If you live and work in Dublin, the State Pension is almost certainly part of your retirement plan, but how it actually works is one of the most consistently misunderstood pieces of the Irish financial system. Some Dubliners assume it will cover everything; others assume they will get nothing. Both groups end up making poor decisions because of it. At Money Maximising Advisors, we sit down with Dublin clients every week to set the record straight before they finalise a private pension strategy. This guide answers the most common questions, debunks six of the biggest myths, and shows you how the State Pension fits into a properly designed Dublin retirement plan.

| This article sits within our Pensions hub and supports the pages our Dublin clients visit most often, including Pensions Advice, Retirement Planning Advice, Additional Voluntary Contributions (AVCs), Directors Pension and Pensions For The Self Employed. |

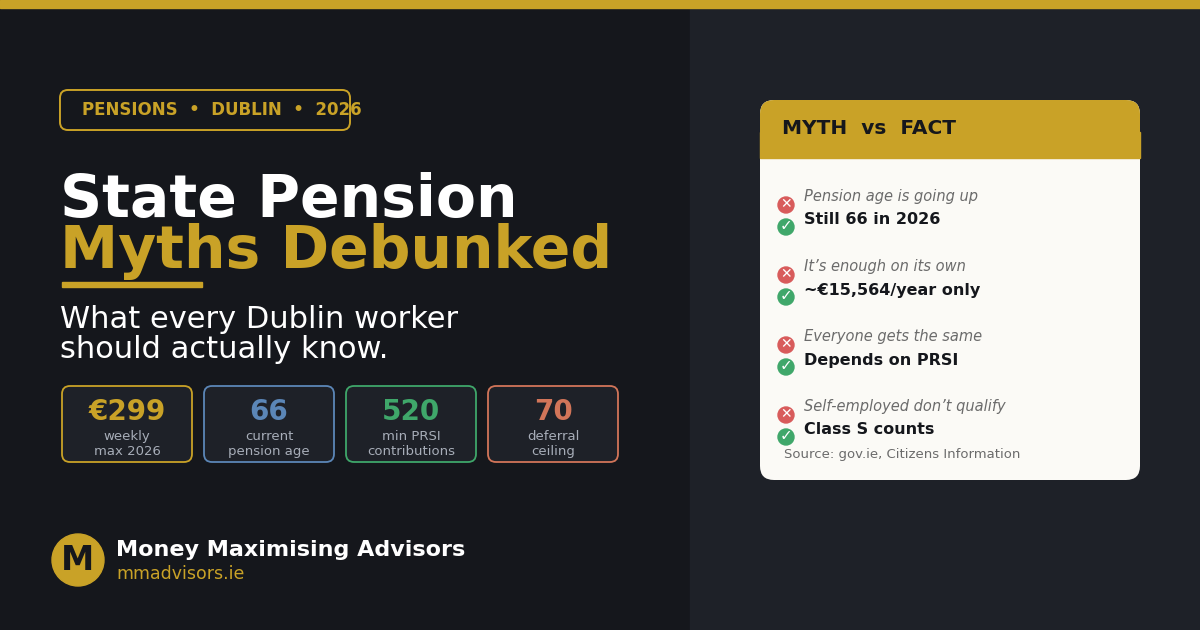

Four numbers that define the 2026 Irish State Pension landscape the starting point for any Dublin retirement plan.

Quick answers: the six questions most Dublin workers ask

What are the most common myths about the State Pension in Ireland?

Six recur in almost every Dublin pension conversation: that the State Pension is enough on its own, that everyone gets the same amount, that the pension age is rising again, that a private pension cancels out the State one, that part-time or career-break workers get nothing, and that the self-employed do not qualify. None of these is true, we walk through each one below.

Is the Irish State Pension enough for retirement?

In a word, no. The maximum personal rate of the State Pension (Contributory) from 1 January 2026 is €299.30 per week, which works out to roughly €15,564 per year. For most Dublin households that is well below the level needed to maintain their pre-retirement lifestyle, particularly with city-centre rents and suburban running costs being what they are. A private pension on top of the State Pension is essential for the vast majority of workers.

Can I receive a private pension and State Pension at the same time?

Yes , the State Pension (Contributory) is not means-tested. It is paid based on your PRSI record alone, regardless of any private pension, occupational pension, ARF drawdown, savings or other income you have. The two layer on top of each other. Only the State Pension (Non-Contributory) is means-tested, and it only applies if you do not qualify for the Contributory version.

How many PRSI contributions do I need for a full State Pension?

