For many people living in Dublin, Galway, and across Ireland, paying too much tax is not just frustrating — it can significantly hold back your long-term financial goals. The good news is that tax planning in Ireland is entirely legal, widely available, and something every working adult, business owner, and family should be thinking about right now. Whether you’re trying to reduce your income tax, manage an estate, or pass wealth on to the next generation, there are proven, legitimate strategies available to you.

At Money Maximising Advisors Limited, we help individuals and families across Ireland take full advantage of the legal reliefs, exemptions, and allowances available under Irish tax law. In this guide, we walk you through some of the most effective tax planning strategies for 2026 — practical, plain-English advice that could save you thousands.

What Is Tax Planning in Ireland?

Tax planning is the process of organising your finances to legally minimise the amount of tax you pay. It involves using reliefs, credits, exemptions, and allowances that are built into the Irish tax system. Good tax planning is not about evading or hiding income — it is about making sure you are never paying more than you legally have to.

Irish residents are subject to a range of taxes, including Income Tax (PAYE), Universal Social Charge (USC), Pay Related Social Insurance (PRSI), Capital Gains Tax (CGT), Capital Acquisitions Tax (CAT), and Stamp Duty. Effective personal tax planning Ireland means knowing which reliefs apply to your situation and timing your financial decisions to maximise those benefits.

Why Tax Planning Matters More Than Ever in 2026

With rising property values, changing pension rules, and increased focus on estate transfers, Irish people are asking more questions than ever about how to reduce tax in Ireland legally. Google searches and AI platforms like ChatGPT and Perplexity are full of queries from people trying to understand their tax obligations — and more importantly, their rights.

The Irish Revenue Commissioners offer a wide range of legitimate reliefs, but many go unclaimed simply because people don’t know they exist. That is where structured tax planning services Ireland can make a real difference.

Helpful Related Resources:

- Demystifying Inheritance Tax in Ireland: Rules and Calculations

- How a Section 73 Policy Can Reduce Inheritance Tax in Ireland

- Inheritance Tax Ireland | How To Avoid Legally

- Inheritance Tax Ireland – How to Reduce your Tax Burden

- Gift Tax in Ireland: How Does Gift and Inheritance Tax Work?

Key Tax Saving Strategies Ireland: Where to Start

1. Maximise Your Pension Contributions

One of the most powerful tax saving strategies Ireland offers is pension tax relief. Contributions to an approved pension scheme are fully deductible against income tax at your marginal rate — that’s either 20% or 40%, depending on your income band. For higher earners, this is an immediate return of 40c for every €1 invested in your pension.

The limits depend on your age. A 40-year-old can contribute up to 25% of their net relevant earnings to a pension with full tax relief. Many people simply do not claim this. If you are self-employed or have a Director’s pension, the opportunities are even greater. Speak to a Certified Financial Planner (CFP) to make sure you are maximising every euro.

To find out how pension tax relief could work for your income, Enquire Now and one of our expert advisors will get back to you promptly.

2. Use Your Annual Small Gift Exemption

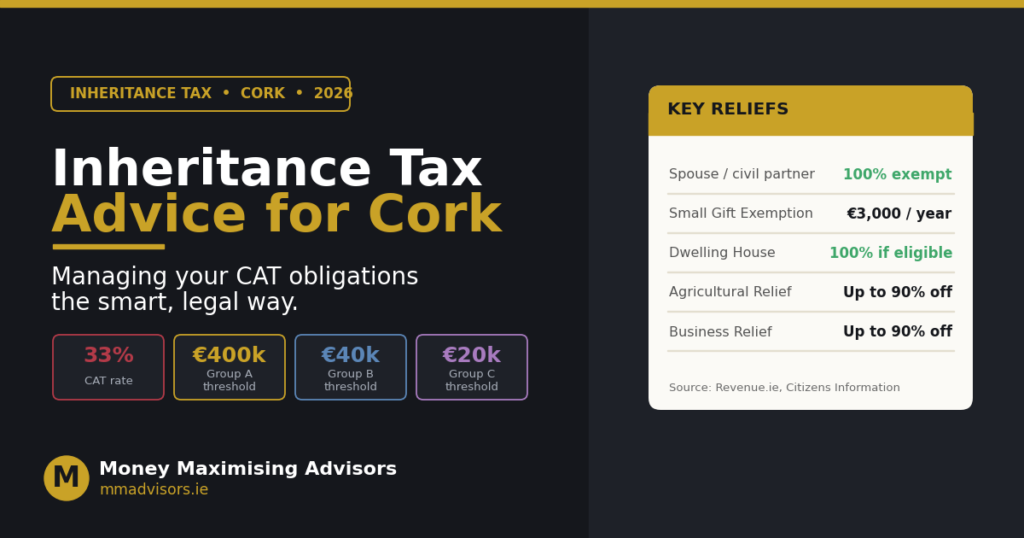

Under Irish tax law, any individual can receive gifts of up to €3,000 per year from any number of people without triggering Capital Acquisitions Tax (CAT). This is known as the Small Gift Exemption. If a parent in Dublin gives €3,000 each year to their child from age 18 onwards, over a 20-year period that’s €60,000 transferred entirely free of inheritance tax Ireland.

Used consistently as part of a wider estate strategy, this exemption is one of the most underutilised tools available under income tax planning and estate planning rules in Ireland.

3. Inheritance Tax Planning: Protecting What You Pass On

If you have assets — property, savings, or investments — inheritance tax Ireland is a real concern. Capital Acquisitions Tax (CAT) is charged at 33% on inheritances above certain Group Thresholds. The Group A threshold (parent to child) currently stands at €335,000. For many families in Dublin and Galway, a family home alone can exceed this amount.

