As we age, the financial landscape can become a bit daunting. Many seniors in Dublin find themselves sitting on a hidden treasure: their homes. With rising living costs and fixed incomes, it’s no wonder that more older adults are exploring options like equity release to boost their finances during retirement. Senior’s equity release is an innovative solution that allows homeowners to tap into the wealth accumulated in their properties without the hassle of moving or selling.

Imagine turning your home into a source of income! Whether you’re looking to fund travel adventures, cover unexpected medical expenses, or simply enhance your quality of life, understanding how lifetime loans work can open doors you never knew existed.

Let’s delve deeper into this financial tool designed specifically for seniors and uncover how it could potentially transform your golden years.

What is Senior’s Equity Release?

Senior’s equity release is a financial product designed to help older homeowners access the wealth tied up in their properties. It allows seniors to convert some of their home equity into cash while continuing to live in their homes.

This scheme typically involves taking out a lifetime mortgage, which enables you to borrow against your home’s value. The loan amount can be used for various purposes—whether it’s funding retirement activities or covering essential expenses.

What makes this approach appealing is that repayment usually isn’t required until the homeowner moves into long-term care or passes away. This means you can enjoy your later years without worrying about monthly repayments.

Equity release programs are tailored specifically for those aged 55 and over, ensuring they provide appropriate support during retirement. They offer flexibility and peace of mind, allowing seniors to maintain ownership of their cherished homes while accessing much-needed funds.

Understanding Equity Release for the Elderly | Lifetime Loans for Dublin Seniors

Equity release is a financial option that allows seniors to access the value locked in their homes. This can be particularly beneficial for those looking to enhance their retirement lifestyle without moving or downsizing.

Lifetime loans, a popular form of equity release, enable elderly homeowners in Dublin to borrow against their property’s value. The loan amount typically does not require monthly repayments during your lifetime, making it an attractive choice for many.

Seniors often use these funds for various purposes—home improvements, travel, or simply supplementing income. It provides flexibility and peace of mind during retirement.

Understanding how this process works is crucial. Each situation varies based on factors like age and property value. Engaging with Money Maximising Advisors can help clarify options tailored specifically to your needs and circumstances.

Benefits of a Lifetime Loan

A Lifetime Loan offers financial flexibility for seniors looking to tap into their home’s value. This can significantly enhance your quality of life during retirement.

With this loan, you’re not required to make monthly repayments. Instead, the amount borrowed is repaid when you sell your home or pass away. This feature provides peace of mind, allowing you to enjoy your funds without the stress of regular payments.

Another advantage is that it enables homeowners to maintain ownership and live in their property as long as they wish. Your house remains a cherished asset while also acting as a source of cash flow.

Additionally, many lenders allow borrowers to choose how much equity they want to release based on their needs. This customisable approach ensures that each individual can tailor the solution according to personal circumstances and goals.

Contact Money Maximising Advisors for expert, no-obligation guidance on lifetime loans.

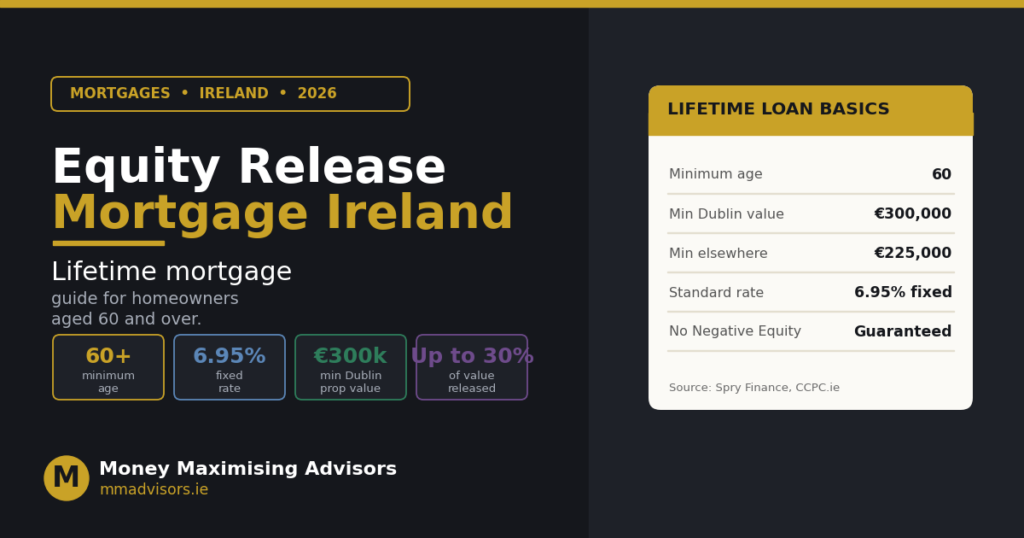

How to Qualify for a Lifetime Loan in Dublin

Qualifying for a lifetime loan in Dublin involves meeting specific criteria set by lenders.

- Generally, applicants must be at least 55 years old. This age requirement ensures that equity release options are tailored to seniors.

- Homeowners need to own their property outright or have a small mortgage remaining. The value of the home also plays a crucial role; typically, it should be worth over €100,000.

