Losing a loved one is never easy. But for many Irish families, the grief of bereavement is quickly followed by an unexpected financial shock — a substantial inheritance tax Ireland bill that nobody planned for. Whether you are receiving a family home in Dublin, a sum of money from a relative in Galway, or assets from a parent anywhere in Ireland, understanding how inheritance tax Ireland works — and how it is calculated — is absolutely essential.

At Money Maximising Advisors, we specialise in helping Irish families navigate the complexities of inheritance tax Ireland, from understanding your obligations to legally reducing the amount you owe. In this guide, we break down everything you need to know about the inheritance tax calculation Ireland process — in plain, straightforward language.

What Is Inheritance Tax in Ireland?

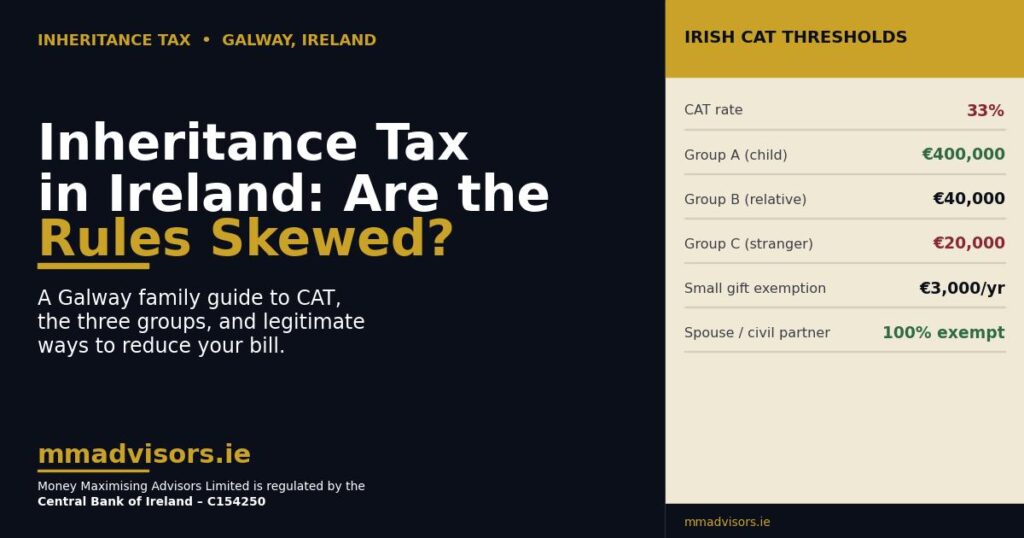

Inheritance tax in Ireland is officially known as Capital Acquisitions Tax (CAT). It is governed by the Capital Acquisitions Tax Consolidation Act 2003 and is administered by Revenue. CAT applies to gifts and inheritances received above a certain tax-free threshold, depending on your relationship to the person giving the assets (known as the “disponer”).

It is important to understand that CAT tax Ireland applies not just to cash inheritances but also to:

- Property (residential and commercial)

- Shares and investment portfolios

- Business assets

- Gifts received during someone’s lifetime

- Certain trust distributions

The same tax — CAT — applies to both gifts and inheritances, which means passing money or assets to someone while you are still alive does not automatically avoid the tax.

How Is Inheritance Tax Calculated in Ireland?

The inheritance tax calculation Ireland follows a clear process. Understanding each step will help you assess your own situation — or that of your estate — more accurately.

Step 1 — Identify the Group Threshold

The starting point for any CAT tax Ireland calculation is identifying which group threshold applies. This is determined entirely by the relationship between the person receiving the inheritance (the “beneficiary”) and the person leaving it (the “disponer”). There are three group thresholds:

| Group | Relationship to Disponer | Tax-Free Threshold (2026) |

| Group A | Child (including adopted/step-child) from parent | €335,000 |

| Group B | Siblings, nieces, nephews, grandchildren, parents | €32,500 |

| Group C | All other relationships (incl. friends, partners) | €16,250 |

These thresholds are lifetime limits. All gifts and inheritances received from the same group are added together across your entire lifetime. Once you exceed your threshold, the excess is taxable.

Step 2 — Calculate the Taxable Value

Once you know your group threshold, you subtract it from the total value of the inheritance. For example:

- A child inherits €500,000 from a parent.

- Group A threshold: €335,000.

- Taxable amount: €500,000 − €335,000 = €165,000.

