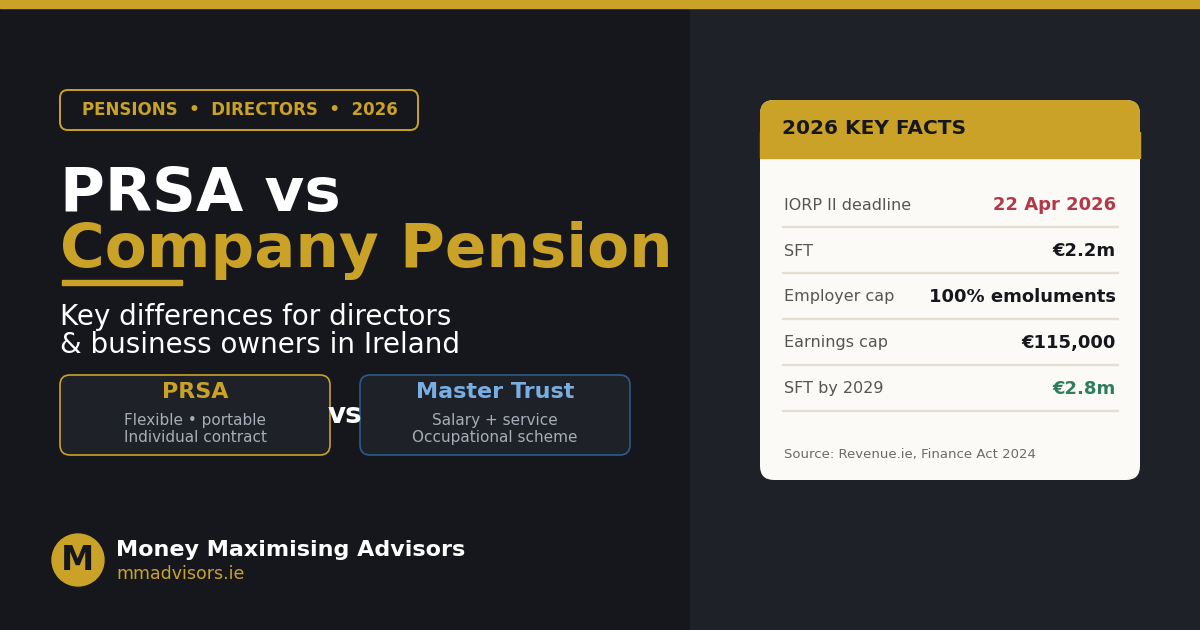

If you run a company in Ireland or sit on its board as a director, your pension structure carries real weight, it dictates how much can be contributed each year, what comes out tax-free at retirement, what happens to the fund on death, and how much regulatory overhead you have to live with. The last three years have rewritten almost every one of those answers, and the IORP II transition deadline on 22 April 2026 has just forced the issue. At Money Maximising Advisors, we work with company directors and business owners across Ireland to choose between a PRSA and a Directors Pension / Master Trust arrangement. This pillar guide sets out the key differences, the 2026 rules, and how to decide which structure suits you.

| This article sits within our Pensions hub and supports the cluster of pages directors and business owners most often visit, including Directors Pension, Pensions For The Self Employed, Occupational Pensions, Employee Pensions and Additional Voluntary Contributions (AVCs). |

What has changed in the last three years

Three legislative moves have reshaped the landscape:

- Finance Act 2022. From 1 January 2023, the benefit-in-kind charge on employer contributions to a PRSA was removed entirely, a structural change that suddenly made PRSAs viable for high-earning directors for the first time.

- Finance Act 2024. From January 2025, employer contributions to a PRSA were capped at 100% of the employee’s emoluments for the tax year, with any excess subject to BIK. For 2023 and 2024 the cap had effectively been removed altogether.

- IORP II transition. The EU’s Institutions for Occupational Retirement Provision Directive was transposed into Irish law in April 2021. Ireland chose not to exempt small one-member executive pensions, so every such scheme established before April 2021 has had to migrate to a fully compliant structure (Master Trust or PRSA) by 22 April 2026.

On top of that, the Standard Fund Threshold (SFT) began climbing again from January 2026, moving from €2 million to €2.2 million, with further €200,000 step-ups each year until it reaches €2.8 million in 2029. For higher earners that creates extra headroom to fund, but only if the right structure is in place.

