For Irish property investors, one of the biggest decisions is whether to buy a rental property in their own name or through an SPV (Special Purpose Vehicle). The choice impacts everything from tax and mortgage eligibility to long-term financial planning. In this detailed guide, Money Maximising Advisors explains the key differences between the two options and helps you decide which structure suits your investment goals.

What Is an SPV and How Is It Different from a Personal Buy-to-Let?

An SPV is a company set up specifically to own and manage property. In Ireland, many landlords form an Irish SPV property company to hold a single rental property or an entire portfolio. This structure separates your personal finances from the investment and provides a clearer business framework.

A traditional buy-to-let, on the other hand, means you purchase the property in your own name and apply for the mortgage personally. Rental income and expenses are declared through your personal tax return.

Key Differences Between a Buy-to-Let Mortgage and an SPV Mortgage

1. Liability and Protection

With an SPV, the property is held by the company—not you personally. This provides a layer of protection, as the SPV ring-fences liabilities. With personal buy-to-let, the investor holds full responsibility for the mortgage and any associated risks.

2. Mortgage Options and Rates

Not all lenders in Ireland offer SPV mortgages. Those that do may have stricter criteria and slightly higher rates. However, specialist lenders increasingly provide limited company BTL mortgage Ireland products designed specifically for SPVs. Comparing SPV mortgage rates Ireland is crucial before making a decision.

3. Taxation and Allowable Deductions

One of the biggest reasons Irish investors choose an SPV is taxation. An SPV pays corporation tax on rental profits and may offer better flexibility for reinvesting profits. Personal buy-to-let income is taxed at individual income tax rates, which can be much higher.

With proper planning, investors can unlock tax benefits SPV rentals Ireland, especially when building a long-term portfolio.

4. Administration and Compliance

A private landlord only needs to maintain basic records and file personal tax returns.

An SPV, however, must file annual accounts, maintain company records, and meet corporate compliance obligations. This adds cost and responsibility, but many investors find the professional structure worth it.

Why Many Irish Investors Choose an SPV

- Better long-term planning: Ideal for those building a property portfolio.

- Professional structure: Many lenders and partners prefer dealing with a company.

- Flexibility for business partners: Shares in the SPV can be distributed easily.

- Succession planning: Ownership transfers are simpler.

- Reinvestment benefits: Profits can be retained in the company at lower tax rates.

- Privacy: Tenants see the company as the landlord, not your personal name.

For investors looking to scale, an SPV for rental property Ireland is often the preferred route.

Potential Drawbacks of an SPV

- Higher mortgage rates than personal BTL mortgages in some cases

- More paperwork and compliance costs

- Possible double taxation when withdrawing profits as personal income

- Stricter lending criteria and lower lender availability

- May not be necessary for single-property owners

These factors should be weighed carefully before choosing your structure.

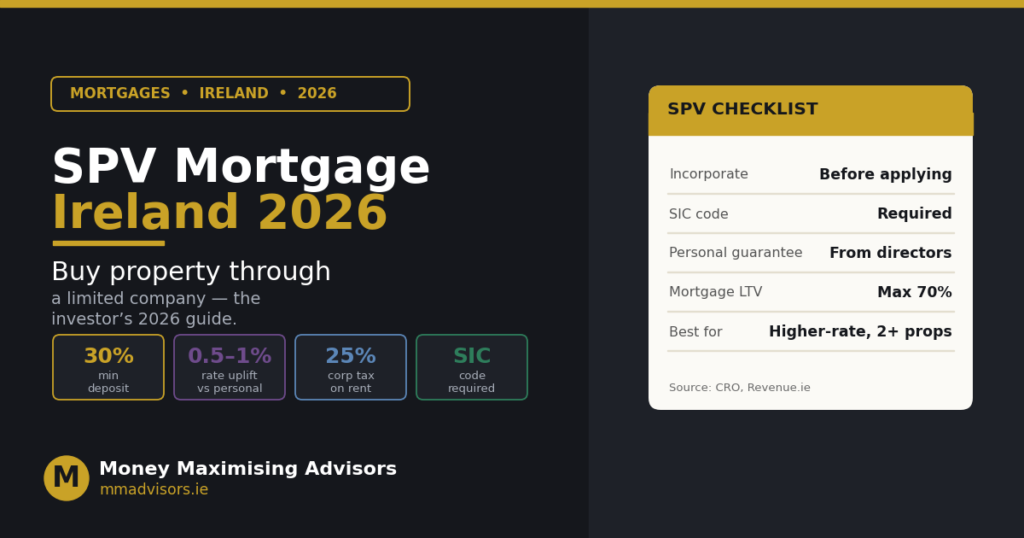

SPV Mortgage Eligibility in Ireland

Lenders offering Buy to let SPV Ireland products typically assess:

- Strength of the business plan

- Expected rental income

- Directors’ personal guarantees

- Loan-to-value ratios

- Property type and location

- Company structure

This is why understanding BTL SPV eligibility Ireland before applying can save time and improve approval chances.

Setting Up an SPV for Buy-to-Let in Ireland

If you decide to move forward, here is a step-by-step outline:

1. Create Your Company

Choose a clear and professional name, especially if it will be used as a company name buy to let mortgage for lender applications.

2. Register the SPV

Register the company with the Companies Registration Office (CRO). This forms your official Irish landlords SPV setup.

3. Open a Business Bank Account

Keep all property income and expenses separate from personal finances.

4. Apply for an SPV Mortgage

Work with a broker familiar with limited company BTL mortgage Ireland and SPV lending. This ensures access to specialist lenders.

5. Manage Accounting and Compliance

Your SPV must:

- File annual returns

- Maintain records

- Prepare financial statements

- Pay corporation tax

This is simple when done with proper planning or using a good accountant.

Tax Considerations for SPV Investors

Investors often choose SPVs for better tax planning. Key points include:

- Corporation tax on rental profits may be lower than personal income tax.

- SPVs can retain profits for reinvestment.

- Some expenses may be more straightforward to claim.

- Dividends or withdrawals must be planned to avoid unnecessary tax.

- Stamp duty and VAT rules still apply regardless of ownership structure.

While there are many tax benefits SPV rentals Ireland, professional advice is crucial to ensure compliance and optimal savings.

Who Should Consider an SPV?

An SPV is ideal if you:

- Plan to build a portfolio of two or more rental properties

- Want separation between your personal and investment finances

- Need a more professional structure for joint ventures

- Prefer long-term wealth building over short-term rental income

- Want better options for estate and succession planning

A personal buy-to-let is better suited to one-off investments or landlords who prioritise simplicity over structure.

Buy-to-Let vs SPV: Quick Comparison

| Feature | Personal Buy-to-Let | SPV Buy-to-Let |

|---|---|---|

| Taxation | Personal income tax | Corporation tax |

| Mortgage rates | Usually lower | Slightly higher |

| Lender availability | High | Moderate |

| Administration | Simple | More complex |

| Liability | Personal | Company-based |

| Best for | Small-scale landlords | Portfolio investors |

Final Thoughts: Which Option Is Better?

There is no one-size-fits-all answer.

If you’re buying one property for passive income, a personal buy-to-let may be perfectly suitable.

If you are serious about growing a portfolio, reinvesting profits or managing your properties as a business, an SPV is often the more strategic choice.

Money Maximising Advisors helps investors evaluate both scenarios, compare SPV mortgage rates Ireland, understand tax implications, and complete the Irish landlords SPV setup process smoothly.

Whether you’re planning to set up SPV buy to let Ireland or want guidance on choosing between structures, our team ensures you make a confident, informed and profitable decision.