Step 3 — Apply the CAT Rate

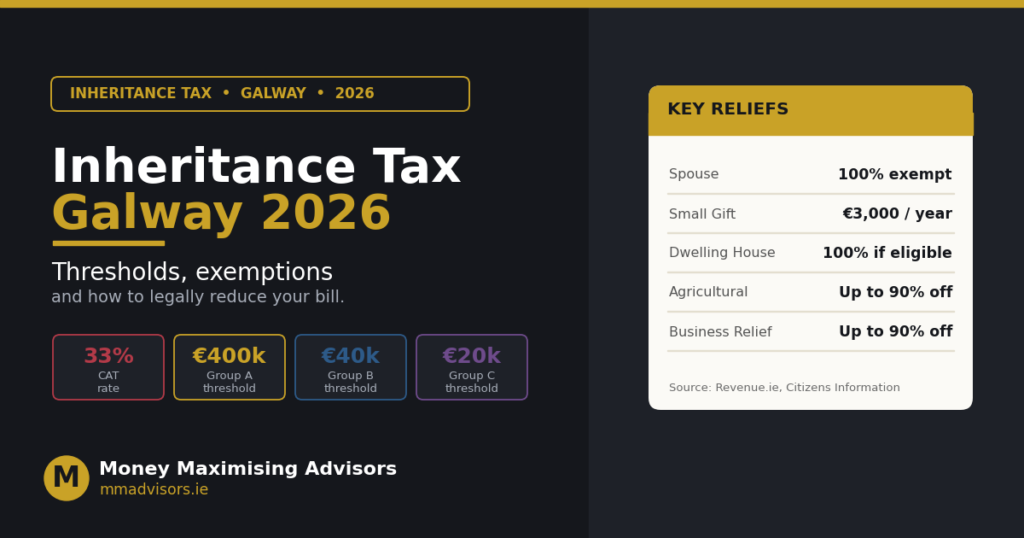

The inheritance tax rate Ireland is currently 33%. This is applied to the taxable amount above the threshold.

Using the example above: €165,000 × 33% = €54,450 CAT bill.

That is a significant sum — particularly if the inheritance is primarily property and the beneficiary does not have cash readily available to pay the bill. This is where proper planning with a qualified advisor can make an enormous difference.

Want to understand exactly how how is inheritance tax calculated Ireland in your specific situation? Enquire Now and one of our experienced tax advisors will walk you through the numbers.

The Small Gift Exemption — Reducing Your CAT Bill Year by Year

One of the most straightforward and legitimate ways to reduce a future inheritance tax Ireland bill is to make use of the Small Gift Exemption. Under current Irish tax rules, any individual can receive up to €3,000 per year from any single donor, completely free of CAT.

This means:

- Two parents can give a child up to €6,000 per year (€3,000 each) — completely tax-free.

- Grandparents can use the same exemption to build education funds for grandchildren.

- Over 10 years, parents could pass €60,000 to a child without touching the Group A threshold at all.

Godparents, uncles, aunts, and other relatives can also use the Small Gift Exemption to set up savings plans for children — building a fund over time for college fees or other future expenses. This strategy is particularly popular amongst Irish families looking to make smart, tax-efficient use of surplus income.

Section 72 and Section 73 Policies — The Irish Solution to Inheritance Tax

Section 72 Policies

A Section 72 policy is a whole-of-life insurance policy specifically designed to cover an anticipated capital acquisitions tax Ireland bill. The policy is taken out during your lifetime, and the payout on death is used to settle the CAT liability — meaning your beneficiaries do not have to sell the family home or liquidate assets to pay the tax.

Key benefits of a Section 72 policy:

- The payout is exempt from CAT in the hands of the beneficiaries (when used to pay a CAT liability)

- Premiums can be paid by the person leaving the estate or by the beneficiaries themselves

- Provides peace of mind that a large property or business can be passed on intact

Section 73 Policy Savings Plan

A Section 73 Policy Savings Plan is a strategic savings plan designed for individuals who want to pass assets — such as property or cash — to loved ones in the most tax-efficient way possible. Funds accumulated within a Section 73 plan can be used to pay a CAT bill when the time comes, and when used for this purpose, the plan proceeds are exempt from CAT.

This is a particularly smart solution for grandparents, godparents, or relatives who want to build a ring-fenced fund for younger generations without immediately triggering a tax liability.

Not sure whether a Section 72 or Section 73 plan is right for your family’s situation? Book Now for a no-obligation consultation with one of our Certified Financial Planners.

Related Posts

Demystifying Inheritance Tax in Ireland: Rules and Calculations

How a Section 73 Policy Can Reduce Inheritance Tax in Ireland

Inheritance Tax Ireland | How To Avoid Legally

Inheritance Tax Ireland – How to Reduce your Tax Burden

Gift Tax in Ireland: How Does Gift and Inheritance Tax Work?

Key Exemptions and Reliefs That Can Reduce Your Inheritance Tax Calculation Ireland

Beyond the thresholds and the Small Gift Exemption, there are several important reliefs that can significantly reduce — or even eliminate — a CAT liability. These include:

- Dwelling House Exemption: A beneficiary who has lived in the property for at least three years before the inheritance, and who has no other residential property, may be fully exempt from CAT on that home.