What is a PRSA?

A Personal Retirement Savings Account (PRSA) is a direct contract between an individual and an approved pension provider, typically an insurance company or investment manager regulated by the Pensions Authority. Because it is personal rather than occupational, you own the contract outright. There is no trustee board to appoint, no scheme rule book to maintain, no IORP II compliance burden to carry, and no need for an employer to act as sponsor.

PRSAs were once a niche product for the self-employed, with employer contributions caught by BIK. The 2023 reforms changed that, and the 2025 cap on employer funding still leaves a meaningful annual allowance. Employee contributions remain subject to age-related tax-relief limits applied to a €115,000 earnings cap, 15% under age 30, scaling to 40% from age 60. For a clear picture of how this fits within your wider retirement plan, our Pensions Advice and Retirement Planning Advice services walk you through it in detail.

What is a company pension or Master Trust?

A company pension is an occupational pension scheme established by a trust for the benefit of employees. In recent years, most Irish employers particularly small and medium businesses have moved away from running their own single-employer scheme in favour of joining a Master Trust: a multi-employer scheme with a professional trustee board that handles governance, investment oversight, IORP II compliance and regulatory reporting on behalf of every participating employer.

Crucially, employer contributions to a Master Trust are calculated on the basis of salary and service. That gives scope to backdate funding for past years of service in a way that a PRSA simply cannot match. At retirement, the tax-free lump sum can be calculated under the older salary-and-service formula, which for directors with 20 or more years of service can reach up to one and a half times final salary, frequently larger than the 25%-of-fund figure a PRSA would produce.

PRSA vs Master Trust: the key differences at a glance

Translating that comparison into plain English: a PRSA is the lighter, more flexible vehicle, yours, portable, simple to administer, and uncapped on the death benefit (the entire fund passes to the estate). A Master Trust is the heavier, more powerful vehicle, capable of accommodating larger backdated funding and potentially a bigger tax-free lump sum, but tied to your employment relationship and governed by a trustee. The right choice depends on age, salary, years of service, what you already hold in other pension structures, and your retirement timeline.

The IORP II 2026 deadline: why this is urgent

If you established a one-member executive pension before April 2021 and have not yet transitioned it, you are now past the cut-off date. Schemes that did not migrate to a Master Trust or a PRSA by 22 April 2026 cannot accept new contributions, cannot be updated with new investment options, and may still attract ongoing governance costs without any of the benefits.

That is not an irreversible situation, but it does need professional advice and it needs it quickly. For business owners who have not yet started a pension at all, the same decision is essentially the first one you face when sitting down to plan. Our team handles both scenarios as part of our Pensions Advice and Corporate Financial Wellness Advice services.

| Holding a pre-2021 executive pension and unsure of the next step? Book Now to talk through your options, or Enquire Now for a same-day callback. |

Who should choose a PRSA?

A PRSA tends to suit directors and business owners who:

- Place a high value on flexibility and simplicity, and would rather avoid trustee governance, scheme documentation and the administrative overhead of running an occupational arrangement.

- Want phased access to their retirement pot — you can hold multiple PRSAs and crystallise each one independently, rather than triggering everything in a single retirement event.

- Already hold a meaningful pension and are managing their position relative to the Standard Fund Threshold; the PRSA’s 25%-of-fund lump sum can sometimes produce a more tax-efficient outcome than a large occupational award.

- Prioritise death-benefit certainty — a PRSA passes its full value to the estate without an occupational scheme’s service-linked caps.

Who should choose a company pension or Master Trust?

A Master Trust tends to be the better answer when:

- You are starting your pension comparatively late and need the salary-and-service funding formula to accommodate larger backdated contributions — something a PRSA cannot deliver in the same way.

- Maximising the tax-free lump sum is a priority and you can build up the years of service to access the 1.5× final salary calculation rather than the 25%-of-fund route.

- You would rather lean on a professional trustee board for IORP II compliance, investment oversight and regulatory reporting than carry any of that yourself.

- Your business has multiple employees and you want a single, governed pension vehicle that the company can sponsor.

