Discover the benefits of equity release mortgages in Ireland, including how homeowners can unlock cash from their property for renovations, debt consolidation, or to help their loved ones. This guide explores key requirements, real-life examples, and important considerations when leveraging your home’s equity.

Equity Release Mortgages in Ireland: Unlocking Financial Freedom

If you’re a homeowner in Ireland, you may be sitting on a valuable asset that could provide you with extra funds. Equity release mortgages offer an opportunity to tap into your home’s value without selling or relocating. This option is particularly appealing for those looking to consolidate debt, finance home improvements, or assist loved ones financially.

The process involves leveraging the equity built up in your property through a remortgage or loan. It’s crucial to understand both the benefits and potential risks before making this decision. As Ireland’s housing market continues evolving, many homeowners are exploring how they can make their assets work for them.

Whether it’s funding a dream renovation or clearing outstanding debts, equity release can be a smart solution tailored to your needs. Let’s delve deeper into what this financial tool entails and how it could benefit you as an Irish homeowner.

Benefits of Equity Release Mortgages

Equity release mortgages offer a host of advantages for homeowners in Ireland. One major benefit is the ability to unlock cash from your home’s value without having to sell or move out. This can provide much-needed funds for various needs, such as home improvements, medical expenses, or supporting children with a deposit on their own property.

Another key advantage is the flexibility they provide. You can choose how much equity you wish to release based on your financial situation and goals. This allows you to manage debts effectively by consolidating loans into one manageable repayment.

Additionally, equity release mortgages often come with competitive interest rates compared to traditional loans. This can result in lower monthly repayments and reduced overall costs over time.

For many individuals nearing retirement or looking at long-term financial planning, this type of mortgage provides an avenue for accessing funds while maintaining homeownership. It’s an effective way to utilise assets wisely during different life stages.

What Can You Use the Funds For?

Equity release mortgages offer homeowners in Ireland a flexible way to access the value locked in their property. The funds you obtain can serve various purposes, tailored to your needs and aspirations.

One popular use is home renovations. Transform that dated kitchen or add an extension—enhancements can boost both comfort and property value. Others choose to address medical expenses or cover educational fees, providing financial relief during important life stages.

You might also like our post on Unlocking The Potential Of Your Property: A Guide To Mortgage Equity Release For Homeowners.

Many people utilize this option for gifting loved ones with a deposit for their own homes. It’s a way of sharing wealth across generations while maintaining stability in retirement years.

Additionally, equity release can help manage inheritance tax liabilities or fund separation-related costs without selling assets hurriedly. You might even use it as a deposit on a second property or holiday home abroad, expanding your real estate portfolio seamlessly.

Some homeowners opt to consolidate short-term loans into one manageable monthly repayment through this scheme, easing financial burdens effectively.

Key Criteria to Qualify

To tap into the benefits of equity release mortgages in Ireland, meeting certain criteria is essential. First and foremost, you must own a property with sufficient equity. Typically, lenders require that your home has a loan-to-value ratio no greater than 80%.

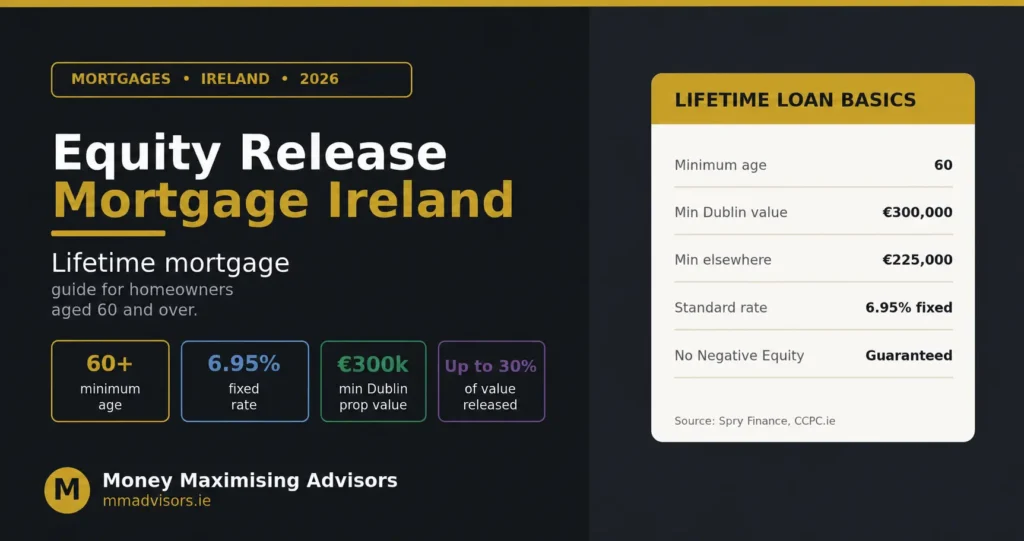

Your age also plays a crucial role; most borrowers need to be at least 55 years old. Additionally, your financial stability will be examined closely. Lenders want to see proof of income and repayment ability.

Another key factor is the property’s location and condition—it should have a minimum market value of €115,000 and be in habitable shape before funds can be released. If you’re an investor aiming to leverage multiple properties for further investments or buy-to-let opportunities, those assets must adhere to these guidelines as well.

Related read: Unlocking Home Wealth: Expert Guide To Equity Release.

Understanding these requirements enhances your chances of qualifying for this mortgage solution tailored specifically for Irish homeowners seeking flexibility in their financial planning.

Discover how to unlock your home’s value. Enquire now for tailored equity release solutions.

Key Property Requirements

When considering an equity release mortgage in Ireland, understanding the key property requirements is crucial. These criteria ensure that your home qualifies and you can access the funds you need.

Ready to discuss your financial goals? Book a consultation today and start your journey to financial freedom.

Firstly, your property must have a loan-to-value ratio of 80% or less. This means that the outstanding mortgage relative to your home’s market value should not exceed this threshold.

Additionally, for residential properties, location matters. The property must be situated in a town with a population of at least 5,000 people or more.

Your house should also have a minimum market value of €115,000. Anything below this may limit your ability to qualify for equity release options.

The condition of your property plays a significant role too. It needs to be habitable before any equity can be released; lenders want assurance that it’s in good shape overall.

Recommended: Equity Release Calculator For Buy To Let Mortgages.

Loan Amounts

When it comes to equity release mortgages in Ireland, understanding the loan amounts you can access is crucial. The amount available largely depends on several factors, including your home’s value and your financial situation.

For a Principal Private Residence, you can typically release up to 90% of its market value. This means that if your house is worth €400,000 and you have €100,000 left on the mortgage, you could potentially access up to €260,000.

On the other hand, if you’re considering buy-to-let properties as an investor or want to unlock capital from residential investment properties in smaller towns or areas outside city centers, there are specific caps based on location and property type.

It’s essential to weigh these figures against what works best for your needs. Whether it’s clearing debt or funding renovations or even helping out family members with deposits for their own homes—understanding how much equity you can tap into makes all the difference.

Terms

Understanding the terms of an equity release mortgage is crucial for any homeowner considering this financial option. The term length will often depend on your age and the lender’s policies, but it typically extends until you sell your home or pass away.

Most lenders allow you to stay in your property as long as you wish, provided that you maintain the home and keep up with any agreed-upon payments. This flexibility ensures that homeowners can enjoy their retirement without immediate pressure.

Additionally, many equity release plans offer options for repayment. Some allow interest-only payments during the life of the loan, while others add interest to the total amount owed until repayment at sale or death.

You might also like our post on Equity Release In Ireland: What You Need To Know.

Loan terms can significantly affect how much equity is released from your home and how repayments are structured. It’s essential to review all aspects closely with a trusted mortgage broker

How Much Can You Access?

One of the most compelling aspects of equity release mortgages is the ability to access a significant amount of funds from your property. The exact amount you can unlock depends on several factors, including your home’s current market value and any outstanding mortgage balance.

