Planning for retirement can feel like a daunting task, especially when it comes to understanding pensions in Ireland. With so many options available and various factors to consider, it’s easy to become overwhelmed. But fret not—whether you’re just starting your career or nearing retirement age, there are essential strategies that can help you secure a comfortable future.

When it comes down to it, effective pension planning hinges on three fundamental principles: amount, account, and asset. Mastering these concepts will pave the way toward building a robust pension investment strategy tailored specifically for your needs. Understanding how much to save is crucial as well as choosing the right savings vehicle and creating an asset mix that suits your attitude towards risk.

Let’s dive into the world of pensions in Ireland and explore how you can make informed decisions about your retirement investments. By focusing on these key areas, you’ll be well-equipped to maximise money from investments and ensure financial security during those golden years ahead.

Three A’s: Amount, Account, and Asset

When it comes to pensions in Ireland, the three A’s — Amount, Account, and Asset — stand as pillars of successful savings.

- Amount refers to how much you contribute toward your pension. Setting the right level of contributions is essential — too little may leave you short in retirement, while too much could put unnecessary pressure on your current finances. Striking the right balance ensures long-term growth without compromising day-to-day stability.

- Account highlights the importance of choosing the right pension structure. Whether it’s an employer-sponsored plan, a personal retirement savings account (PRSA), or another pension vehicle, the type of account you select can impact flexibility, tax benefits, and access to your funds in retirement.

- Asset focuses on where your pension contributions are invested. Diversifying across assets such as equities, bonds, and property can help manage risk and maximise potential returns. The right mix should reflect both your risk tolerance and your long-term financial goals.

Understanding these three A’s helps pave the way toward effective pension investment strategies tailored to individual needs. By prioritising them, you can work toward achieving a secure and comfortable retirement.

Amount: How Much Should You Save?

Determining how much to save for retirement can feel overwhelming. The truth is, there’s no one-size-fits-all answer. It largely depends on your lifestyle and financial goals.

A good rule of thumb is to aim for 15% of your gross income each year. This figure can include employer contributions if you have a pension plan in place.

Consider the age at which you want to retire and the life you envision during those years. Do you dream of travel or maintaining a specific standard of living? These aspirations will shape your savings target.

Break down your goal into manageable monthly contributions. Regular, consistent saving helps build momentum over time.

Don’t forget about inflation when calculating future needs; it erodes buying power. Staying informed about these factors will empower more effective planning as you move forward with your pension investment strategies.

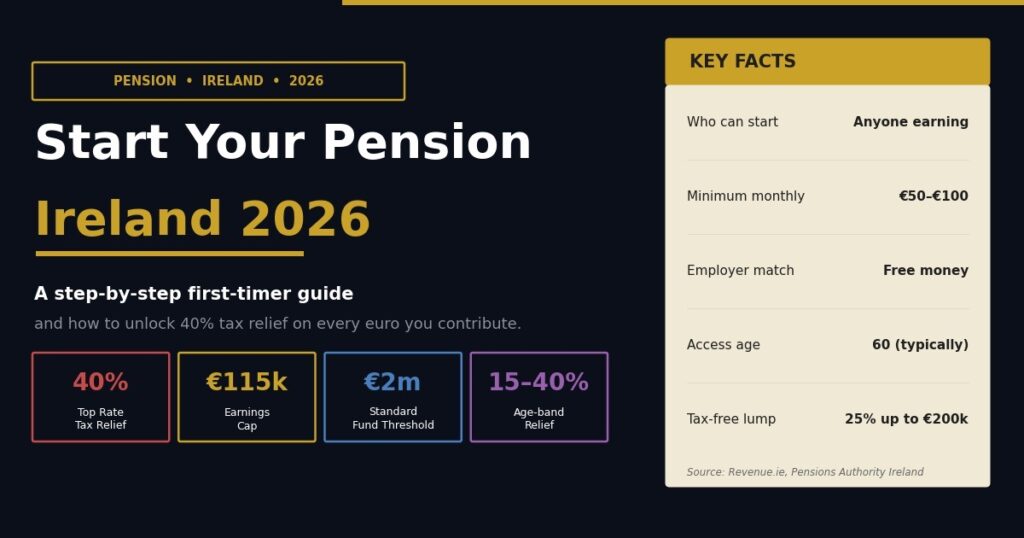

Account: Choose the Right Savings Vehicle?

Choosing the right savings vehicle is crucial for your pension plan in Ireland. With numerous options available, it can be overwhelming.

Consider a personal pension plan if you’re self-employed or want more control over your retirement investment. This allows flexibility in contributions and investment choices tailored to your goals.

For employees, an occupational pension scheme might be available through your employer. These plans often come with company contributions that can significantly boost your savings.

Another option is a PRSA (Personal Retirement Savings Account). It’s designed for those who change jobs frequently or need flexibility in their retirement planning.

Evaluate each choice carefully based on factors like fees, tax implications, and potential returns. Your decision should align with your long-term financial strategy while keeping accessibility and adequacy in mind.

Book Your Free Pension Consultation with Money Maximising Advisors – Discover how our experts can maximise your savings and tailor a plan that works for your future.

