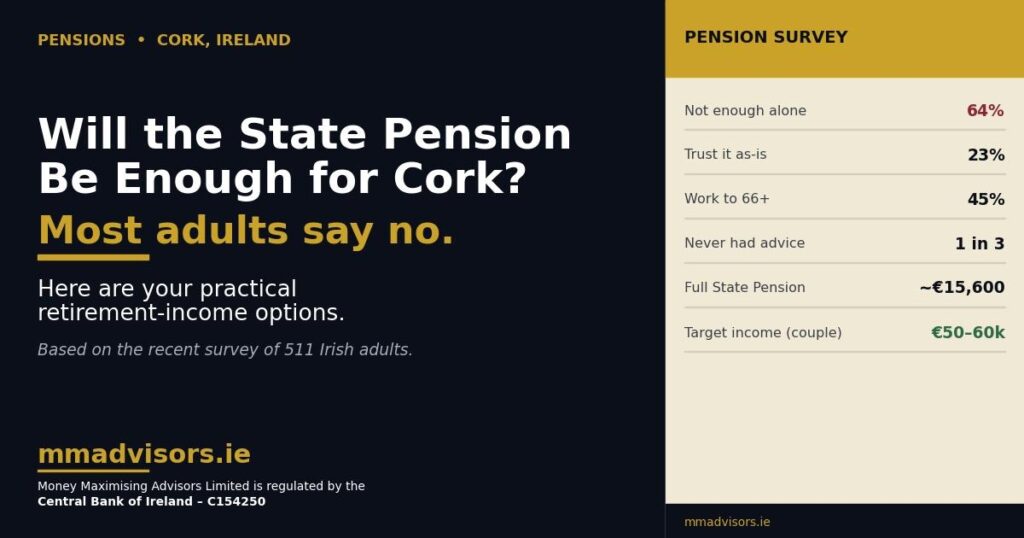

If you live in Cork and you have ever wondered, quietly, whether the State Pension will actually be enough, you are very much in the majority. A national survey of 511 adults conducted in May 2026 found that retirement confidence in Ireland has eroded sharply: most working adults now believe the State Pension alone will not see them through, many expect to work well past 66, and a sizeable share have never had any real pension advice. At Money Maximising Advisors, we sit down with Cork households every week to help them turn that anxiety into a concrete plan. This pillar guide walks you through the survey’s key findings, what they mean for a Cork-based saver, and exactly which retirement options you have if the State Pension on its own is not going to do the job.

| This article sits within our Pensions hub and supports the cluster of pages our Cork clients use most often, including Pensions Advice, Retirement Planning Advice, Additional Voluntary Contributions (AVCs), Directors Pension and Pensions For The Self Employed. |

Four headline findings from the 2026 national pension survey — the backdrop for any Cork retirement plan.

What the 2026 pension survey actually found

The data comes from askpaul’s third annual national pension survey, run in early May 2026 across 511 adults. It is not a Cork-specific study, but the picture it paints is the same one we hear from Cork households across the city, Douglas, Ballincollig, Carrigaline and beyond. People know they should be doing more. They feel the weight of that. And many simply do not know where to begin. The findings below set the scene.