Why a combination can be the right answer

It is not always one or the other. A common solution for directors with longer time horizons is to combine the two: a company pension or Master Trust for employer-funded, salary-and-service contributions, plus a PRSA funded personally to capture additional flexibility, phased access and death-benefit advantages. The total across all arrangements must remain within the SFT — €2.2 million in 2026, rising to €2.8 million by 2029 — but within that headroom, the combination strategy can be both legitimate and tax-efficient. Our Pensions Advice team models this for clients in detail, including how it sits alongside Additional Voluntary Contributions (AVCs) and any Approved Retirement Funds (ARF) planned for retirement.

Standard Fund Threshold: more room to fund through 2029

The SFT timetable matters: every additional €200,000 of headroom is a meaningful funding opportunity for directors.

For high earners and seasoned company directors, the SFT trajectory is one of the most important planning levers of the next four years. The combination of a rising threshold and the post-2023 PRSA reforms means that contribution capacity in 2026, across PRSA and occupational vehicles together, is materially higher than it was even three years ago. Putting that capacity to work, year on year, is the difference between merely having a pension and having a properly funded retirement.

Structure isn’t enough: investment mandate matters too

Picking the right vehicle is only half the job. The mandate inside it, the mix of equities, bonds and cash your fund actually holds, determines the long-term outcome at least as much. Many directors arriving at retirement are auto-switched into conservative “lifestyle” options that may be too defensive given a 20 to 30-year drawdown horizon. Reviewing both your structure and your investment mandate together is the discipline we apply to every client engagement. If equities, bonds and global diversification are unfamiliar territory, our Education Seminars / Presentations cover the fundamentals, and our Money Maximising Advisors YouTube channel hosts plain-English explainers.

Most-read pension and retirement guides

If you found this useful, the most read guides we share with directors and business owners include:

- Pension Plan in Ireland: How Much Will My Pension Pay Me If I Retire at 60?

- AVC vs PRSA: Which Irish Pension Top-Up Is Right for You?

- Pension Tax-Free Lump Sum at 50 Ireland — All You Need To Know

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- AVCs Explained: Should You Make Additional Voluntary Contributions?

- Why Every Business Owner in Ireland Should Consider a Directors Pension

Related posts

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- How Pension Advice in Ireland Saves Tax & Grows Wealth

- Auto-Enrolment Pensions Ireland: Everything You Need to Know in 2026

- Your Complete Guide to Pension Planning in Ireland 2026

Frequently asked questions

How much can an employer contribute to a PRSA in 2026?

From January 2025, employer contributions to a PRSA are capped at 100% of the employee’s emoluments for the tax year. The earnings cap of €115,000 applies to age-related employee tax relief. Anything above the employer cap is treated as benefit-in-kind. Between 2023 and 2024, employer contributions to a PRSA were effectively uncapped following the Finance Act 2022 reforms.

What is the IORP II deadline and does it affect my pension?

22 April 2026 was the final deadline for executive pension schemes established before April 2021 to migrate to an IORP II-compliant structure, either a Master Trust or a PRSA. Schemes that did not transition cannot accept new contributions or be updated with fresh investment options. If you hold an affected scheme, Book Now to talk through the transition urgently.

Can I have both a PRSA and a company pension?

Yes. A common strategy for directors with longer time horizons is to combine the two: an occupational scheme or Master Trust funded by the company alongside a personally funded PRSA. The total across all arrangements must stay within the Standard Fund Threshold (€2.2 million in 2026, rising to €2.8 million by 2029).

Which gives a bigger tax-free lump sum at retirement?

It depends on your salary and service. A PRSA allows 25% of the fund tax-free. An occupational scheme or Master Trust can produce up to 1.5 times final salary tax-free for those with 20 or more years of service, typically a larger figure for long-serving directors. Modelling both options before retirement is essential.

Ready to review your structure?

Whether you are choosing a structure for the first time, transitioning an executive pension under IORP II, or considering a combined PRSA-plus-company-pension approach, our team is ready to model the options for you. Book Now for a free consultation with a Qualified Financial Advisor, or visit Money Maximising Advisors to learn more.

Important information:

Pension figures, thresholds and contribution caps cited in this article reflect the rules in force in Ireland as of 2026, including changes introduced by the Finance Acts 2022 and 2024 and the IORP II transition. Always verify current Revenue and Pensions Authority guidance before acting. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. The value of pension investments can fall as well as rise, and past performance is not a reliable indicator of future returns. You should seek personalised advice from a Qualified Financial Advisor before making any pension decision.