- Lenders will assess your financial situation and may look into your income and credit history. However, many focus more on the property’s value than personal finances when it comes to equity release products.

- You must live in your property as your main residence. Vacation homes or buy-to-let properties usually do not qualify for this type of financing option in Ireland.

Types of Properties Not Suitable

Certain properties may not qualify for equity release schemes. It’s essential to understand these limitations.

- Properties that are uninhabitable or require significant structural work often fall outside eligibility. Lenders typically want homes in good condition to ensure their investment is secure.

- Additionally, non-standard constructions, such as those made from timber or prefabricated materials, generally pose challenges. These types of homes can be harder to value and sell.

- Leasehold properties with short leases also face scrutiny. A lease under 70 years may deter lenders due to potential issues when it comes time to remortgage or sell the property.

- Shared ownership properties might not qualify either. Since multiple parties hold stakes in the home, this complicates the equity release process significantly.

How Much Can You Release?

The amount you can release through equity depends on various factors. Primarily, your age and the value of your property play crucial roles. Generally, older homeowners can access a higher percentage of their property’s worth.

Most providers allow you to release between 20% to 60% of your home’s market value. The specific figure often hinges on individual circumstances like health conditions or lifestyle choices.

Your home’s condition is also important. Well-maintained properties in prime locations tend to fetch more during evaluations than those requiring repairs or updates.

It’s essential to consult with professionals who can guide you through this process. They will help assess what’s feasible for your situation while ensuring all aspects are considered carefully. This tailored approach enhances financial security in retirement without compromising comfort at home.

The Application Process

The application process for seniors’ equity release is straightforward but requires careful consideration.

- First, you’ll need to choose a reputable provider who specialises in lifetime loans.

- Once you’ve selected a lender, the next step involves an initial chat about your financial situation and needs. This conversation helps determine the best options available to you.

- Following that, you’ll fill out an application form detailing your personal information and property specifics. The lender will then conduct a valuation of your home to assess its current market value.

- After this assessment, be prepared for some paperwork related to legal requirements and terms of the agreement. It’s essential to read everything carefully before signing anything.

- Once approved, funds can typically be accessed quickly—sometimes within weeks—allowing you to enjoy the benefits without delay.

Pros and Cons of Senior’s Equity Release

Equity release can be a valuable option for seniors looking to tap into their home’s value.

One major benefit is the ability to access cash without needing to move or sell your property. This can provide financial freedom, allowing for a better quality of life during retirement.

However, there are drawbacks to consider. Taking out a lifetime loan means accumulating interest over time, which reduces the inheritance left for heirs. Additionally, it may affect eligibility for certain benefits.

Another point of concern is that not all properties qualify. Homes in disrepair or those with shared ownership might face issues in approval.

It’s essential to weigh these factors carefully before deciding on equity release options—after all, what works well for one person may not suit another’s unique situation and needs.

Common Misconceptions about Senior’s Equity Release

Many seniors hesitate to explore equity release due to misconceptions.

- One common belief is that they will lose ownership of their home. In reality, with most equity release schemes, homeowners retain full ownership and can continue living in their property for as long as they wish.

- Another misconception involves the notion that only those in financial distress should consider this option. However, many individuals use seniors’ equity release simply to enhance their retirement lifestyle or fund big purchases like travel or renovations.

- Additionally, some people worry about debts accumulating over time. While interest does compound on a lifetime mortgage, it’s essential to remember that you won’t owe more than your home’s value when it comes time to repay the loan.

- There’s a fear surrounding inheritance loss. Though releasing equity may reduce what heirs receive, careful planning can mitigate these concerns while still providing immediate financial benefits.

FAQ’s About Senior’s Equity Release

Is equity release safe?

Yes, equity release schemes from reputable providers are designed to be safe. Most regulated plans ensure you retain the right to live in your home for the rest of your life.

Will I lose ownership of my home?

No. With lifetime mortgages, which are the most common type of equity release, you remain the legal owner of your home as long as you live in it.

Are there hidden fees or charges with equity release?

Costs can vary depending on the provider. While some fees are standard (like arrangement or legal fees), transparency is key. Always review the terms carefully and consult a financial advisor.

How much money can I release from my home?

The amount depends on several factors including your age, the value of your property, and the type of plan you choose. A personalised assessment will give you an accurate estimate.

Will equity release affect what I leave to my heirs?

Yes, equity release reduces the value of your estate, which can affect the inheritance you leave behind. It’s important to discuss this with a specialist advisor to fully understand the implications.

Conclusion

Navigating the world of equity release can seem complex, especially for seniors looking to make the most of their retirement years. With options like lifetime loans available in Dublin, elderly homeowners have a valuable tool at their disposal. This financial avenue allows you to tap into your home’s value while still living in it.

While there are common misconceptions about seniors’ equity release—like assuming it’s only for those struggling financially—it’s important to note that many retirees use these funds creatively and responsibly. Whether it’s taking a dream vacation or simply enhancing daily living conditions, releasing equity from your home can provide much-needed flexibility.

As you consider mortgage equity release opportunities in Ireland, consulting with experts like Money Maximising Advisors can guide you through every step of the application process and help clarify any uncertainties surrounding this option.

Call Money Maximising Advisors today to explore safe equity release options tailored for Dublin homeowners.