When it comes to passing on your wealth, understanding inheritance tax can be a daunting challenge. In Ireland, this tax can significantly impact the legacy you leave for your loved ones. Many people are unaware of how much they could owe or what strategies exist to mitigate these costs. The good news is that with proper planning and knowledge, you can navigate this complex landscape effectively.

With rising property values and growing estates, now is the perfect time to explore options that enhance financial security while ensuring peace of mind for you and your family. From Section 72 policies in Ireland to various exemptions and reliefs available under current legislation, there are numerous ways to approach inheritance planning strategically.

This guide will help demystify the intricacies of inheritance tax in Ireland and equip you with valuable insights as you prepare for the future.

What Is Inheritance Tax in Ireland?

Inheritance tax, often referred to as capital acquisitions tax (CAT), is a levy on the value of assets inherited by beneficiaries in Ireland. This tax applies when someone passes away and their estate is transferred to heirs.

The primary aim of inheritance tax is to ensure that wealth distribution remains fair while contributing to government revenue. It’s calculated based on the market value of the assets at the time of death.

In Ireland, not all inheritances are subject to this tax. The amount due depends significantly on the relationship between the deceased and the beneficiary. Close relatives generally enjoy higher exemptions compared to distant relatives or non-relatives.

For many families, understanding this framework can be challenging. Awareness of current thresholds and rates helps individuals prepare for potential liabilities when dealing with estates.

Current Inheritance Tax Rates and Thresholds (2025)