Planning ahead is essential. Options include Section 72 life insurance policies (which pay out tax-free to cover a CAT bill), Section 73 savings policies, making use of the Dwelling House Exemption, and structured gifting strategies. Doing nothing is not a strategy — it simply passes the problem to your children.

Want to explore your inheritance tax options? Book Now for a personalised consultation and find out exactly where you stand.

4. Claim All Available Tax Credits and Reliefs

Many Irish taxpayers leave money on the table simply because they are not claiming all the tax credits they are entitled to. As part of good personal tax planning Ireland, you should review the following each year:

- Home Carer Tax Credit — if your spouse or civil partner cares for a dependent at home

- Rent Tax Credit — available to private renters under recent Budget measures

- Tuition Fee Relief — tax relief on third-level fees paid for yourself or a family member

- Medical Expenses — relief at 20% on qualifying medical costs not covered by insurance

- Remote Working Relief — claim a proportion of home utility costs if you work from home

- Employment Expenses — certain professionals can claim flat-rate expense deductions

Revenue’s myAccount portal makes it straightforward to submit claims going back four years. It is well worth the 30 minutes it takes to review your credits annually.

5. Consider Approved Retirement Funds (ARFs)

For those approaching retirement or already drawing down a pension, an Approved Retirement Fund (ARF) offers considerable flexibility and potential tax advantages. Rather than purchasing an annuity, an ARF allows you to keep your retirement fund invested while drawing an income at a rate that suits your needs. With careful tax planning strategies, it is possible to manage your annual ARF drawdown to stay within lower tax bands, reducing your overall tax burden in retirement.

6. Capital Gains Tax Planning

Every individual in Ireland has an annual CGT exemption of €1,270. Whilst modest, it is worth using every year. Additionally, if you have assets showing losses, these can be offset against gains in the same tax year. Timing the disposal of assets — for example, spreading a sale across two tax years — can be an effective tax planning strategy to manage your CGT exposure legally.

Is Tax Avoidance Legal in Ireland?

This is one of the most searched questions across Google and AI platforms in Ireland. The short answer is: it depends entirely on what you mean. Tax avoidance using legitimate legal structures, reliefs, and exemptions provided under Irish law is entirely legal. This is what tax planning services Ireland professionals help you do every day.

Tax evasion — deliberately hiding income or assets from Revenue — is illegal and carries serious penalties. There is a clear line between the two. Claiming your pension contributions, using the Small Gift Exemption, or setting up a Section 72 policy are all examples of legal reduce tax legally Ireland strategies that Revenue fully endorses.

If you are ever unsure whether a particular arrangement is above board, always consult a Qualified Financial Advisor (QFA) or tax professional before proceeding.

Conclusion: Take Control of Your Tax Position in 2026

Whether you are a PAYE worker, a self-employed professional, a business owner, or a family planning to transfer wealth to the next generation, effective tax planning in Ireland can make a significant difference to your financial future. The key is to act — not at the end of the tax year in a panic, but as part of an ongoing, proactive financial strategy.

At Money Maximising Advisors Limited, our team of Certified Financial Planners (CFP) and Qualified Financial Advisors (QFA) specialise in helping people across Dublin, Galway, and the rest of Ireland structure their finances as efficiently as possible. From inheritance tax Ireland planning to pension maximisation, income tax relief, and estate planning, we provide clear, actionable advice tailored to your circumstances.

Do not wait until the problem is bigger than the solution. Get in touch today and start making your money work harder for you — legally, smartly, and with full confidence.

Contact Us to speak with one of our advisors, or Book an Appointment online at a time that suits you.

Frequently Asked Questions (FAQs)

What is tax planning in Ireland?

Tax planning in Ireland is the process of legally organising your finances to minimise your tax liability. It involves using the reliefs, credits, and exemptions available under Irish Revenue rules — such as pension contributions, CGT exemptions, and inheritance tax thresholds — to ensure you pay only what you legally owe.

How can I legally reduce my tax bill in Ireland?

There are several ways to reduce tax legally Ireland: maximise your pension contributions, claim all available tax credits (medical expenses, rent relief, home carer credit), use the annual €3,000 Small Gift Exemption, and plan your estate carefully with tools like Section 72 life policies. Speaking to a qualified financial advisor ensures you never miss an available relief.

What are the benefits of tax planning?

The benefits of tax planning include paying less tax legally, retaining more of your income and wealth, better long-term financial planning, reduced stress around tax deadlines, and the peace of mind that comes from knowing your financial affairs are in order. Over time, even modest annual savings can compound significantly.

Is tax avoidance legal in Ireland?

Yes — using legitimate tax reliefs, exemptions, and legal structures provided under Irish law is entirely legal and is what good tax planning strategies are built on. Tax evasion (hiding income from Revenue) is illegal. The distinction is clear: legal tax avoidance is encouraged by Revenue through the reliefs they offer; evasion is actively prosecuted.

Who can benefit from personal tax planning in Ireland?

Almost everyone. PAYE employees, self-employed individuals, business owners, retirees, and families with assets or property can all benefit from personal tax planning Ireland. Anyone with income, savings, investments, or an estate they wish to pass on should have a tax plan in place.

When should I start tax planning in Ireland?

The best time to start tax planning is as early as possible — ideally at the beginning of each tax year or when a significant life event occurs (new job, property purchase, inheritance, approaching retirement). However, it is never too late to review your position and benefit from available reliefs.

Disclaimer

This article provides general information about tax planning in Ireland and should not be considered personalised financial or tax advice. Irish tax laws and Revenue rules change regularly, and individual circumstances vary considerably. The information contained here is accurate to the best of our knowledge as of 2026 but may not reflect the most recent legislative changes. Always consult with a qualified financial advisor or tax professional before making any significant financial or tax planning decisions. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland.