You may misguidedly believe that inheritance tax is a rich man’s tax that won’t affect you.

But if your property is more than €335,000, your child is liable to pay inheritance tax. The thresholds are even lower for other relationships.

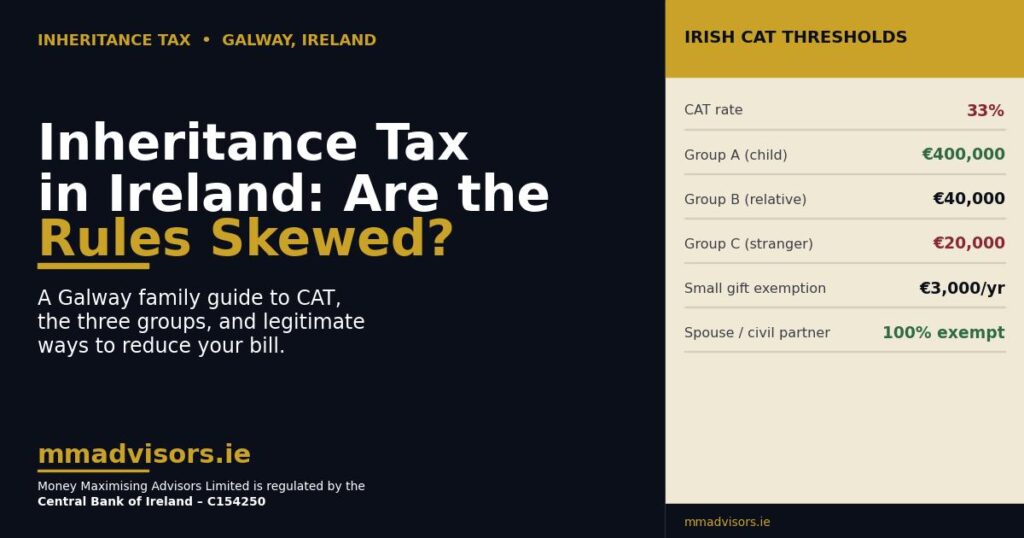

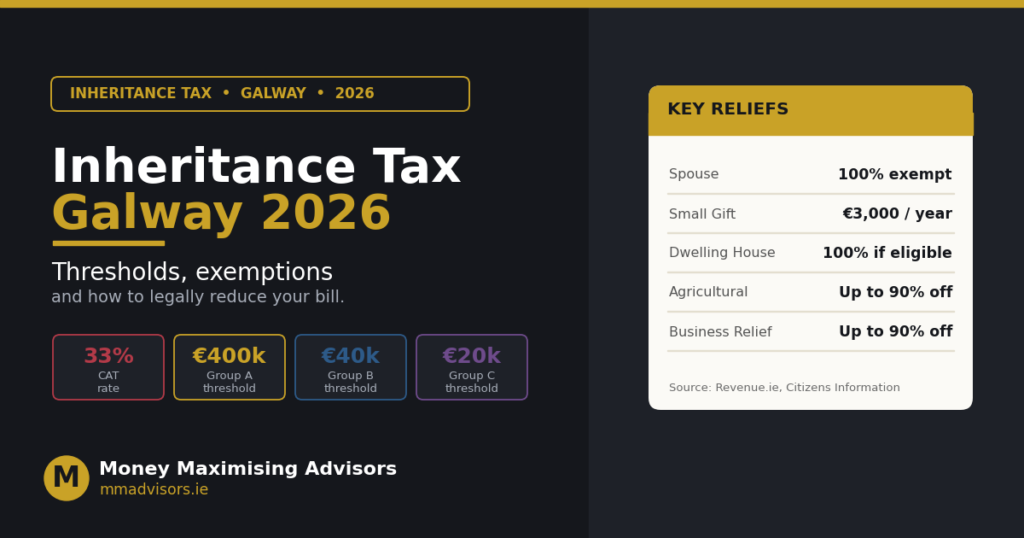

Basically, anything above these thresholds will be liable to a 33% tax payment.

Unfortunately, inheritance tax is something that we often overlook before it’s too late. And then it hits it at a time when you’re already stressed.

However, there are measures that you can put into place to reduce your potential tax liability.

This write-up deals with inheritance tax advice Dublin – how inheritance is treated and the tax implications after death when assets are being passed.

Money Maximising Advisors is a reputed financial firm that specialises in pensions advice Dublin. Their website is packed with information on this subject along with useful guides and tips.

Let’s get started….

What Is Capital Acquisition Tax (CAT)?

You may have heard the term CAT thrown around before but perhaps you’re unsure of what it exactly means. We all are eligible to receive gifts or inheritances up to a certain amount over our lifetime.

However, once it passes the thresholds, a Capital Acquisition Tax (CAT) will be applicable.

Now, CAT can be broken down into two types of tax:

- Gift Tax: This is applicable when the person giving the tax is alive.

- Inheritance Tax: This is applicable when the person giving the gift has passed away.

“In 2024, the current rate of Inheritance tax in Ireland is 33%”

Who Is Liable To Pay The Inheritance Tax?

