Buying a home is one of the biggest financial commitments you will ever make, and protecting that investment should be a top priority. That is where mortgage protection Ireland comes in – a type of life insurance specifically designed to pay off your outstanding mortgage if you or your partner pass away during the term of the loan.

At Money Maximising Advisors Limited, we understand that navigating mortgage protection insurance can feel complicated. Our experienced team of Certified Financial Planners (CFP) and Qualified Financial Advisors (QFA) are here to make it simple and help homeowners across Dublin, Galway, and all of Ireland get the cover they need.

In this guide, we will cover everything you need to know about mortgage protection insurance Ireland, from whether it is compulsory to how much it costs and what to watch out for.

What Is Mortgage Protection Insurance?

Mortgage protection insurance Ireland is a type of decreasing term life insurance for mortgage protection that is taken out for the same duration as your mortgage. The cover amount decreases over time in line with your outstanding mortgage balance, so if you pass away during the term, the policy pays off the remaining mortgage.

This means your family can stay in the home without the burden of mortgage repayments. It provides real peace of mind during what can be one of life’s most stressful financial commitments.

Is Mortgage Protection Compulsory in Ireland?

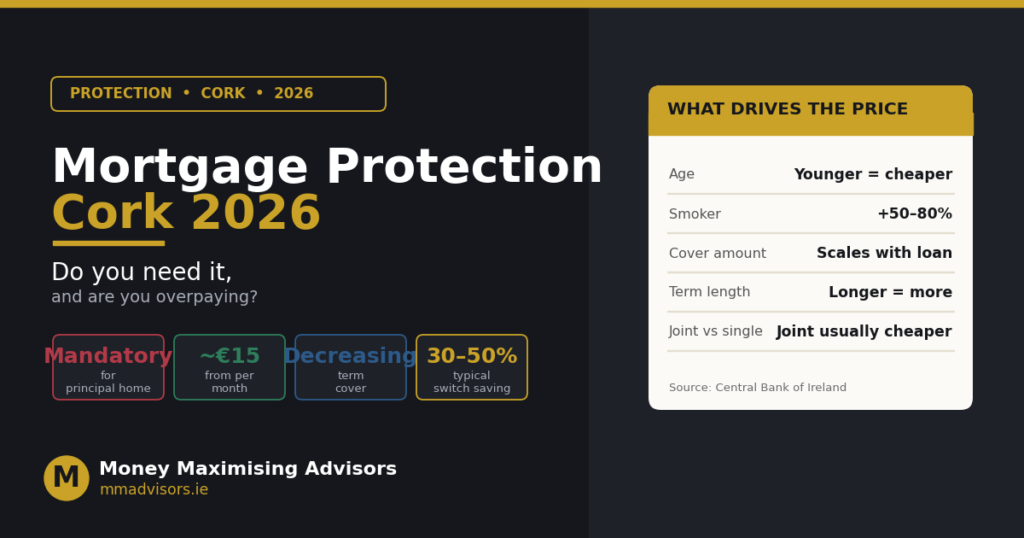

In short, yes – for most borrowers. Under the Consumer Credit Act 1995, mortgage protection Ireland is a legal requirement when taking out a home loan in Ireland. Your lender must ensure that you have a mortgage protection cover Ireland policy in place before they will release the mortgage funds.

There are a few exceptions to this rule:

- If you are over a certain age (typically 50 or above) and cannot obtain cover.

- If you have a serious health condition that makes you uninsurable.

- Investment or buy-to-let properties are generally exempt.

For a deeper dive into the legal requirements, read our detailed article on Mortgage Protection Insurance Ireland: Legal Requirements Explained.

How Much Does Mortgage Protection Cost in Ireland?

The mortgage protection insurance cost varies depending on several factors:

- Your age – Younger applicants typically pay lower premiums.

- Your health – Pre-existing conditions or being a smoker can increase costs.

- The mortgage amount – Larger mortgages require more cover, which costs more.

- The mortgage term – Longer terms mean the insurer is covering you for a greater period.

As a rough guide, a healthy non-smoker in their early 30s with a €300,000 mortgage over 30 years might pay anywhere from €20 to €40 per month. However, prices can vary significantly between providers, which is why it pays to shop around or, better yet, work with a qualified advisor who can compare the market for you.

Want to find the best deal on mortgage insurance? Book an Appointment with our team and we will compare the top providers for you.

What Are Red Flags on a Mortgage Application?

While this guide focuses on mortgage protection Ireland, it is worth mentioning some common issues that can cause problems with your mortgage Ireland application more broadly:

- Unpaid debts or loans – Outstanding personal loans, credit card balances, or missed payments are major red flags.

- Irregular spending – Lenders scrutinise your bank statements closely. Gambling transactions, frequent overdraft use, or unexplained large withdrawals can raise concerns.

- Insufficient savings history – Banks want to see a consistent pattern of saving over at least 6 months.

- Job instability – Frequent job changes or short employment history can be a concern.

Addressing these issues before you apply can significantly improve your chances of approval.

Will Mortgage Rates Go Down in 2026 in Ireland?

This is a question on many homebuyers’ minds. While nobody can predict the future with certainty, the European Central Bank’s monetary policy decisions have a direct impact on mortgage protection insurance Ireland costs and broader mortgage Ireland rates. If interest rates continue to stabilise or decrease, it could mean more favourable borrowing conditions for Irish homebuyers.

Regardless of rate movements, having proper mortgage protection cover Ireland in place is essential to protect your family and your home. And remember, understanding your wider financial picture – including tax implications of gifts towards your deposit – is just as important. Check out our post on How Much Money Can You Gift to a Family Member Tax-Free in Ireland? for more on this topic.

Ready to protect your home and your family? Enquire Now for expert advice on mortgage protection insurance, or Book Now to schedule your consultation.

Have questions about your mortgage protection options? Contact Us – we are always happy to help.

Conclusion

Mortgage protection Ireland is not just a legal requirement – it is a vital safety net for you and your family. Understanding the costs, knowing what is required, and choosing the right policy can save you money and give you peace of mind throughout the life of your mortgage.

At Money Maximising Advisors Limited, we make it our business to find you the best mortgage protection insurance Ireland policy at the most competitive price. Serving clients across Dublin, Galway, and throughout Ireland, our team is ready to help you protect what matters most.

Frequently Asked Questions (FAQs)

1. Will mortgage rates go down in 2026 in Ireland?

It is possible, depending on the European Central Bank’s decisions and broader economic conditions. While rates may stabilise or decrease, it is impossible to predict with certainty. Regardless, having mortgage protection in place remains essential.

2. Is mortgage protection compulsory in Ireland?

Yes, for most residential mortgage borrowers, mortgage protection Ireland is a legal requirement under the Consumer Credit Act 1995. There are limited exemptions for those unable to obtain cover due to age or health.

3. What are red flags on a mortgage application?

Common red flags include unpaid debts, gambling transactions, irregular spending patterns, insufficient savings history, and frequent job changes. Cleaning up your finances before applying can make a big difference.

4. How much does mortgage protection cost in Ireland?

The mortgage protection insurance cost varies based on your age, health, mortgage amount, and term. A healthy non-smoker in their 30s might pay between €20 and €40 per month for a €300,000 mortgage over 30 years.

Disclaimer: This article provides general information and should not be considered personalised financial, insurance, or mortgage advice. Mortgage protection requirements and costs change periodically, and individual circumstances vary. Always consult with our qualified financial advisors or insurance professionals before making significant financial decisions.