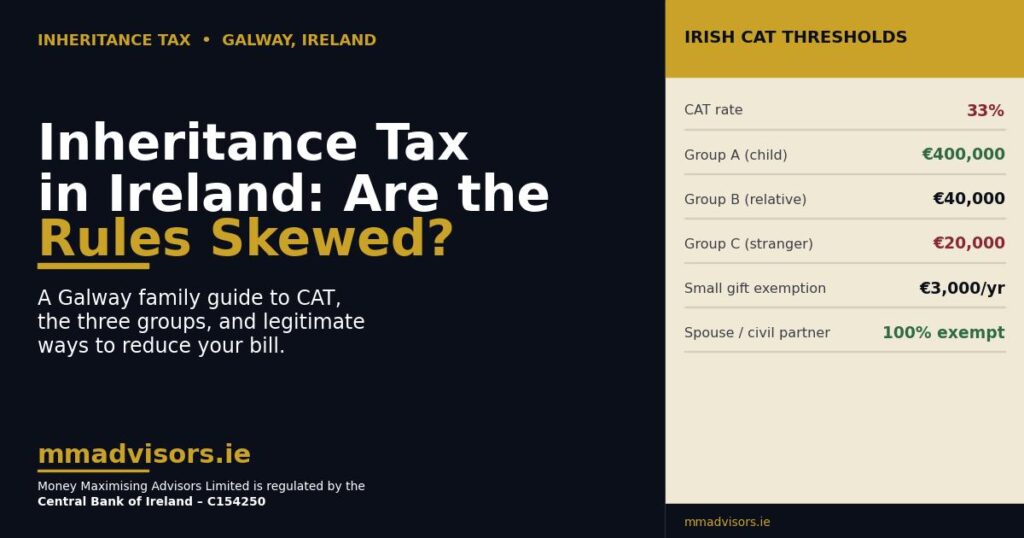

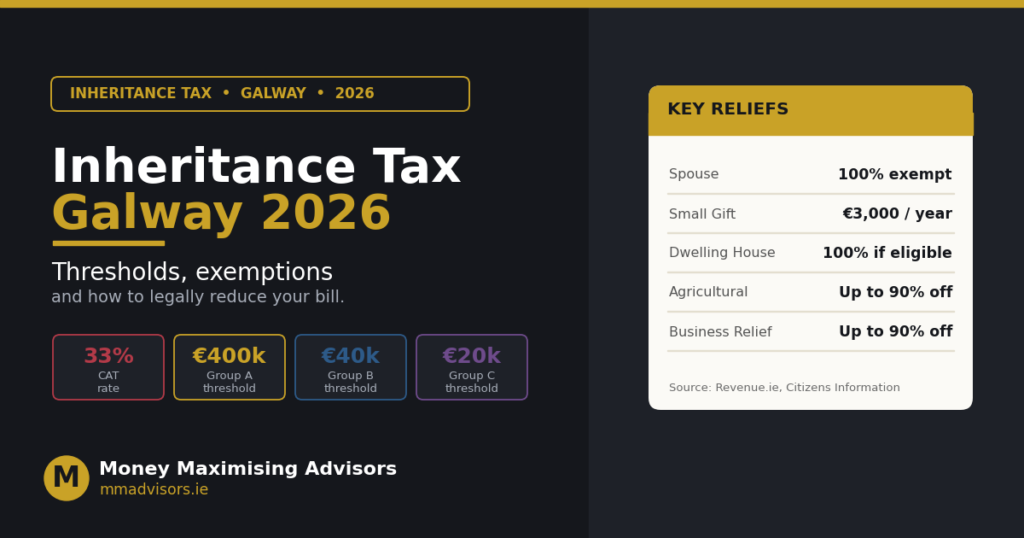

As of 2025, inheritance tax rates in Ireland remain a crucial aspect of estate planning. The standard rate applied to inheritances is currently set at 33%.

Thresholds are vital for understanding how much can be inherited before incurring taxation. For children inheriting from parents, the threshold stands at €335,000. This means that any amount exceeding this limit will be taxed at the aforementioned rate.

For siblings or more distant relatives, the threshold drops dramatically to €32,500. This significant difference underscores the importance of legacy planning and financial security.

Moreover, non-financial benefits such as emotional support and peace of mind play a critical role in effective estate management. Understanding these thresholds equips individuals with knowledge essential for informed decisions regarding their assets and family protection strategies.

How to Calculate Inheritance Tax in Ireland

Calculating inheritance tax in Ireland involves several straightforward steps.

- First, you must determine the value of the estate. This includes all assets such as property, savings, investments, and personal belongings.

- Next, identify any debts or liabilities that need to be deducted from this total. The net value is crucial for calculating taxable amounts.

- Once you have the net figure, refer to the current thresholds set by Revenue. These vary depending on your relationship with the deceased; closer relatives enjoy higher exemptions.

- After establishing your threshold category—Group A, B or C—you can then assess how much inheritance tax applies based on these rates.

- Filing for reliefs and exemptions is also essential. Certain gifts may qualify for specific allowances that can significantly reduce tax obligations when transferred to heirs.

Inheritance Tax Exemptions and Reliefs

Inheritance tax exemptions and reliefs can significantly ease the financial burden on beneficiaries. In Ireland, certain thresholds allow for tax-free inheritance under specific conditions.

For instance, transfers between spouses or civil partners are exempt from inheritance tax entirely. This ensures that families can maintain their wealth without immediate taxation upon death.

Additionally, there are various reliefs available depending on the nature of the asset passed down. Business relief allows heirs to inherit a family business with reduced tax implications, promoting continuity and stability within enterprises.

Furthermore, agricultural relief applies to farms transferred to children, ensuring that essential farming operations continue without excessive financial strain.

These exemptions play a crucial role in effective estate planning and legacy preservation. Understanding them is vital for anyone looking to protect their family’s future and enhance financial security through strategic estate decisions.

“From Section 72 policies to tailored estate planning, Money Maximising Advisors ensure your wealth is passed on efficiently and tax-effectively.”

Inheritance Tax Savings Plans and Strategies

Inheritance tax can be a considerable burden on your loved ones. However, with effective savings plans and strategies, you can mitigate this impact.

- One popular method is the Section 72 policy in Ireland. This life assurance product allows you to provide a payout that covers potential inheritance taxes when your estate is settled.

- Another approach involves making use of annual gift exemptions. By gifting small amounts each year, you reduce the value of your estate over time while providing financial support to family members.

- Consider establishing trusts as well; they serve as valuable tools for legacy planning. Trusts not only protect assets but also offer specific benefits regarding inheritance tax relief in Ireland.