Under the Total Contributions Approach (TCA), you need 2,080 paid full-rate PRSI contributions the equivalent of 40 years, to qualify for the maximum rate. To qualify for any rate, you need at least 520 paid contributions (10 years) and to have entered insurable employment before age 56. Between those two bounds you receive a pro-rata amount.

What age can I claim the State Pension in Ireland?

The qualifying age in 2026 remains 66. Proposed increases to 67 and 68 were not enacted. For those born after 1 January 1958, you can also defer claiming up to age 70, each year of deferral increases your weekly rate when you eventually start drawing it. We can model whether deferral makes sense for your situation as part of a Retirement Planning Advice review.

Does everyone qualify for the State Pension in Ireland?

Not automatically. The Contributory pension is earned through PRSI; the means-tested Non-Contributory version acts as a safety net for residents aged 66+ who fall short. Most full-time Irish workers, employees and self-employed alike, will qualify for some level of Contributory pension, although the rate can vary significantly depending on your work history. People who took career breaks, worked abroad for long periods, or who only worked part-time should check their record early and explore options to fill any gaps.

The six biggest State Pension myths debunked

The six recurring misconceptions Dublin workers bring to a pension review and what the rules actually say.

Myth 1. “The State Pension is enough to retire on.”

This is the most expensive misconception in Irish personal finance. At €299.30 per week (€15,564 per year) in 2026, the State Pension delivers roughly a third of average Irish full-time earnings. For a Dublin couple where both qualify for the full rate, the combined household income is around €31,000 a year a meaningful foundation, but nowhere near enough to maintain most pre-retirement lifestyles, especially with city living costs. A Pension Plan in Ireland projection will show you the gap clearly.

Myth 2. “Everyone gets the same amount.”

The rate you receive is directly tied to your PRSI contribution record. Two Dubliners retiring on the same day with the same employer history will only receive the same pension if their lifetime PRSI history is identical. Career breaks, periods abroad, part-time work and self-employment gaps all reduce your rate, sometimes by a quarter or more. Checking your record at MyWelfare.ie should be one of the first things any Dublin worker over 45 does.

Myth 3. “The pension age is going up to 67 or 68.”

Proposed rises to age 67 (in 2021) and 68 (in 2028) were debated, but not enacted. As of 2026, the State Pension age remains 66. A flexible deferral option was introduced for those born after 1 January 1958: you can choose to start your pension any time between 66 and 70, with the weekly rate increasing for each year of deferral. The official age has not risen, only the upper end of when you can choose to claim.

Myth 4. “My private pension will cancel out the State Pension.”

This one comes up almost every week in Dublin client meetings. The Contributory State Pension is not means-tested and is paid in addition to any private pension you have. There is no offset, no reduction, no clawback against the rate. The whole point of building Additional Voluntary Contributions (AVCs), an Occupational Pension, a PRSA or a Directors Pension is that they layer on top of the State Pension, not in place of it.

Myth 5. “If I never worked full-time, I get nothing.”

Several mechanisms protect people whose PRSI record looks thin on paper:

- PRSI credits are awarded for periods on social welfare payments such as Jobseeker’s Benefit, Illness Benefit, Maternity Benefit and Carer’s Benefit.

- Long-Term Carers Contributions (introduced from 1 January 2024) can credit up to 1,040 weeks 20 years toward your record if you cared for someone full-time.

- UK and EU contributions may count under bilateral social security agreements, often closing the gap for people who worked abroad earlier in life.

- The Non-Contributory pension is means-tested but provides a safety net at age 66+ for those who still do not qualify for the Contributory version.

Myth 6. “Self-employed people don’t qualify for the State Pension.”

Self-employed Irish workers pay Class S PRSI at 4.2% of reckonable income, with a minimum annual charge of €650 in 2026 and those contributions count fully toward the State Pension. A Dublin freelancer, contractor or sole trader who has been paying Class S consistently for 40 years can absolutely qualify for the full rate. The strategy for self-employed workers also typically includes a PRSA or Personal Pension, which carries generous tax relief and sits on top of the State Pension at retirement.

How your PRSI record translates into a weekly rate

Indicative TCA bands, your actual rate is the higher of the TCA and Yearly Average assessments.

Two methods are used to calculate your State Pension rate. The Yearly Average divides your total contributions by the years between your first PRSI payment and pension age, an average of 48 or more gives the full rate. The Total Contributions Approach (TCA) simply counts your total paid weeks: 2,080 (40 years’ worth) gets you the full rate, with proportional reductions below that. Revenue and the Department of Social Protection assess you under both and pay whichever produces the higher rate.