- Agricultural Relief: Qualifying farmers can receive agricultural land and assets at a 90% reduction in their taxable value, massively reducing the CAT bill.

- Business Relief: Similar to Agricultural Relief, Business Relief provides a 90% reduction in the taxable value of qualifying business assets.

- Favourite Nephew/Niece Relief: A niece or nephew who has worked substantially in a family business may qualify for Group A threshold treatment rather than the lower Group B threshold.

- Charitable Exemption: Inheritances left to approved charities in Ireland are fully exempt from CAT.

Understanding which reliefs apply to your situation can make a dramatic difference to your final inheritance tax calculation Ireland. This is precisely where working with an experienced advisor pays for itself.

Who Pays Inheritance Tax in Ireland?

Under Irish law, it is the beneficiary — the person receiving the inheritance — who is responsible for paying the CAT tax Ireland. This can come as a surprise to many families, particularly when the inheritance is primarily property rather than liquid cash.

The deadline for filing a CAT return and paying the tax due is 31 October of the year following the valuation date. Missing this deadline can result in interest charges and penalties from Revenue.

If a beneficiary cannot pay the CAT bill — because, for example, the inheritance is a family farm or home — they may be forced to sell assets to raise the funds. This is precisely the scenario that a well-structured Section 72 policy is designed to prevent.

Frequently Asked Questions (FAQs)

1. How is inheritance tax calculated in Ireland?

Inheritance tax in Ireland — formally called Capital Acquisitions Tax (CAT) — is calculated by first identifying your group threshold based on your relationship to the person leaving the estate. The threshold is subtracted from the total value received, and CAT at 33% is applied to the remainder. All gifts and inheritances from the same group are aggregated over your lifetime.

2. What is the inheritance tax rate in Ireland?

The standard inheritance tax rate Ireland is 33%, applied to any amount above your applicable group threshold. This rate applies to both gifts received during a person’s lifetime and inheritances received on death. Certain reliefs such as Agricultural Relief and Business Relief can significantly reduce the taxable value before this rate is applied.

3. How much can you inherit tax-free in Ireland?

How much you can inherit tax-free depends on your relationship to the deceased. Children inheriting from a parent have a lifetime tax-free threshold of €335,000 (Group A). Siblings, nieces, nephews, and grandchildren have a Group B threshold of €32,500. All others — including friends and non-married partners — have a Group C threshold of €16,250. The Small Gift Exemption of €3,000 per year per donor sits outside these thresholds entirely.

4. Who pays inheritance tax in Ireland?

In Ireland, the beneficiary — the person receiving the inheritance — is responsible for paying CAT. This is different to some other countries where the estate pays the tax before assets are distributed. The filing and payment deadline is 31 October of the year following the valuation date, and penalties apply for late payment.

5. What is a Section 72 policy and how does it help with inheritance tax Ireland?

A Section 72 policy is a whole-of-life insurance policy specifically designed to cover a CAT liability. The payout on death is used to settle the inheritance tax bill, and when used for this purpose, the proceeds are exempt from CAT in the beneficiaries’ hands. It is one of the most effective tools for ensuring that a family home or business can be passed on without being sold to pay a tax bill.

6. Can I reduce my inheritance tax bill legally in Ireland?

Yes — there are several legitimate strategies available. These include making full use of the €3,000 annual Small Gift Exemption, taking out a Section 72 or Section 73 policy, timing the transfer of assets to avail of available reliefs, and structuring your estate to maximise the use of thresholds across multiple beneficiaries. A qualified inheritance tax advisor can help you identify the right combination for your circumstances.

Conclusion

Understanding inheritance tax Ireland does not have to be complicated — but getting the planning wrong can be extremely costly for your loved ones. Whether you are looking to understand your own exposure, protect a family home, or build a long-term strategy to minimise the tax burden on the next generation, the most important step is taking professional advice sooner rather than later.

At Money Maximising Advisors, our team of experienced Tax Advisors, Certified Financial Planners (CFP), and Qualified Financial Advisors (QFA) work with families across Dublin, Galway, and the rest of Ireland every day. We make the inheritance tax calculation Ireland process straightforward, and we help you build a plan that protects your estate and your family’s future.

Do not leave it until it is too late. Contact Us today to speak with a specialist, or Book an Appointment at a time that suits you. Your family deserves a plan.

Disclaimer

This article provides general information about inheritance tax and Capital Acquisitions Tax (CAT) in Ireland and should not be considered personalised financial or tax advice. Irish tax laws, thresholds, and reliefs are subject to change. Individual circumstances vary considerably and the details of your own situation may affect how the rules apply to you. Always consult with a qualified financial advisor or tax professional — such as the team at Money Maximising Advisors — before making significant decisions regarding estate planning or inheritance tax.