Typically, you can release up to 90% of your principal private residence’s value. For buy-to-let properties or investment homes, this figure may differ—usually capped at around 70%. Additionally, if you’re holding a valuable property with minimal debt against it, more options become available.

Lenders also consider your income and repayment ability. If you have strong financial health, it increases the likelihood of accessing larger sums. This makes equity release particularly attractive for those looking to consolidate debts or fund home improvements.

You’ll need to submit detailed applications outlining costs associated with renovations if that’s why you’re releasing equity. Proper planning ensures smoother approval processes and helps clarify what funds are truly accessible based on individual circumstances.

Interest Rates Available

Interest rates play a crucial role when considering equity release mortgages. In Ireland, these rates can fluctuate based on various factors such as your loan-to-value ratio and the type of property you’re leveraging.

Typically, the interest rate on equity released from your principal private residence ranges between 3% to 4.5%. This competitive rate can make accessing funds more appealing for many homeowners looking to tap into their home’s value.

For buy-to-let properties or investment homes, the scenario shifts slightly. Interest rates here tend to start around 5.35% and may go up to 5.85%. These numbers are essential for investors keen on maximising their returns while managing borrowing costs effectively.

Brokers often provide tailored advice that aligns with current market trends and individual financial profiles. It’s wise to consult them before making any decisions about refinancing or debt consolidation through an equity release mortgage; they’ll help ensure you choose the best option available in today’s dynamic market.

Take the first step towards financial flexibility. Book a consultation with our experts now.

Financial Requirements to Qualify

When considering an equity release mortgage in Ireland, understanding the financial requirements is crucial. Lenders typically assess your income and overall financial stability to determine if you qualify.

You’ll need to demonstrate adequate repayment ability. This often involves providing proof of income from employment, pensions, or other sources. Lenders want assurance that you can comfortably manage ongoing mortgage repayments.

Your credit score also plays a significant role. A solid credit history not only boosts your eligibility but may also help secure a more favourable interest rate on the equity release product.

Additionally, many lenders require a minimum disposable income after all expenses have been accounted for. This ensures you’re not overextending yourself financially when taking out an equity release loan.

Having some knowledge about your property’s market value can be beneficial as well. It aids in determining how much equity you can potentially unlock while meeting lender criteria effectively.

Curious about your options? Enquire now to learn how much equity you could access.

REAL-LIFE SCENARIOS

How One Couple Unlocked €75,000 from Their Home — Without Touching Their Savings

Imagine a couple, both teachers with a combined income of €100,000. They own a home valued at €350,000 and have an existing mortgage balance of €200,000. Over the years, they’ve built up substantial equity in their property.

Related read: Senior’S Equity Release: Lifetime Loans In Dublin.

By considering an equity release mortgage, they realised they could remortgage their home for €225,000. After paying off the current mortgage with these funds released from their house in Ireland, they were left with €75,000 in cash without dipping into their hard-earned savings.

This newfound wealth opens doors to endless possibilities—renovating their kitchen or bathroom is now within reach. They can also support their children’s education or assist them with a deposit for purchasing another property. The financial flexibility provided by releasing equity has empowered this couple to enjoy life on their terms while maintaining ownership of their cherished family home.

Turning Equity Into Opportunity: A Smart Divorce Settlement Solution

When divorce comes knocking, navigating the financial landscape can be daunting. One couple found a smart way forward using equity release mortgages in Ireland. They owned a home valued at €400,000 with €100,000 left on the mortgage.

As part of their settlement agreement, the wife was entitled to remain in the family home. The husband agreed to leave ownership but needed compensation for his share. The solution? By remortgaging through an equity release product, they accessed funds without selling their beloved home.

This approach allowed them both to move forward financially while keeping things amicable during what could have been a stressful time. Additionally, it enabled her to stay put—a critical factor for stability during such life changes.

Their story highlights how understanding your options around refinancing and leveraging property value can transform challenges into opportunities during uncertain times like separation or divorce.

Wrong or conflicting section about home improvement specialists.