For most Dublin workers, the practical implication is straightforward: every paid PRSI week is worth real money in retirement. Checking your record before you reach 60 gives you time to plug gaps, which is exactly the kind of housekeeping our Pensions Advice team handles routinely.

How the State Pension fits into a Dublin retirement plan

The right way to think about the State Pension is as the foundation of your retirement income, not the structure itself. For a Dublin household targeting a comfortable retirement enough to keep paying the running costs of a Dublin home, contribute toward grandchildren’s education, take regular holidays and absorb the occasional larger expense, the State Pension typically covers 30–50% of what you actually need. The rest comes from a private pension built up over your working life.

The mix depends heavily on your employment status. PAYE employees usually rely on a workplace pension plus AVCs; public sector workers in Dublin should look at Public Sector AVCs and Last Minute AVC close to retirement; company directors get extraordinary leverage from a Directors Pension; and self-employed Dubliners typically use a PRSA. All of these layer on top of the State Pension.

| Want to see exactly how much State Pension you’re on track for? Book Now for a free Dublin pension review, or Enquire Now and we will be in touch within one working day. |

Boosting your PRSI record before you retire

If you spot a gap in your record a few years working abroad, a career break, an early period in casual work, several routes can help close it before retirement:

- Voluntary contributions can be made if you have at least 520 paid PRSI contributions and apply within 60 months of leaving compulsory PRSI; rates depend on your last class of contribution.

- Working past 66 with deferral under the post-2024 rules allows you to keep building contributions to age 70 while earning a higher eventual pension rate.

- Long-Term Carers Contributions can be claimed retrospectively if you provided full-time care for 20 years or more.

- UK/EU contributions are aggregated under bilateral agreements — your years working in London, Manchester or anywhere across the EU can count toward the qualifying conditions.

- Class S self-employment can be added later in your career and still contributes meaningfully to a full record.

Common State Pension mistakes Dublin workers make

From the conversations we have every week in Dublin client meetings:

- Assuming the State Pension will be enough. Project the gap between your expected retirement spending and €15,564/year early, the answer drives every other decision.

- Not checking the PRSI record until age 64. By then it is often too late to plug meaningful gaps. Run the check at 45, again at 55.

- Ignoring overseas contributions. Years worked in the UK, Australia or other agreement countries often go uncounted simply because nobody asked Revenue to add them.

- Stopping work at 66 without modelling deferral. For people in good health with another income, deferring can be one of the highest-return decisions available.

- Treating the private pension as optional. It is the only realistic route to bridge the income gap for most Dublin workers.

Most-read pension guides for Dublin workers

If you found this useful, these are among our most-visited pension guides:

- Pension Plan in Ireland: How Much Will My Pension Pay Me If I Retire at 60?

- AVC vs PRSA: Which Irish Pension Top-Up is Right for You?

- Auto-Enrolment Pensions Ireland: Everything You Need to Know in 2026

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- How Pension Advice in Ireland Saves Tax & Grows Wealth

- Pension Tax-Free Lump Sum at 50 Ireland — All You Need To Know

Explore our full range

This guide is part of our wider Pensions hub. You can also explore our Mortgages, Protection, Public Sector, Savings & Investments and Inheritance Tax hubs, or learn more about us.

Our Services & Products

Our Services

Our Products

Related posts

- Cork State Pension Not Enough: Your Retirement Options 2026 Guide

- Auto-Enrolment Pensions Ireland: Everything You Need to Know in 2026

- Standard Fund Threshold 2026: What It Means for Your Pension in Ireland

- Early Retirement in Ireland: Your 2026 FIRE Strategy Guide

Dublin? Let’s look at your pension together.

Whether you are 35 and starting from scratch, 50 and trying to make up lost ground, or 60 and within touching distance of retirement, our team will give you a clear, no-jargon picture of what the State Pension will deliver, what the gap looks like, and exactly which private vehicles will close it. Book Now for your free Dublin pension review, or visit Money Maximising Advisors to learn more about how we work.

Important information

State Pension rates, PRSI rules and pension age provisions referenced in this article are correct as at 1 January 2026 and are drawn from gov.ie, Citizens Information and the Budget 2026 announcement. Rates and rules can change in future Budgets. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. The value of private pension investments can fall as well as rise, and past performance is not a reliable indicator of future returns. You should seek personalised advice from a Qualified Financial Advisor before making any financial decision.