Here is something that surprises a lot of people: every time you make a pension contribution in Ireland, the government effectively pays a portion of it for you. That is not a marketing slogan — it is how pension tax relief Ireland actually works. And yet, a huge number of Irish workers are either not in a pension at all, or are contributing far less than they could be — leaving significant tax savings on the table every single year.

At Money Maximising Advisors, we help clients across Dublin, Galway, and throughout Ireland make the most of their pension in Ireland. In this guide, we explain exactly how pension tax relief Ireland 2026 works, what the limits are, and how to ensure you are not leaving free money behind.

What Is Pension Tax Relief and Why Does It Matter?

Pension tax relief is a government incentive that lets you contribute to your pension from your pre-tax income. In practical terms, this means the money that would otherwise go to Revenue in income tax instead goes directly into your pension pot, invested and growing for your retirement.

The rate of pension tax relief Ireland you receive depends on the income tax rate you pay:

- Standard rate taxpayer (20%): For every €100 you put into your pension, the actual cost to you is €80 — Revenue contributes €20

- Higher rate taxpayer (40%): For every €100 contributed, the cost to you is just €60 — Revenue contributes €40

That is an immediate, guaranteed return of 25% or 67% on your money before it has even been invested. No savings account, no stock market — just the Irish tax system working in your favour. This is why Ireland pension tax benefits are consistently described as the most powerful wealth-building tool available to Irish workers.

How Does Pension Tax Relief Work in Ireland in Practice?

Understanding how pension tax relief works in Ireland is straightforward once you see it in action.

For PAYE Employees

If you are a PAYE worker contributing to an occupational pension scheme, your contributions are typically deducted from your gross salary before tax is calculated. This means you automatically receive tax relief at your marginal rate without needing to make a claim to Revenue. Your employer may also contribute on your behalf — and those contributions do not count against your personal tax relief limits.

For Self-Employed and PRSA Holders

If you are self-employed or contributing to a Personal Retirement Savings Account (PRSA), you pay into your pension from your net income and then claim the tax relief back through your annual tax return (Form 11 or a PAYE anytime claim). The relief is applied against your income tax bill, meaning you receive a rebate — or a reduction in what you owe Revenue — proportional to your tax rate.

PRSI and USC Do Not Qualify

It is important to note that pension tax relief Ireland applies to income tax only. Pension contributions do not attract relief against PRSI or USC. This is a common misconception — particularly among self-employed workers who are used to thinking about all three charges together.

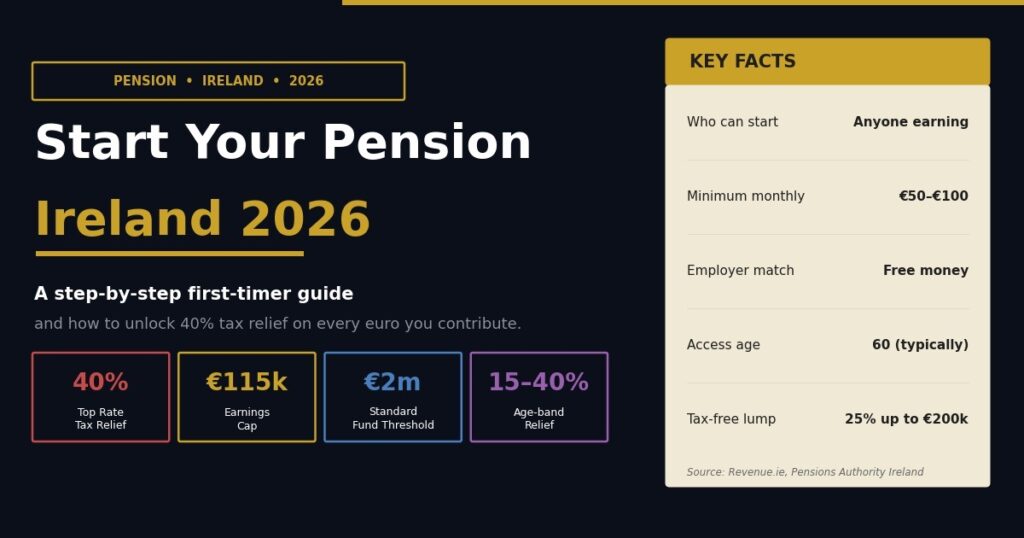

What Is the Maximum Pension Contribution in Ireland?

