When it comes to building long-term financial security, few tools are as powerful — or as underutilised — as a well-structured pension. Yet many people across Ireland still haven’t fully explored what pension advice Ireland can do for them. The reality is that with the right guidance, your pension isn’t just a retirement fund — it’s one of the most effective tax-saving and wealth-building vehicles available to you today.

At Money Maximising Advisors Limited, our team of Certified Financial Planners and Qualified Financial Advisors work with individuals across Dublin, Galway, and throughout Ireland to help them unlock the full potential of pension planning. Whether you’re just starting out or reviewing an existing arrangement, expert pension advice Ireland can make a substantial difference to your financial future.

How Does Pension Tax Relief Work in Ireland?

One of the most compelling reasons to seek pension advice Ireland is the significant pension tax relief Ireland available to Irish taxpayers. In simple terms, every euro you contribute to a qualifying pension is deducted from your taxable income — meaning you pay less income tax in the year you contribute.

The level of tax relief you receive depends on your marginal rate of income tax:

- If you pay income tax at 40% (the higher rate), you get €40 back for every €100 contributed

- If you pay at the standard 20% rate, you receive €20 back per €100 contributed

This makes pension contributions tax relief one of the most straightforward ways to immediately reduce your tax bill while simultaneously growing your retirement savings. It’s genuinely a case of the government contributing towards your future — and yet many people leave this benefit entirely unused.

Is Pension Advice Worth It in Ireland?

Absolutely — and the numbers speak for themselves. Without proper pension advice Ireland, many people either contribute too little, choose unsuitable pension products, or miss key opportunities to maximise pension tax relief Ireland.

A qualified financial advisor Ireland will help you:

- Identify the right type of pension for your employment status and goals

- Maximise pension contributions tax relief within Revenue’s permitted age-related limits

- Select investment funds aligned with your risk appetite and retirement timeline

- Integrate pension planning into your broader wealth management Ireland strategy

- Plan for retirement income in the most tax-efficient way possible

Related reading: Your Complete Guide to Pension Planning in Ireland 2026: Why Now Is the Time to Secure Your Retirement.

How Can Pensions Reduce Tax in Ireland?

Beyond the immediate pension tax relief Ireland on contributions, pension planning offers several other tax advantages that make it central to any retirement planning Ireland strategy:

Tax-Free Growth

Funds held within a pension grow free of Capital Gains Tax (CGT) and income tax. This means your investments can compound more efficiently than they would in a standard savings or investment account.

Tax-Free Lump Sum at Retirement

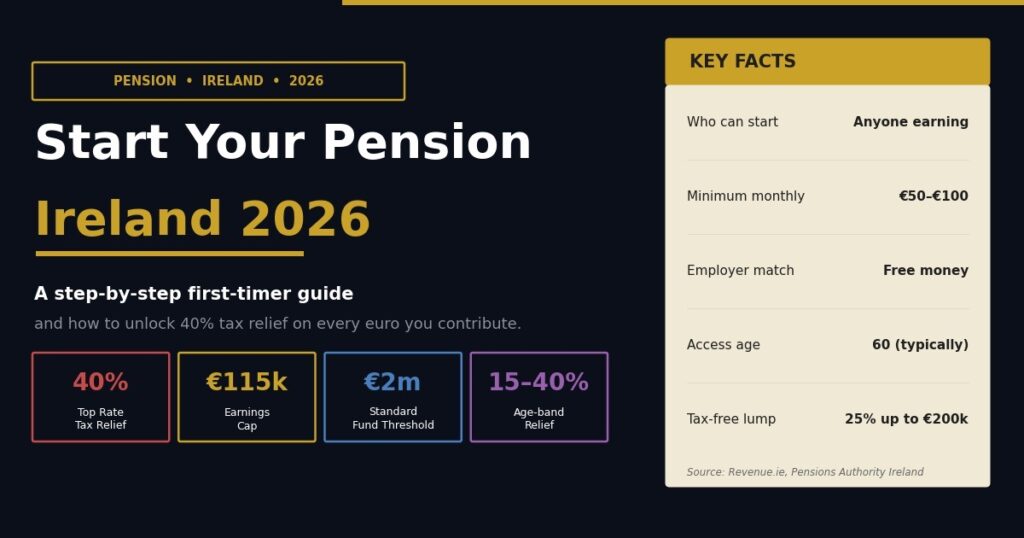

When you retire, you can take a tax-free lump sum from your pension — currently up to 25% of the fund value, subject to a lifetime limit of €200,000. This is a significant benefit that careful pension advice Ireland can help you maximise.

Income Drawdown and Tax Management

The remaining pension fund can be drawn down over retirement. With the right structure, you can manage how much taxable income you receive each year, potentially keeping yourself in lower tax bands throughout retirement.

Employer Contributions

If your employer makes contributions to your pension, these are also tax-free in your hands — effectively giving you additional tax-free pay.

Explore more: Saving Pension Plan in Ireland: The 2026 Expert Guide to Building a Secure Retirement.

What Is the Best Pension Option in Ireland?

The best pension option in Ireland depends heavily on your individual circumstances — your employment status, income level, age, and long-term financial goals. The main pension types available include:

Occupational Pension Schemes

Employer-sponsored schemes available through your workplace. Often the most cost-effective option if your employer also contributes.

Personal Retirement Savings Accounts (PRSAs)

A flexible PRSA Ireland is available to both employed and self-employed individuals. It’s portable, meaning you can take it with you if you change jobs, and offers flexible contribution levels.

Retirement Annuity Contracts (RACs)

Primarily used by self-employed individuals and those without access to occupational schemes. RACs offer full pension tax relief Ireland on contributions within Revenue limits.