Many homeowners believe that they must hire a home improvement specialist when using equity release funds for renovations. While this is often recommended, it’s not always mandatory. The choice depends on the complexity and scale of your project.

If you’re planning minor updates like painting or new flooring, you might manage these tasks yourself with adequate skills. However, structural changes or work requiring specific permits typically demand professional expertise.

Engaging a specialist can ensure quality and compliance with local regulations. They bring valuable insight into what improvements will add the most value to your property. Moreover, experienced specialists have established relationships with suppliers and subcontractors that could save both time and money.

Before deciding on hiring anyone, assess your capabilities honestly. Take an inventory of what needs doing versus what you can realistically handle yourself versus what might require specialist intervention.

Remortgage & Consolidate Loans to Reduce Monthly Repayments

Are you feeling weighed down by multiple loan repayments each month? It’s a common scenario for many homeowners. With an equity release mortgage, there’s a solution that could simplify your financial life.

By remortgaging and consolidating your existing loans into one manageable payment, you can potentially reduce your monthly financial burden. This approach allows you to streamline various debts such as personal loans or credit cards into just one mortgage repayment.

For example, imagine having three separate payments: a home improvement loan, a personal loan, and your current mortgage. Each comes with its own interest rate and due date—overwhelmingly complicated! By using the funds from equity release to pay off these debts, everything rolls into one package.

This not only eases stress but may also lower the overall interest being paid across all debts. It can free up some much-needed cash flow in your monthly budget.

Recommended: How Releasing Equity From Your Home Or Investment Property Can Unlock Financial Freedom.

Remortgage for a House Extension to Generate Income

Thinking about expanding your home to generate extra income? Many homeowners are leveraging equity release mortgages for this purpose. By remortgaging, you can unlock funds that facilitate a new extension. Imagine transforming unused space into a self-contained unit or rental opportunity.

This option not only increases your property’s value but also creates an additional revenue stream. Whether it’s constructing a granny flat or converting an attic, the potential is immense. Homeowners have reported significant returns from these investments, especially in areas with high rental demand.

Moreover, financing through equity released from your home means you might avoid the hassle of traditional loans and their stringent requirements. The process can be streamlined and tailored to suit individual needs.

Consider consulting with experienced brokers who understand the nuances of this approach; they can guide you through the specifics and help ensure that every step aligns with your financial health goals.

Releasing Equity to Buy a Second Property

Many homeowners dream of expanding their property portfolio, and equity release mortgages in Ireland can make this a reality. By tapping into the value of your existing home, you can secure funds that serve as a deposit for another investment.

Imagine owning a principal private residence valued at €400,000 with only €100,000 left on the mortgage. Through equity release, it’s possible to unlock up to €260,000. This amount could be used not only for personal expenses but also as leverage towards purchasing a buy-to-let property or holiday home.

The process is straightforward with broker assistance. You’ll need an accurate market value assessment on your current residence and plan how much you wish to allocate towards the new purchase. Lenders typically look favourably at applicants seeking to invest further in real estate through released equity options.

Leveraging your existing assets wisely could lead you into lucrative opportunities without draining your savings account. It’s essential to explore all avenues when considering how best to use the equity tied up in your home.

Here’s How an Investor Turned Equity Into Expansion

Imagine an investor who owns three buy-to-let properties in Ireland. Each property is valued significantly, contributing to a healthy portfolio. This individual saw an opportunity: releasing equity could fuel further investments and expansion.

By leveraging the value of their existing properties, the investor secured funds through an equity release mortgage. This move enabled them to access capital without selling any assets—an appealing strategy for those looking to grow their real estate holdings.

With additional cash on hand, they explored new ventures such as purchasing another rental property or renovating existing ones. The flexibility offered by this approach allowed them to diversify and increase passive income streams.

The freedom that comes with accessing trapped equity can open doors previously thought unattainable. Investors like this one are discovering innovative ways to grow wealth while maintaining control over their portfolio’s composition.