The eight numbers every Cork adult should see

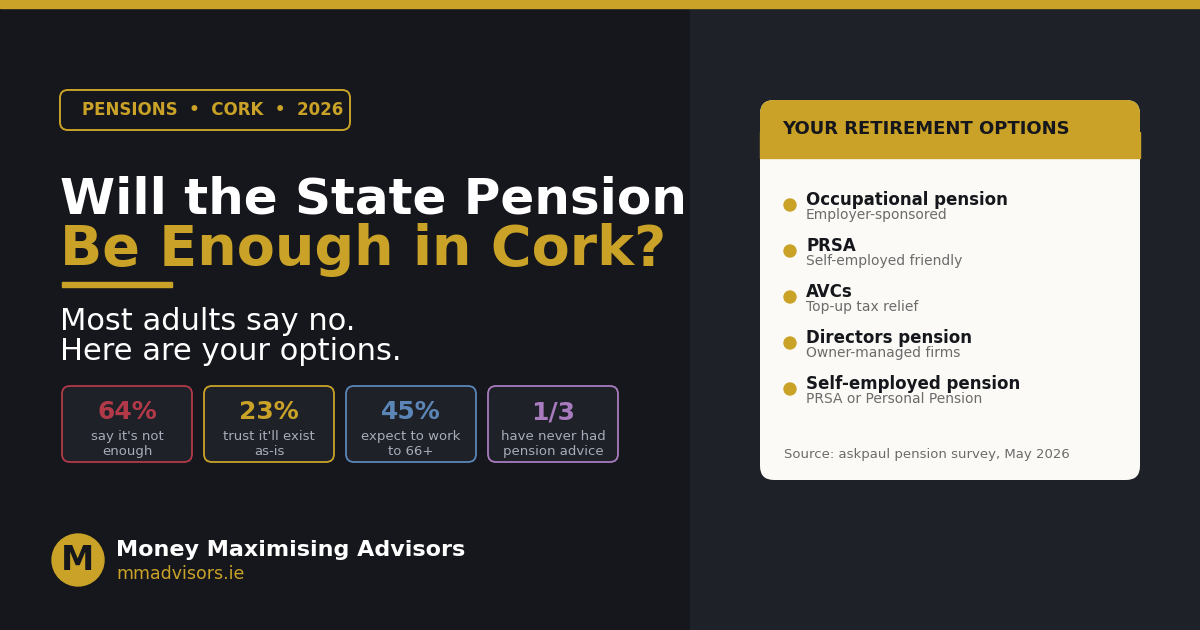

- 64% say the State Pension on its own would not be enough to live on.

Almost two thirds of respondents do not see the State Pension as a survival income, never mind a comfortable retirement. In Cork, where running costs in the suburbs and commuter belt have climbed steadily, that view is well grounded. The State Pension was always designed as a safety net, not a sole income, and the survey makes clear that the public has internalised that reality. The practical conclusion is the same one we deliver in every Pensions Advice meeting: a second, private pension is essential for almost everyone.

- Only 23% believe the State Pension will still exist in its current form when they retire.

Confidence in the longevity of the current scheme is low. Over a third expect it to be cut back or restructured, and a further 5% think it will not exist at all by the time they reach retirement age. Whether or not those expectations prove correct, planning as if the State Pension will be smaller in real terms than it is today is a sensible default. The cheaper way to be wrong is to have saved a little too much, not far too little.

- 45% expect to retire at 66 or later — and 4% never plan to retire at all.

Retirement-age expectations from the survey — the assumption of a clean exit at 66 no longer holds for almost half.

Almost half of working adults now expect to work to 66 or beyond, including 13% who anticipate working into their late 60s, 5% beyond 70, and 4% who do not expect to stop at all. Only around 10% see themselves retiring before 60. For Cork workers, that translates into a hard truth: unless you start funding earlier and harder, the choice to retire when you want is largely taken away.

- 58% say rent or mortgage costs leave little room for pension saving.

Housing is the single biggest squeeze on long-term saving. Almost three in five respondents told the survey that monthly housing costs absorb the cash that would otherwise be heading into a pension. Cork buyers are not immune, our Mortgage Comparison Advice team regularly sees households where the mortgage is well within affordability rules but leaves nothing left for retirement. The fix is rarely to slash the mortgage; it is to design pension contributions so they pull every possible euro of tax relief out of the system.

- 42% are saving something — but suspect it isn’t enough.

More than four in ten respondents have started saving for retirement but believe their contributions are inadequate. A further 11% know they should have started but have not. Together that is over half the working population running on a hunch that things will be fine, without ever properly modelling the numbers. A simple pension review, something we do in a single 60-minute session, turns that hunch into a clear projection.

- Over a third would run out of money within three months if their income stopped.

Long-term saving sits on top of short-term security, and the survey reveals just how thin that foundation is for many people. Over a third would not last three months without their primary income, 14% would not last a month, and only 17% have more than a year’s cushion. For Cork households, this is the case for layering Income Protection and, where relevant, Serious Illness Cover or Public Sector Salary Protection underneath a pension plan, not on top of it.

- A third of employees don’t know what their employer contributes to their pension.

Around one in three working adults cannot confidently state how much their employer puts into their pension each month. Another 21% have only a rough idea, and 11% have no idea at all. For Cork employees in pharmaceutical, tech and public sector roles — sectors where employer contributions can be very generous not understanding what is already arriving in your fund is leaving free money on the table. If this is you, an Occupational Pensions or Public Sector Superannuation Advice review will tell you what you have.

- A third of adults have never had any real pension advice.

Roughly one in three adults have never sat down with anyone for meaningful pension guidance. Among those who have, half found it genuinely useful, yet only 9% said embarrassment about their current savings was holding them back. The real barriers are not knowing where to go, who to trust, and whether it is too late. For most Cork adults under 60, the honest answer is that it is almost never too late, but every year of delay raises the contribution you need to make.

Your retirement options if the State Pension isn’t enough

The four main private pension vehicles available to Irish workers and business owners.