Executive Pension Plans

Designed for company directors and executives, these can allow for higher contributions and greater wealth management Ireland flexibility.

A qualified financial advisor Ireland will assess your situation and recommend the most suitable structure — one that maximises your pension contributions tax relief and fits your long-term retirement planning Ireland goals.

Related article: Pension Plan in Ireland: How Much Will My Pension Pay Me If I Retire at 60?.

How Much Tax Relief Can I Claim on Pension Contributions in Ireland?

Revenue sets age-related limits on the percentage of your gross income you can contribute to a pension and claim pension tax relief Ireland on:

- Under 30: up to 15% of net relevant earnings

- 30–39: up to 20%

- 40–49: up to 25%

- 50–54: up to 30%

- 55–59: up to 35%

- 60 and over: up to 40%

These limits apply to net relevant earnings up to a current annual income cap of €115,000. It’s worth reviewing your contributions annually to ensure you’re making the most of your available pension contributions tax relief — particularly as you approach retirement age, when the limits become more generous.

Also relevant: Section 72 Pension Ireland: A Smart Guide to Tax-Efficient Retirement Planning in 2026.

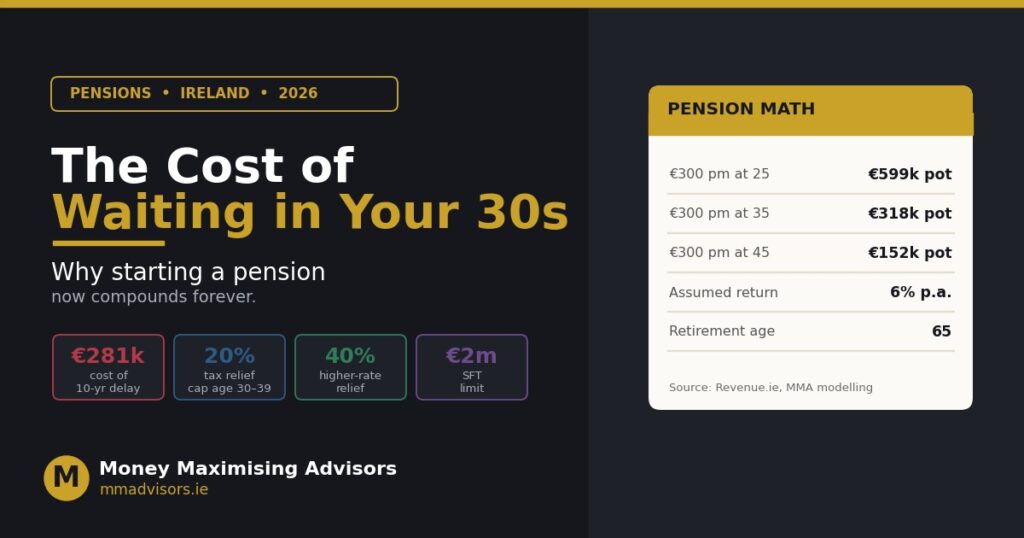

Private Pension Ireland: Why Start Now?

The single most powerful factor in private pension Ireland growth is time. The earlier you start contributing, the longer your fund has to grow — and with tax-free compounding, the difference between starting at 30 versus 40 can be hundreds of thousands of euros by retirement.

Even small, regular contributions made early will far outperform larger contributions made later. This is why the first step in any retirement planning Ireland journey should be to seek professional pension advice Ireland sooner rather than later.

Start Your Pension Journey Today

Whether you’re looking to start your first private pension Ireland, review an existing arrangement, or maximise your pension tax relief Ireland before the tax year ends, our team is ready to help.

At Money Maximising Advisors Limited, our qualified advisers will work with you to create a tailored pension planning Ireland strategy that genuinely works for your circumstances.

Contact Us to speak with an adviser, or Book an Appointment at a time that suits you.

Frequently Asked Questions

How does pension tax relief work in Ireland?

Pension tax relief Ireland allows you to deduct pension contributions from your taxable income, reducing your income tax bill at your marginal rate — either 20% or 40%. The more you contribute (within Revenue limits), the more tax you save.

Is pension advice worth it in Ireland?

Yes, professional pension advice Ireland can significantly improve your financial outcomes. An adviser helps you choose the right pension structure, maximise tax relief, select appropriate investments, and plan your retirement income efficiently.

How can pensions reduce tax in Ireland?

Pensions reduce tax in several ways — through immediate relief on contributions, tax-free growth within the fund, a tax-free lump sum at retirement, and the ability to manage taxable income drawdown in retirement.

What is the best pension option in Ireland?

The best pension option depends on your employment status, income, and goals. PRSAs, occupational schemes, RACs, and executive pensions all have different advantages. A qualified financial advisor Ireland will identify the most suitable option for you.

How much tax relief can I claim on pension contributions in Ireland?

The amount of pension contributions tax relief you can claim depends on your age — ranging from 15% of net relevant earnings for those under 30, up to 40% for those aged 60 and over. Income above €115,000 per annum is excluded.

Conclusion

Smart pension advice Ireland isn’t just about retirement — it’s one of the most effective ways to reduce your tax bill today while building lasting wealth for tomorrow. Whether you’re employed, self-employed, or a company director, there’s a pension structure that can work powerfully for you. Our team at Money Maximising Advisors Limited is here to make sure you don’t leave any pension tax relief Ireland on the table.

Disclaimer

This article provides general information about pension planning and tax relief in Ireland and should not be considered personalised financial or tax advice. Irish tax laws and Revenue limits change periodically, and individual circumstances vary. Always consult with a qualified financial adviser or tax professional before making significant pension or retirement planning decisions.