Galway has been one of the most dependable rental markets in Ireland for years, strong year-round demand from students at the University of Galway and ATU, a steady professional cohort across the city’s pharmaceutical, medtech and IT employers, and a tight housing stock that supports rental yields. If you are thinking about buying an investment property in Galway in 2026, the headline question for most investors is the same: what will a Buy-to-Let (BTL) mortgage actually cost, and what will the lender let me borrow? At Money Maximising Advisors, we structure these applications for Irish investors every week. This pillar guide answers the six questions investors ask us most often, then walks through how the numbers actually stack up.

| This article sits within our Mortgages hub and supports the cluster of pages our Galway investors use most often, including Buy-to-let Mortgages, SPV Mortgages, Mortgage Comparison Advice and Equity Release Mortgages. |

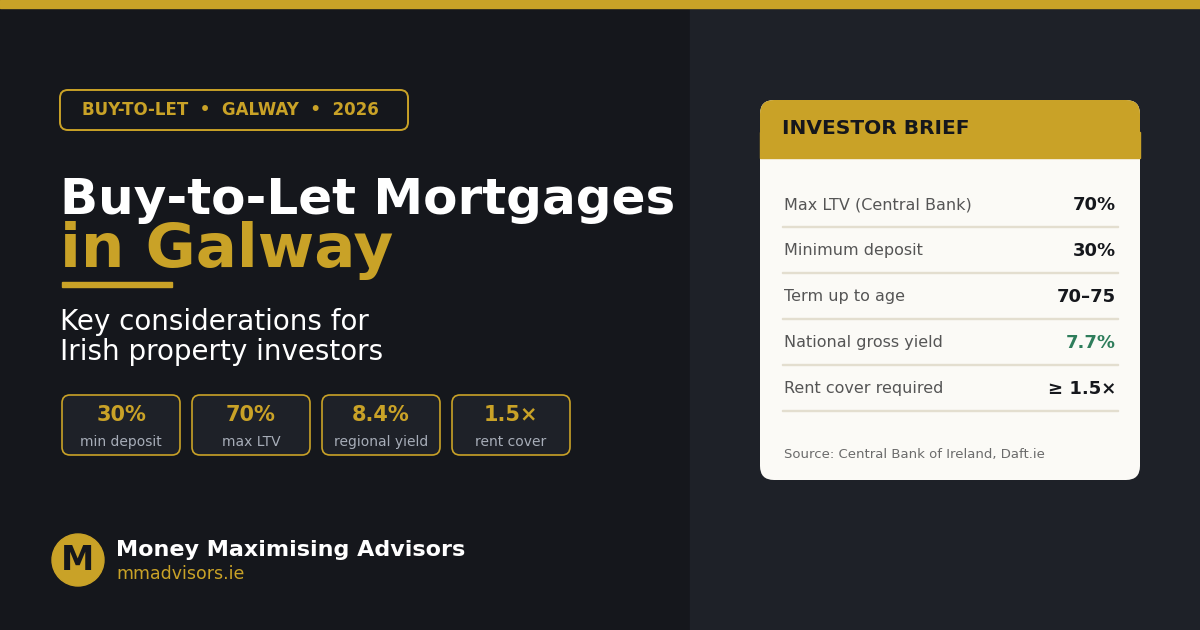

The four numbers every Galway buy-to-let investor should commit to memory.

Quick answers: the six questions every Galway investor asks

Before the deeper walk-through, here are direct answers to the questions we get most often, the same questions Google is surfacing as People Also Ask for Irish buy-to-let searches.

What is the minimum deposit for a buy-to-let mortgage in Ireland?

Under Central Bank of Ireland rules, buy-to-let lending is capped at 70% loan-to-value (LTV). That means a minimum deposit of 30% of the purchase price for most Irish investors. Some specialist lenders, and most lenders dealing with non-resident or limited-company applicants, expect 30–35%. There is no Help to Buy or First Home Scheme for investment property, those supports are for owner-occupiers only.

Can first-time buyers get a buy-to-let mortgage in Ireland?

In practice, no or at least, only very rarely. Most Irish high-street lenders will not approve a buy-to-let application from someone who has never held a residential mortgage in their own name. A small number of lenders may consider it on an exception basis if the income, deposit and property fundamentals are exceptional. If you are a genuine first-time buyer, the standard route into property is an owner-occupier mortgage first; investment property typically follows once you have a track record. See First Time Buyer Mortgages: How Much Can First Time Buyers Borrow? for the route most first-time buyers actually take.

How much can I borrow on a buy-to-let mortgage?

Up to 70% of the property’s value, subject to two affordability tests. First, the property must show enough rental yield (most lenders look for 5–6% minimum) for the rent to comfortably exceed the mortgage payment. Second, the rent has to clear an Interest Coverage Ratio (ICR) test of typically 125–145% in other words, your rent must exceed your mortgage payment by that margin. Some lenders also reference a 3.5× gross income sanity check on the applicant, but rental income is the primary driver.

What are the current buy-to-let mortgage rates in Ireland?

Buy-to-let rates in Ireland have always run higher than rates on owner-occupier mortgages because lenders treat investment property as a higher-risk loan. In 2026 the best green residential rates can start with a 3, while typical buy-to-let rates sit notably higher. Pricing also depends on whether you borrow personally or through a limited company, the BER rating of the property, the LTV bracket, and your term (interest-only options are available with some Irish lenders). Because pricing moves regularly, we will quote you live indicative rates from across the lender panel as part of any review.

Is buy-to-let property still a good investment in Ireland?

It can be a strong investment, but “good” depends entirely on the numbers and your tax position. The case for it: structurally tight Irish rental supply, robust demand in Galway from students and professionals, and the option to write off mortgage interest against rental income. The case against: rental income is taxed at your marginal income tax rate (plus USC and PRSI), Residential Tenancies Board (RTB) registration and compliance are non-negotiable, and yields can be squeezed by interest costs if rates move up. Properly modelled in your name or via an SPV, it remains a viable asset class for many Irish investors. We model the after-tax position for each property as part of our Mortgage Comparison Advice service.

What income is required for a buy-to-let mortgage?

Unlike residential mortgages, there is no Central Bank loan-to-income cap on buy-to-let lending. The Central Bank rules limit you on deposit (70% LTV) but leave affordability to the lender, which is assessed primarily through the rental income and ICR. That said, individual lenders still want to see that you have a stable personal income to cover rental voids, manage major repairs and absorb interest-rate rises. Most lenders expect to see a regular employment or business income; some apply an internal cap of 3–3.5× your gross income as a secondary check.

Why Galway makes a strong buy-to-let case

Galway’s rental market has three characteristics that have made it consistently popular with Irish investors. First, the demand side is exceptionally diverse: the University of Galway and Atlantic Technological University (ATU) together support a large, structurally renewing student population that turns over every academic year. Second, the city’s pharmaceutical, medtech and tech employers — Medtronic, Boston Scientific, Cisco and others, supply a steady stream of higher-earning professionals into the rental market. And third, supply remains tight: new-build delivery, even after the strongest national output since 2009, has not caught up with underlying demand, particularly in the city centre, Salthill, Knocknacarra and along the Oranmore commuter belt.

That tightness shows up in yields. While Dublin yields have compressed in recent years, well-located Galway apartments and houses often deliver gross rental yields comfortably in the 5–7% range high enough to clear most lender criteria with room to spare. Areas with strong yields include the city centre (one- and two-bed apartments aimed at professionals and short-let students), and family homes near schools in Knocknacarra, Renmore, Oranmore and Athenry. We discuss specific micro-markets in our Irish Property Investment in 2026: Is Buy-to-Let Still Viable? guide.

How lenders actually calculate what you can borrow

Three checks decide your borrowing capacity, in this order:

Step 1: Rental yield check

Gross rental yield is annual rent divided by purchase price, expressed as a percentage. A €300,000 Galway property generating €1,500 per month rents at €18,000 a year a gross yield of 6%. Most Irish BTL lenders want at least 5–6% before they will look at the file. Anything below that and the maths typically does not work for them, regardless of how strong your personal income is.

Step 2: Stress-tested affordability

Even where the yield looks fine at today’s rates, lenders re-run the affordability calculation at a stressed rate, typically in the 5–8% band or roughly 2 percentage points above the actual mortgage rate. The point is to confirm that the property remains viable if rates rise. A small number of newer, lower-yielding properties pass at today’s rates but fail under stress they simply do not get funded at the loan amount the investor wants.

Step 3: Interest Coverage Ratio (ICR)

Finally, lenders divide your rental income by the mortgage payment and look for 125–145%. Higher-rate taxpayers and limited-company applicants tend to land at the upper end of that range. If rent only just covers the mortgage, the deal will be marked down or declined.

Pass all three and you can borrow up to 70% of the property value. Fail any one and the lender will either reduce the loan amount until you do pass, or decline outright. We screen properties for our clients against all three tests before they go too far down the road on any particular purchase.

Personal name or limited company (SPV)?

Two routes to a Galway buy-to-let, each with different tax and lending implications.

The most strategically important decision in any Irish BTL purchase is how you hold the property. The two main options are personal ownership and a Special Purpose Vehicle (SPV), essentially a limited company set up to hold investment property.

In your personal name

This is the simplest route and how most Irish investors hold their first investment property. Setup is straightforward, the widest panel of lenders is available, and the deposit requirement sits at the standard 30%. The tax catch is significant: rental profits are taxed at your marginal income tax rate, plus USC and PRSI, which can push your effective tax bill above 50% if you are a higher-rate taxpayer. For a lower-rate taxpayer holding one or two properties, however, personal ownership remains attractive.

Through a limited company (SPV)

Holding through an SPV Mortgage structure means rental profits are taxed at the corporation tax rate rather than your personal marginal rate, typically a major saving for higher-rate taxpayers and serious portfolio investors. The trade-offs are real, though: a smaller pool of SPV-friendly lenders, slightly higher deposit requirements (often 30–35%), more demanding documentation, and the costs and admin of running a company. The structure also has knock-on implications for how you eventually extract value, dividends, salary, pension contributions or company sale. Our team works alongside our Corporate Investments and Directors Pension specialists to model the right structure for each investor.

Tax considerations for Galway landlords

Once your Galway buy-to-let is up and running, a number of tax obligations kick in. The headline items every investor needs to plan for:

- Stamp duty at purchase. 1% on the first €1 million of the property value and 2% on any portion above. Budget this on top of your 30% deposit before you go to contract.

- Income tax, USC and PRSI on rental profits. Rent is taxable income in the year it is earned, less allowable deductions. For most Irish landlords, the dominant deductions are mortgage interest, RTB registration, repairs and maintenance, agent fees and insurance.

- RTB registration. All residential tenancies must be registered with the Residential Tenancies Board within the statutory window, and re-registered annually. Failure to register can disqualify you from claiming mortgage interest relief.

- Capital Gains Tax on disposal. If and when you eventually sell, gains are taxable at the prevailing CGT rate (currently 33%) less any available reliefs.

- Local Property Tax (LPT). An annual charge based on the property’s self-assessed valuation band.

| Thinking about a Galway buy-to-let? Book Now for a free consultation, or Enquire Now and we will be in touch within one working day. |

Common mistakes to avoid

From years of structuring Irish BTL applications, the pitfalls we see most often:

- Buying before approval. In a tight Galway market, going sale-agreed before BTL approval-in-principle is in place rarely ends well.

- Stretching the yield assumption. Always model with realistic, not best-case, rent figures — lenders will check market comparables.

- Ignoring the BER. Energy rating affects running costs for your tenant and may now influence the rate you secure on the mortgage itself.

- Picking the wrong ownership structure. The personal-vs-SPV decision is far easier to get right at the outset than to unwind later.

- Skipping protection cover. Lenders insist on Mortgage Protection at drawdown, and Income Protection should be reviewed alongside.

Most-read mortgage guides

If you found this useful, these are among our most-read guides for Irish property investors:

- Investment Property in Ireland: Should You Buy in Your Own Name or Through a Limited Company?

- Irish Property Investment in 2026: Is Buy-to-Let Still Viable?

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords

- How Much Can You Borrow for a Buy-to-Let? Rental Yield, Stress Tests and Lender Criteria Explained

- Pros & Cons of Using a Limited Company (SPV) for Property Investment in Ireland

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

Explore our full range

This guide is part of our wider Mortgages hub. You can also explore our Pensions, Protection, Public Sector, Savings & Investments and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- Comparing the Best Buy-to-Let Mortgage Rates in Ireland

- Step-by-Step Guide: How to Get an Investment Property Mortgage in Ireland (Using an SPV)

- Buy-to-Let vs SPV Mortgage: What Every Irish Property Investor Should Know

- Using Company Profits to Invest in Property: A Smart Guide for Irish Business Owners

Ready to invest in Galway?

Whether you are buying your first investment property in the Galway city centre, expanding an existing portfolio across the county, or considering a switch from personal ownership to an SPV structure, our team handles the full process: lender selection, structuring, application management and protection cover. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: You may have to pay charges if you pay off a fixed-rate loan early.

WARNING: The cost of your monthly repayments may increase.

Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. Lending criteria, terms and conditions apply. Buy-to-let mortgage rates, lender criteria, Central Bank rules and tax rates change from time to time and should be verified against current sources before making a decision. You should seek personalised advice from a Qualified Financial Advisor and, where appropriate, a tax adviser, before purchasing investment property.