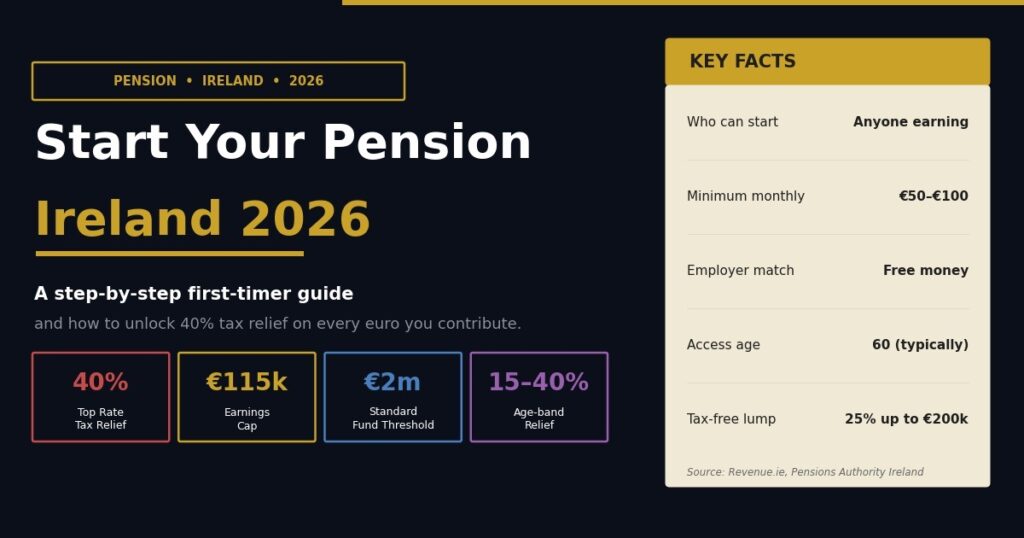

If the survey confirms that the State Pension alone will not cut it, the practical question becomes which top-up vehicle is right for you. The answer depends on your employment status, your sector and whether you own a business. The main routes are:

Occupational pension scheme

If you work for a private sector employer in Cork say in Apple, Pfizer, Stryker, EMC or any of the larger employers in Cork city or the Ringaskiddy/Little Island corridor, you may already be enrolled in a workplace scheme. The employer matches some or all of your contribution, and the State currently grants income tax relief on your portion at your marginal rate (up to limits that increase with age). Our Employee Pensions page sets out how to get the most from one.

PRSA or Personal Pension

If you do not have access to an occupational scheme, because you work for a small employer that has not yet set one up, or because you are between jobs, a Personal Retirement Savings Account (PRSA) is the most common starting point. PRSAs are portable, flexible and easy to open. If you are self-employed in Cork (a contractor, tradesperson, consultant or sole trader), see Pensions For The Self Employed for the rules that apply to you.

AVCs — Additional Voluntary Contributions

If you already have an occupational pension and want to top it up, Additional Voluntary Contributions (AVCs) let you do exactly that, with the same tax relief as your main contributions. For public sector workers in Cork, teachers, gardai, HSE staff — our Public Sector AVCs and Last Minute AVC services are specifically designed to make sure no available tax-efficient room goes unused before retirement.

Directors pension

If you are a company director in Cork, your most powerful retirement vehicle is usually a Directors Pension. Company contributions are typically a fully deductible business expense, contribution limits are generous, and the fund grows largely tax-free until drawdown. Used properly, this is often the single largest wealth-builder for owner-managed Cork businesses.

| Not sure which vehicle is right for you? Book Now for a no-obligation Cork pension review, or Enquire Now and we will be in touch within one working day. |

How much do you actually need to retire on?

There is no single magic number, but a useful Irish rule of thumb is that you will need around two thirds of your pre-retirement income each year to maintain your standard of living, including whatever the State Pension delivers. For a Cork couple on a combined €90,000, that means targeting roughly €60,000 of annual income from age 66. The State Pension covers a meaningful portion of that, but the gap of €20,000–€30,000 a year needs to come from somewhere — typically a fund built up over decades of regular contributions. Drawdown is usually a mix of a tax-free lump sum and an Approved Retirement Fund (ARF).

Common pension mistakes Cork adults should avoid

From the conversations we have every week, these are the patterns most likely to leave you short:

- Treating the State Pension as the plan. It is a foundation, not a strategy. Build a private layer on top of it from day one.

- Not knowing your employer match. If your employer matches up to 6% and you only contribute 3%, you are leaving free money behind.