Frequently Asked Questions (FAQ)

1. What is an equity release mortgage?

An equity release mortgage allows you to unlock the value built up in your home without selling or moving. You can access funds for various purposes, such as renovations, education, or gifting a deposit to loved ones while still retaining ownership of your property.

2. Are equity release mortgages safe?

Yes, when managed properly through regulated lenders. At MM Advisors, we assess eligibility and repayment ability before recommending this option. Our aim is to ensure you make informed decisions that align with your financial stability.

3. Is it better to remortgage or release equity?

It depends on your situation. Remortgaging can lower interest rates, while equity release gives access to cash tied up in your property. Both options have pros and cons based on individual needs.

4. Can I use home equity to clear debts?

Absolutely! Many homeowners use released equity to consolidate high-interest debts into a more manageable monthly payment plan. It’s important to consult with a broker who can guide you through the process effectively.

5. Does it cost money to release equity?

There are associated costs like valuation fees, legal expenses, and lender charges involved in releasing equity from your home. However, many brokers offer competitive packages that may offset some of these expenses over time.

6. Can I release equity as cash?

Yes, you can! Many lenders allow you to access up to €100,000 in cash for approved purposes. Smaller loans often require minimal documentation. However, for amounts over €100,000, a cost estimate is needed. If structural work is involved, planning permission is required.

7. Can equity release repay an existing mortgage?

Yes! An equity release mortgage can be used to refinance or clear outstanding mortgages on your property. This approach consolidates debt, providing a streamlined and often more manageable repayment structure.

8. Can I release equity to buy out a partner’s share?

Absolutely, equity release can facilitate buying out a partner’s share. This process is particularly useful during separation or divorce. You can use the released funds to settle ownership disputes efficiently.

9. What is the LTV for buy-to-let equity release?

The typical loan-to-value (LTV) ratio for buy-to-let equity release is up to 70%. This ratio applies to loans up to €1 million. For loans between €1–1.25 million, the LTV can drop to around 65%. If you’re releasing equity through your pension for a buy-to-let, it’s generally capped at 50%. These terms ensure that both homeowners and investors can access significant funds while maintaining manageable risk levels for lenders.

10. Is a home equity loan a good idea?

A home equity loan can be beneficial for homeowners looking to access funds tied in their property. It allows you to leverage your home’s value, which can be used for various purposes like renovations or debt consolidation.

11. Can it be repaid early?

Yes, an equity release mortgage can often be repaid early. Most lenders allow for early repayment, but it’s essential to check if there are any penalties or fees associated with doing so.

12. Is leveraging equity better than a personal loan?

Leveraging equity can offer more favourable terms compared to a personal loan. It often provides access to larger sums and lower interest rates, making it an attractive option for homeowners.

Additionally, the flexibility in repayment plans can be beneficial. Many lenders allow interest-only payments initially, which might ease financial pressure.

Conversely, personal loans are usually quicker to obtain and don’t require home valuation. However, they typically come with higher interest rates and shorter repayment periods.

In summary, leveraging home equity could be a smarter choice for significant financial needs like renovations or consolidating debt. It’s important to weigh your options based on your unique circumstances before deciding which route aligns best with your financial health and goals.

CONCLUSION

Equity release mortgages in Ireland offer a flexible and accessible way for homeowners to unlock the value in their properties. Whether you’re considering renovations, addressing financial challenges during a separation, or thinking about your retirement plans, these options provide avenues worth exploring. The ability to tap into your home’s equity can empower you with funds that might otherwise remain dormant.

Understanding the process is crucial. From knowing how much equity you can access based on your property’s value and loan-to-value requirements to evaluating potential interest rates—all contribute to making informed decisions. The journey may seem complex at first glance, but with the right guidance from experienced advisors, it becomes manageable and rewarding.

While venturing into equity release could be a strategic move towards financial freedom or investment growth, it’s essential to weigh your options carefully. Assess what suits your unique situation best—be it remortgaging for home improvements or consolidating debts under one manageable payment plan.

Take the first step towards unlocking the possibilities of your home. Get in touch with our advisors today and let Money Maximising Advisors Limited help you navigate the path to equity release.