The amount of tax relief on pension contributions Ireland you can claim is capped based on your age and your net relevant earnings. Revenue applies age-related percentage limits on the portion of your income that qualifies for tax relief:

| Age | Max % of Net Relevant Earnings |

| Under 30 | 15% |

| 30 – 39 | 20% |

| 40 – 49 | 25% |

| 50 – 54 | 30% |

| 55 – 59 | 35% |

| 60 and over | 40% |

These percentages apply to net relevant earnings up to a maximum of €115,000 per year (the Revenue earnings cap). So even if you earn more than €115,000, your qualifying contribution for tax relief purposes is capped at that figure.

For example: a 45-year-old earning €80,000 can contribute up to 25% of €80,000 = €20,000 per year and receive full tax relief. At the 40% rate, that means Revenue effectively contributes €8,000 of that pension contribution for them.

Want to know exactly how much you could be contributing and saving in tax? Enquire Now and our pension specialists will calculate your personal maximum.

Can You Get 40% Tax Relief on Your Pension in Ireland?

Yes — if you are a higher-rate taxpayer in Ireland, you are entitled to 40% pension tax relief in Ireland on your pension contributions up to your age-based limit. This is one of the most compelling reasons to prioritise pension saving at higher income levels.

However, there is an important nuance: if your contributions bring your taxable income down below the standard rate threshold (currently €42,000 for a single person in 2026), the relief on that portion drops to 20%. For most higher earners making average contributions, this is rarely an issue — but it is worth understanding when maximising contributions close to the limit.

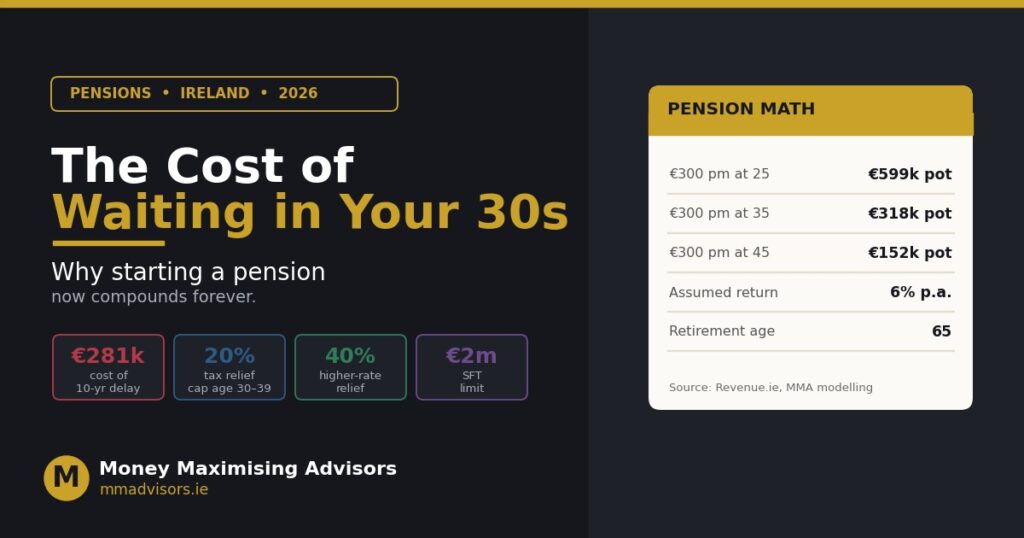

It is also worth noting that pension tax relief Ireland 2026 rules have been stable in recent years, but the government reviews contribution caps and reliefs periodically. Maximising contributions sooner rather than later is generally sound advice.

Further Reading on Pensions in Ireland

These guides from our blog offer further insight into pension planning:

- Pension Plan in Ireland: How Much Will My Pension Pay Me If I Retire at 60?

- AVC vs PRSA: Which Irish Pension Top-Up is Right for You?

- Auto Enrolment Pensions Ireland: Everything You Need to Know in 2026

- Pensions Plan Ireland: Discover the 3 A’s to Successful Savings

Keen to make the most of your pension in Ireland before the tax year ends? Book Now for a dedicated pension review session with one of our Qualified Financial Advisors.

AVCs, PRSAs, and Back-Year Contributions: Boost Your Relief Further

Many people do not realise they can make Additional Voluntary Contributions (AVCs) or PRSA contributions on top of their standard pension — and still claim full tax relief, provided they remain within their age-based limit.

Even more usefully, Revenue allows you to make a pension contribution after the end of the tax year and apply it to the previous year’s relief — provided you do so before the filing deadline (31 October, or mid-November if filing online). This means that if you underpaid in a previous year, you may still be able to claim the relief retroactively. This is a strategy many higher earners use at tax time to reduce a large income tax bill.

The rules around tax relief on pension contributions in Ireland are flexible enough to reward proactive planning — and AVCs are often the fastest way to close the gap between what you have been contributing and what you could have been contributing.

Auto-Enrolment in 2026: A New Chapter for Irish Pension Planning

Ireland’s long-awaited auto-enrolment pension scheme is now a reality in 2026. Workers aged 23–60 who earn over €20,000 per year and are not already in an occupational pension will be automatically enrolled. Crucially, this new scheme includes employer contributions and a government top-up — making it a significant new benefit for workers who previously had no pension at all.

However, the government top-up under auto-enrolment operates differently to standard pension tax relief Ireland — it is a direct top-up rather than income tax relief. For higher earners, traditional occupational pensions and PRSAs with full marginal rate tax relief will generally still be more advantageous. This is exactly the kind of planning question our advisors help clients work through.

We Also Provide

| Service | What We Offer |

| Pension Advice Ireland | Personalised pension planning for PAYE workers, self-employed, and directors |

| AVC & PRSA Planning | Maximising tax-efficient top-up contributions to your existing pension |

| Retirement Planning | Comprehensive planning for a financially secure retirement |

| Self-Employed Pensions | Tailored pension solutions for sole traders and business owners |

| Public Sector Pensions | Specialist advice on superannuation and AVC options |

| Savings & Investments | Complementary investment strategies to work alongside your pension |

Conclusion: Your Pension Is the Most Tax-Efficient Investment You Can Make

No other financial product in Ireland offers an immediate, guaranteed uplift of 20–40% the moment you put money in. Pension tax relief Ireland is genuinely one of the most powerful financial tools available — and yet far too many people in Ireland are either not using it or not maximising it.

Whether you are a PAYE worker wondering about AVCs, a self-employed professional starting a PRSA, or someone approaching retirement wanting to make a final push, the right pension in Ireland strategy can make an enormous difference to your financial future. At Money Maximising Advisors, our team of experienced Tax Advisors, Certified Financial Planners (CFP), and Qualified Financial Advisors (QFA) will help you identify and act on every opportunity available to you — across Dublin, Galway, and all of Ireland.

Contact Us for a no-obligation chat, or Book an Appointment online at your convenience and let us help you maximise your pension tax benefits in 2026.

Frequently Asked Questions

How does pension tax relief work in Ireland?

When you contribute to a pension in Ireland, those contributions are made from pre-tax income — meaning you receive income tax relief at your marginal rate (20% or 40%). For PAYE workers, this happens automatically through payroll. Self-employed workers and PRSA holders claim the relief through their annual tax return.

How much tax relief can I get on pension contributions?

You can claim income tax relief at your marginal rate — 20% or 40% — on pension contributions up to your age-based percentage limit of net relevant earnings capped at €115,000. A 40% taxpayer contributing €10,000 effectively receives €4,000 back from Revenue in tax relief.

What is the maximum pension contribution in Ireland?

The maximum qualifying contribution for pension tax relief Ireland ranges from 15% of net relevant earnings (under age 30) to 40% (age 60 and over), applied to a maximum earnings cap of €115,000 per year. Your employer’s contributions are separate and do not count towards your personal limit.

Can I get 40% tax relief on my pension?

Yes — if you pay income tax at the higher rate of 40%, you are entitled to 40% tax relief on pension contributions in Ireland up to your age-based limit. This means a €10,000 pension contribution effectively costs you just €6,000 once the tax relief is applied.

Can I make a pension contribution after the tax year ends and still claim relief?

Yes — Revenue allows back-year pension contributions, typically until 31 October of the following year (or mid-November for online filers). This is a valuable planning tool for anyone who wants to reduce a previous year’s tax bill or who received a late bonus. Pension tax relief Ireland 2026 rules continue to support this approach.

Disclaimer: This article provides general information and should not be considered personalised financial or tax advice. Pension tax relief rates, contribution limits, and Irish tax laws change periodically, and individual circumstances — including employment type, income level, and existing pension arrangements — vary. Always consult with our qualified financial advisors or tax professionals before making significant pension or financial planning decisions.