Asset Mix: Invest to Reflect Your Attitude and Situation

Your asset mix plays a crucial role in your retirement investment strategy. It’s about aligning your investments with both your risk tolerance and personal circumstances.

If you’re more conservative, you might prefer bonds or cash equivalents. These options tend to be less volatile, providing steady returns over time.

On the flip side, if you’re comfortable with some risk, consider equities or alternative assets. They can offer higher growth potential but come with increased volatility.

Life events such as marriage, children, or career changes also influence your asset allocation. Regularly assess how these factors affect your financial goals and adjust accordingly.

Consulting a Money Maximising Advisor can help tailor an approach that suits you best. Their expertise ensures your portfolio reflects not just market trends but also who you are as an investor.

Common Mistakes to Avoid When Saving for Retirement in Ireland

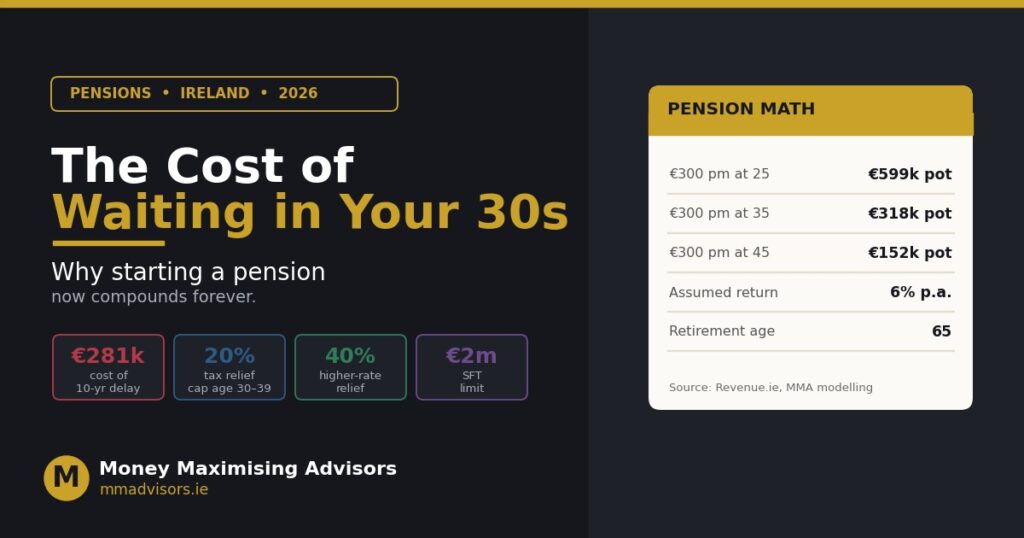

- One of the biggest pitfalls is procrastination. Many people delay starting their pension plan, hoping they can catch up later. The reality is that time is a powerful ally in building wealth.

- Another common mistake involves underestimating expenses during retirement. It’s crucial to consider rising living costs and healthcare needs when planning your savings.

- Failing to diversify investments can also be detrimental. Relying solely on one type of asset might expose you to risk as market conditions change. A balanced portfolio spreads out potential risks.

- Additionally, ignoring employer contributions can lead to missed opportunities for growth. If your workplace offers matching funds, take full advantage; it’s essentially free money for your future.

- Not reviewing your pension plan regularly may lead you off track over time. Life changes—such as new jobs or family dynamics—can impact financial goals and strategies significantly.

FAQ’S:

What are the different types of pensions available in Ireland?

In Ireland, you can choose from various pension options. These include occupational pensions provided by employers, personal retirement savings accounts (PRSAs), and public sector schemes.

How much should I contribute to my pension plan?

The right contribution varies based on individual circumstances. Many financial advisors recommend starting with 15% of your salary and adjusting as needed.

Can I access my pension before retirement age?

Accessing your pension early is generally not allowed without penalties. Exceptions exist for specific situations like serious illness or financial hardship.

Is it advisable to switch pension funds?

Switching funds may be beneficial if you’re unsatisfied with performance or fees. Always consult a Money Maximising Advisor before making changes.

What happens to my pension if I change jobs?

Your accumulated benefits can often be transferred to a new employer’s scheme or moved into a private fund, ensuring continuity in your retirement planning.

Conclusion

When considering pensions in Ireland, understanding the three A’s—Amount, Account, and Asset—is crucial for successful savings. Each aspect plays a significant role in shaping your retirement strategy.

Remember to assess how much you should save based on your lifestyle and future plans. Choosing the right pension plan ensures that your money works effectively towards your goals. It’s also essential to create an asset mix that aligns with both your risk tolerance and financial situation.

Avoiding common pitfalls can make all the difference in securing a comfortable retirement. Educate yourself about potential mistakes like underestimating expenses or neglecting diversification.

As you embark on this journey toward effective retirement investment strategies, keep these principles close at hand. Engaging with Money Maximising Advisors can provide additional support tailored to your unique circumstances.

Start Your Pension Journey Today – Let Money Maximising Advisors guide you on the right Amount, Account, and Asset strategy for a secure retirement.

More articles:

- College Education Savings Plan in Ireland: The 2025 Parent’s Guide to Smart Education Planning

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?