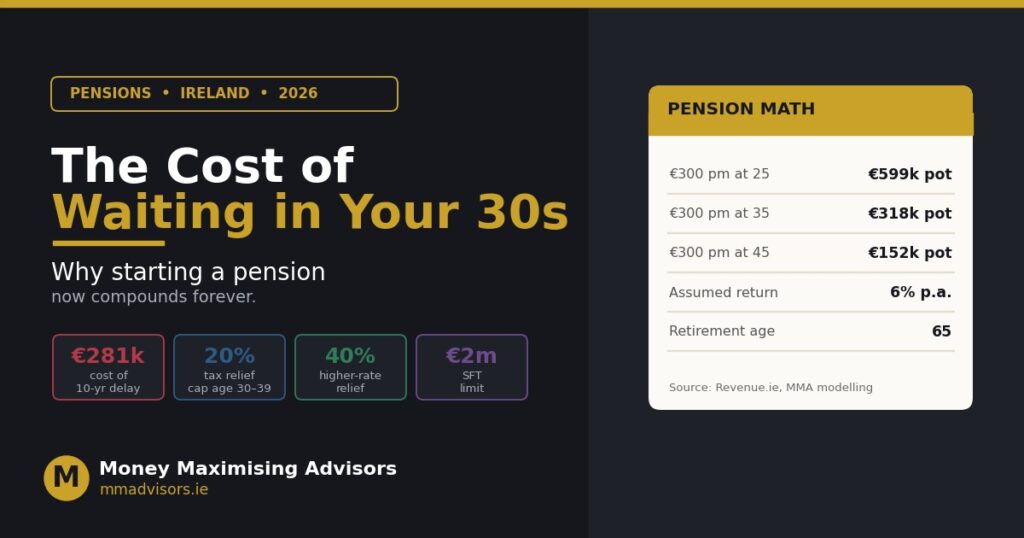

- Delaying until “things settle down”. They rarely do. Every decade of delay roughly doubles the contribution required to hit the same target.

- Ignoring AVC headroom in the run-up to retirement. The last few years before drawdown often offer the biggest tax-relief opportunities of your career.

- Skipping advice because you feel behind. The survey is clear: most people are in the same boat, and starting late beats not starting at all.

Most-read pension guides

If you found this useful, these are among our most-visited pension guides for Irish savers:

- Pension Plan in Ireland: How Much Will My Pension Pay Me If I Retire at 60?

- AVC vs PRSA: Which Irish Pension Top-Up is Right for You?

- Auto-Enrolment Pensions Ireland: Everything You Need to Know in 2026

- How Much Should I Have in Savings in Ireland?

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- How Pension Advice in Ireland Saves Tax & Grows Wealth

Explore our full range

This guide is part of our wider Pensions hub. You can also explore our Mortgages, Protection, Public Sector, Savings & Investments and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- How Pension Advice in Ireland Saves Tax & Grows Wealth

- Pension Tax-Free Lump Sum at 50 Ireland — All You Need To Know

- Early Retirement in Ireland: Your 2026 FIRE Strategy Guide

Frequently asked questions

How much is the Irish State Pension worth?

The maximum personal rate of the State Pension (Contributory) provides a meaningful base income but is widely accepted to be insufficient on its own for most working adults’ expected retirement lifestyles. Rates are reviewed each Budget. We will model your full picture, State Pension plus any private pots as part of a Cork retirement review.

Is it too late to start a pension in my 40s or 50s?

Almost never. Tax relief on contributions actually grows with age, the percentage of earnings you can claim relief on increases at age 30, 40, 50 and 60 which means later starters can often catch up faster than they expect. Our Retirement Planning Advice service is built around this scenario.

What is the difference between a PRSA and an AVC?

A PRSA is a standalone, portable pension contract that you own, typically used by those without an occupational scheme. An AVC is an additional contribution made on top of an existing occupational scheme. Both attract tax relief at your marginal rate. See AVC vs PRSA: Which Irish Pension Top-Up is Right for You? for a fuller comparison.

I have an old pension from a previous job in Cork. What should I do with it?

Leaving an old pension dormant is one of the most common mistakes we see. Depending on the scheme rules, you may be able to consolidate it into a more appropriate vehicle, take a tax-efficient lump sum at the right age, or simply rebalance the underlying funds. Our Previous Pension Advice and Pensions From Previous Employments services are designed exactly for this.

Cork? Let’s build your plan.

Whether you are starting from scratch, picking up an old workplace pension or trying to make sense of what your current employer is contributing, our team will give you a clear, no-jargon picture of where you stand and what your options are. Book Now for your free Cork pension review, or visit Money Maximising Advisors to learn more about how we work.

Important information:

Statistics cited in this article are drawn from askpaul’s third annual national pension survey, conducted via SurveyMonkey by Fairstone Asset Management DAC (trading as askpaul) between 1 and 6 May 2026, with 511 Irish respondents. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. The value of pension investments can fall as well as rise, and past performance is not a reliable indicator of future returns. You should seek personalised advice from a Qualified Financial Advisor before making any financial decision.