- Engaging with Money Maximising Advisors can guide you through these options effectively, ensuring tailored solutions for peace of mind and financial security for your family’s future.

Benefits of an Inheritance Tax Savings Plan

An inheritance tax savings plan offers a range of benefits that can significantly enhance your financial strategy.

- One immediate advantage is the protection it provides for your heirs. By planning ahead, you ensure that more of your wealth is passed on to loved ones rather than going toward taxes.

- These plans often bring peace of mind, knowing you’ve taken steps to secure your family’s future. Financial security becomes more achievable when inheritance tax liabilities are minimised or eliminated.

- A well-structured savings plan also allows for flexibility in how assets are distributed. This can lead to better legacy planning and control over what happens with your estate after you’re gone.

- Additionally, some policies may offer non-financial benefits, such as emotional comfort for family members facing difficult decisions during an already challenging time.

With guidance from Money Maximising Advisors, creating a tailored approach becomes easier and more effective.

Common Mistakes to Avoid in Inheritance Planning

Inheritance planning can be complex, and pitfalls are common.

- Not reviewing your plan regularly – Major life events like marriage, divorce, or having children require updates to keep your estate plan valid.

- Overlooking tax implications – Many people underestimate inheritance tax rates in Ireland or miss exemptions such as the Section 72 inheritance tax relief.

- Lack of family communication – Failing to discuss your intentions can cause confusion and disputes among family members later.

- Relying on DIY solutions – Without professional advice, you may miss key opportunities to maximise tax savings and protect assets.

- Ignoring non-financial legacies – Emotional and relational aspects of your legacy are equally important; consider how your choices affect family harmony over time.

How a Financial Advisor Can Help?

Navigating inheritance tax can be complex. A financial advisor provides expertise to simplify this process.

They assess your current financial situation and future goals. This tailored approach ensures you’re on track for effective estate planning in Ireland.

Advisors stay updated on the latest laws and regulations, including specific benefits of Section 72 policies. They help identify exemptions and reliefs available to minimise your tax liability effectively.

With a focus on legacy planning, they guide you through options that maximise your family’s financial security. Their insights into non-financial benefits can also enhance peace of mind during an often stressful time.

Moreover, working with Money Maximising Advisors allows you to explore various savings plans that suit your unique needs while ensuring family protection remains a priority. With their support, you’ll make informed decisions about life assurance and other essential strategies for long-term stability.

FAQs About Inheritance Tax in Ireland

What is inheritance tax in Ireland?

It’s called Capital Acquisitions Tax (CAT) and applies to gifts or inheritances received. The beneficiary, not the estate, pays the tax.

Are there any exemptions or thresholds?

Yes. Tax-free limits depend on your relationship:

- Group A: €335,000 (children)

- Group B: €32,500 (siblings, nieces/nephews)

- Group C: €16,250 (others)

Reliefs like Dwelling House, Business, and Agricultural Relief may apply.

How is inheritance tax calculated?

The tax is 33% on the value of the estate (property, cash, investments, etc.) minus thresholds and reliefs.

Do life insurance policies affect inheritance tax?

Yes. Unless set up as a Section 72 policy, life insurance may be taxable. Section 72 plans can cover inheritance tax bills.

When should I start inheritance tax planning?

Start early to use exemptions, gifting strategies, and reliefs effectively. Early planning ensures smoother wealth transfer.

Conclusion

Inheritance tax can be a complex issue for many individuals and families in Ireland. Understanding the current rates, exemptions, and reliefs available is crucial in navigating this financial landscape. By exploring various inheritance tax savings plans, such as Section 72 policies, you can take significant steps towards minimising your liability.

Estate planning is not just about finances; it’s also about ensuring peace of mind for you and your loved ones. Implementing strategies that focus on both financial security and non-financial benefits will help protect your family’s future.

Engaging with Money Maximising Advisors can provide tailored advice to meet your specific needs. We guide you in creating a legacy plan that aligns with your goals while maximising any potential inheritance tax reliefs available in Ireland.

“Speak with Money Maximising Advisors for expert guidance on tax-efficient inheritance planning in Ireland.”