If you’re a spouse or civil partner receiving an inheritance from your deceased spouse or civil partner, you don’t have to pay or worry about inheritance tax.

Everybody else is liable for inheritance tax. Your children are especially at high risks.

Anytime you want to create a strong secure financial plan for your future, you can get in touch with reputed financial advisors at MMA and discuss different types of financial and pensions advice Dublin.

How Is Inheritance Tax Paid In Ireland?

The onus to pay inheritance tax is always on the person who is receiving the gift or inheritance.

You must also know that: Revenue always expects tax liabilities to be settled quickly.

| Received Gifts or Inheritance: | Revenue expects payment by: |

| Between January – August | October 31st |

| Between September – December | August 31st of the following year. |

What Happens If You’re Late Filing A Payment?

As you can see from the above table, the payment for inheritance tax depends on when the inheritance was received in regard to what date payment must be made.

However, if you’re not a resident of Ireland, then it is your responsibility to arrange for an agent in Ireland to ensure that your Capita Acquisition Tax (CAT) is made to Revenue.

If you’re late filing your revenue but pays the tax by 31st October, you’ll face a late filing charge:

When the delay is 2 months or less – 5%

Any delay longer than 2 months – 10%

In tandem with the above charges, there will also be an interest charge per day. This will equate to approximately 8% per annum.

What Should A Parent Do To Prepare For Inheritance Tax?

If the parents are married or civil partners, then they receive inheritance from their spouse, tax-free.

The problem arises with the death of the second parent.

- Death of the first parent – assets passed down to the second partner – which is tax-free.

- Death of the second parent – assets pass the children – which is fully taxable.

How Is Inheritance Tax Calculated?

The first thing you need to consider is the value of the estate. Then you have to decide the threshold that you fall under.

Currently, there are three different threshold groups:

| Group A | Group B | Group C | |

| €335,000 | €32,500 | €16,250 |

As already mentioned, the CAT for gifts and inheritance is 33%.

Group A | Son/Daughter

Group A applies to the son or daughter of the person endowing the gift or inheritance. It also includes foster children, step-children, and adopted children. Parents also fall under this threshold when they take an absolute inheritance from a child.

Group B |Brother/Sister/Niece

Group B applies when the beneficiary is a brother, sister, niece, nephew, grandparent, grandchild, lineal ancestor or a lineal descendant of the disponer.

Group C|Other

People with a relationship to the disponer and not covered in Group A or B fall under Group C.

What If I Have Received A Previous Inheritance?

If you’ve received an inheritance of €50,000 (for example) from one of your parents, then your threshold will reduce from €335,000 to €285,000.

If you pass your threshold completely with a different inheritance, anything that is received from the point will be taxed at 33%.

Inheritance Tax Reliefs

There are 4 reliefs that you can use to lower your inheritance tax liability:

Dwelling House Exemption

You will be exempted from CAT on the inheritance of a dwelling house if:

- The house must be the main residence of the person who has died.

- The person inheriting the home must have lived there for three months before the homeowner’s death.

- The person inheriting the house doesn’t own or have any interest in another house.

- The individual inheriting the home must remain living in the home for at least six years after inheritance.

- The individual inheriting the home must not possess any interest in any other property. This also includes any other properties that may be part of the same inheritance.

This will not apply, if:

- You‘re over 65 at the date of inheritance.

- You’re required by reason of employment to live elsewhere.

- You’re required to live elsewhere because of your mental or physical state as certified by the doctor.

Favourite Niece/Nephew

When this relief applies, a niece or nephew can be treated as a child and get the higher threshold of €335,000.

Annual Gift Exemption:

You may receive a gift up to €3,000 of value from any person in any calendar year without having to pay Capital Acquisition Tax (CAT). This means that you can take a gift from several people in the same calendar year and the first €3,000 from each disponer is exempt from CAT.

How Can You Use Life Insurance To Cover Inheritance Tax?

You can easily do so by using a special Revenue approved policy called Section 72. For more details on this, feel free to discuss it with our expert financial advisors.

What Is Section 72 Life Insurance Policy?

Previously known as a Section 60 policy, a Section 72 is a Revenue approved Life Insurance policy. The payout on an S72 is tax-free if you use it to pay inheritance tax liability.

In simple words, money flows through the policy tax-free to pay an inheritance tax bill.

How Should I Set Inheritance Tax Life Insurance?

For this, you need to rightly estimate the amount of inheritance tax you will need to cover. However, this is an inexact science because there are three variables that you have no control over:

- The market value of the assets.

- The tax-free thresholds.

- The 33% inheritance tax rate.

Final Thoughts

This is a pretty comprehensive look on how to look on how to use Section 72 Life Assurance to pay an inheritance tax bill. Get in touch with our team and receive genuine, fair information on inheritance tax in Ireland. Feel free to ask for pensions advice Dublin and our team will be more than happy to help!

Talk to us at +353 91 393 125

Mail us at office@mmadvisors.ie

Or visit our office at Unit 3, Office 6, Liosban Business Park, Tuam Rd, Galway, Ireland

Read Also- What Are Your Legal Rights When Facing Redundancy?