one of the most frequently asked questions we receive. The answer depends on whether the stepchild has been legally adopted. In general:

- A legally adopted stepchild is treated as a natural child and qualifies for the Group A threshold of €335,000

- A non-adopted stepchild is generally treated as a stranger in blood (Group C) and would only have a threshold of €16,250

- In some cases, a stepchild who was treated as a child of the household may be able to make a case for Group A treatment — but this is fact-specific and requires careful legal and financial advice

The difference in Irish inheritance tax thresholds between Group A and Group C is enormous — €335,000 versus €16,250 — meaning the tax implications of a step-relationship can be extremely significant. For families with blended structures, this is an area that should never be left unaddressed.

Explore solutions: How a Section 73 Policy Can Reduce Inheritance Tax in Ireland.

How Much Can You Inherit Tax-Free in Ireland?

To summarise the Irish inheritance tax thresholds currently in place:

- Group A (parent to child, in most cases): €335,000

- Group B (siblings, nieces/nephews, grandchildren, lineal ancestors): €32,500

- Group C (all others, including most step-relationships and non-family): €16,250

It’s important to note that these thresholds are lifetime cumulative limits. If someone received a gift or inheritance previously, those amounts are counted against the same threshold when calculating future CAT tax Ireland liability.

Strategies to Reduce Inheritance Tax in Ireland

The good news is that with proper planning, there are effective and entirely legal strategies to reduce inheritance tax Ireland exposure. These include:

Section 72 and Section 73 Life Insurance Policies

Revenue-approved life insurance policies specifically designed to cover Capital Acquisitions Tax Ireland liabilities on death. The proceeds are payable tax-free to beneficiaries, provided the policy meets Revenue criteria.

Annual Small Gift Exemption

Each year, a person can receive gifts of up to €3,000 from any individual entirely free of CAT. Used consistently over time, this exemption can meaningfully reduce the size of a taxable estate.

Business and Agricultural Relief

Qualifying business and agricultural assets may attract 90% relief from CAT tax Ireland, significantly reducing the taxable value of these assets in an estate.

Spousal Exemption

Transfers between spouses and civil partners are exempt from inheritance tax Ireland — but this does not apply to cohabiting couples, which can create challenges in blended family situations.

Also helpful: Inheritance Tax Ireland | How To Avoid Legally.

Plan Now — Protect Your Family Later

Inheritance tax planning is not just for the very wealthy. Any Irish family with property, savings, or a business should consider how Capital Acquisitions Tax Ireland could affect those they leave behind — and take steps now to mitigate it.

Our team at Money Maximising Advisors Limited provides expert, tailored inheritance tax planning advice to families across Dublin, Galway, and the whole of Ireland. We’ll help you understand your Irish inheritance tax categories, assess your exposure, and implement the most effective strategies to protect your estate.

Contact Us to speak with an adviser, or Book an Appointment at your convenience.

Read more: Inheritance Tax Ireland – How to Reduce your Tax Burden.

Frequently Asked Questions

What are the inheritance tax categories in Ireland?

Irish inheritance tax Ireland categories are divided into Group A (parent to child), Group B (broader family including siblings, nieces, and nephews), and Group C (everyone else). Each group has a different tax-free threshold which determines how much CAT tax Ireland you may owe.

How much can you inherit tax-free in Ireland?

The current Irish inheritance tax thresholds are €335,000 (Group A), €32,500 (Group B), and €16,250 (Group C). These are lifetime cumulative limits, so prior gifts and inheritances from the same group count towards the threshold.

What is Group A inheritance tax in Ireland?

Group A applies primarily to children inheriting from a parent and carries the most generous threshold of €335,000. Adopted children and, in some cases, certain stepchildren may qualify for Group A treatment.

What is Group B inheritance tax in Ireland?

Group B covers siblings, nieces, nephews, grandchildren, and lineal ancestors other than parents. The tax-free threshold is €32,500 — significantly lower than Group A, which can lead to material Capital Acquisitions Tax Ireland liabilities on larger inheritances.

What is Group C inheritance tax in Ireland?

Group C applies to all other beneficiaries — including non-family members, friends, and most step-relationships. The threshold is just €16,250, making it the category with the highest relative tax exposure.

Do stepchildren pay inheritance tax in Ireland?

Inheritance tax on stepchildren Ireland depends on whether the stepchild has been legally adopted. Adopted stepchildren typically qualify for Group A. Non-adopted stepchildren generally fall into Group C, resulting in a much lower tax-free threshold and potentially significant tax liability.

Related reading: Gift Tax in Ireland: How Does Gift and Inheritance Tax Work?.

Conclusion

Understanding the Irish inheritance tax categories — and how Capital Acquisitions Tax Ireland applies to your specific family situation — is one of the most important things you can do to protect your loved ones. Whether you’re in a traditional family structure or navigating the complexities of a blended family, proper planning can make an enormous difference to the inheritance tax Ireland burden your beneficiaries face. At Money Maximising Advisors Limited, we’re here to help you plan effectively, legally, and compassionately.

Disclaimer

This article provides general information about Capital Acquisitions Tax and inheritance tax categories in Ireland and should not be considered personalised financial, legal, or tax advice. Irish tax laws and Revenue thresholds change periodically, and individual circumstances — particularly in blended or non-traditional family situations — vary significantly. Always consult with a qualified financial adviser or tax professional before making inheritance tax or estate planning decisions.