As we navigate through 2026, Irish taxpayers are facing a landscape of new regulations, updated thresholds, and evolving opportunities for tax planning Ireland. Whether you’re a PAYE worker, self-employed professional, or business owner, understanding the changes in the Irish tax year 2026 is essential to maximising your financial position and minimising your tax liability legally and efficiently.

At Money Maximising Advisors Limited, we’ve been guiding individuals and businesses through the complexities of Ireland’s tax system for years. Our team of Experienced Tax Advisors, Certified Financial Planners (CFP), and Qualified Financial Advisors (QFA) is here to help you make sense of the latest developments and implement effective Ireland tax planning strategies tailored to your unique circumstances.

In this comprehensive guide, we’ll explore what’s new in 2026, highlight key changes that affect your wallet, and provide practical advice on how to optimise your tax position throughout the year.

Understanding the Irish Tax Year 2026: Key Changes and Updates

The Irish tax year 2026 runs from 1st January to 31st December 2026, and several important changes have been introduced that impact both individuals and businesses across Dublin, Galway, and the entire country.

Updated Tax Bands and Rate Thresholds

One of the most significant changes for 2026 involves adjustments to tax bands and standard rate cut-off points. These modifications directly affect how much of your income is taxed at the lower 20% rate versus the higher 40% rate. For tax planning for individuals Ireland, understanding where your income falls within these bands is the foundation of effective tax optimisation.

The standard rate band has been widened for both single individuals and married couples, meaning more of your income is taxed at the lower rate before you hit the higher threshold. This represents a real opportunity for middle-income earners to retain more of their hard-earned money.

Enhanced Personal Tax Credits

Personal tax credits have also been increased for 2026, providing additional relief for taxpayers. The employee tax credit, personal tax credit, and earned income credit have all seen modest increases, which accumulate to create meaningful savings throughout the year.

For those seeking tax advisory Ireland services, it’s worth noting that these credits are often underutilised or misclaimed, resulting in overpayment of tax that could have been avoided with proper planning.

USC and PRSI Adjustments

The Universal Social Charge (USC) and Pay Related Social Insurance (PRSI) have undergone modifications in 2026. The USC entry threshold has been raised, meaning more low-income earners are exempt from this charge entirely. Additionally, certain USC bands have been adjusted to provide relief for middle-income households.

Ireland Tax Planning Strategies That Actually Work in 2026

Effective tax planning advice Ireland isn’t about finding loopholes—it’s about understanding the legitimate reliefs, credits, and allowances available to you and structuring your finances accordingly.

Maximising Pension Contributions

One of the most powerful Ireland tax optimization tools available is pension contribution relief. Contributions to approved pension schemes receive tax relief at your marginal rate, meaning higher earners can claim 40% relief on qualifying contributions.

For 2026, the age-related percentage limits remain in place, allowing individuals to contribute significant amounts based on their age:

- Under 30 years: 15% of earnings

- 30-39 years: 20% of earnings

- 40-49 years: 25% of earnings

- 50-54 years: 30% of earnings

- 55-59 years: 35% of earnings

- 60 and over: 40% of earnings

If you haven’t maximised your pension contributions yet this year, now is the time to enquire now about how this strategy could benefit your overall tax planning Ireland approach.

Property-Related Tax Reliefs

Property owners in Dublin, Galway, and across Ireland should be aware of several valuable tax reliefs available in 2026. The Rent-a-Room Relief scheme continues to allow homeowners to earn up to €14,000 tax-free annually from renting a room in their principal private residence.

Additionally, landlords can claim various expenses against rental income, including mortgage interest (subject to certain restrictions), maintenance costs, insurance, and management fees. Proper documentation and strategic timing of expenses can significantly reduce your taxable rental income.

Corporate Tax Planning Ireland Considerations

For business owners and self-employed professionals, corporate tax planning Ireland strategies become even more crucial in 2026. The corporation tax rate structure remains competitive, but smart planning around timing of income recognition, capital allowances, and expense claims can substantially impact your tax position.

Research and Development (R&D) tax credits continue to offer significant benefits for qualifying companies, with the credit providing a valuable cash injection for innovative businesses investing in new technologies, products, or processes.

Tax Reliefs and Credits Available in Ireland for 2026

Understanding and claiming all available tax reliefs is fundamental to effective tax planning Ireland strategy. Here are some key reliefs you shouldn’t overlook:

Medical Expenses Relief: You can claim tax relief on qualifying medical expenses at your standard rate of tax (20%). This includes expenses not covered by your health insurance, such as certain dental treatments, optical costs, and prescribed medical aids.

Home Carer’s Tax Credit: If you’re caring for a dependent person, you may qualify for the Home Carer’s Tax Credit, worth up to €1,700 in 2026.

Tuition Fees Relief: Tax relief is available on qualifying tuition fees for approved undergraduate and postgraduate courses, providing valuable support for continuing education.

Employment and Investment Incentive (EII): For those with investment capacity, the EII scheme offers tax relief at your marginal rate for investments in qualifying Irish companies, subject to certain conditions and holding periods.

To explore which reliefs apply to your situation and ensure you’re not leaving money on the table, book now for a consultation with our qualified advisors.

Tax Planning Consultants Ireland: When Professional Help Makes Sense

While some aspects of tax planning can be managed independently, working with experienced tax planning consultants Ireland professionals often pays for itself many times over, particularly when dealing with:

- Complex income sources (rental properties, foreign income, investments)

- Business structures and company tax optimisation

- Inheritance planning and estate management

- Redundancy payments and severance packages

- Large capital transactions

At Money Maximising Advisors Limited, we take a holistic approach to your financial situation, considering not just your immediate tax position but your long-term financial goals, retirement planning, and wealth preservation strategies.

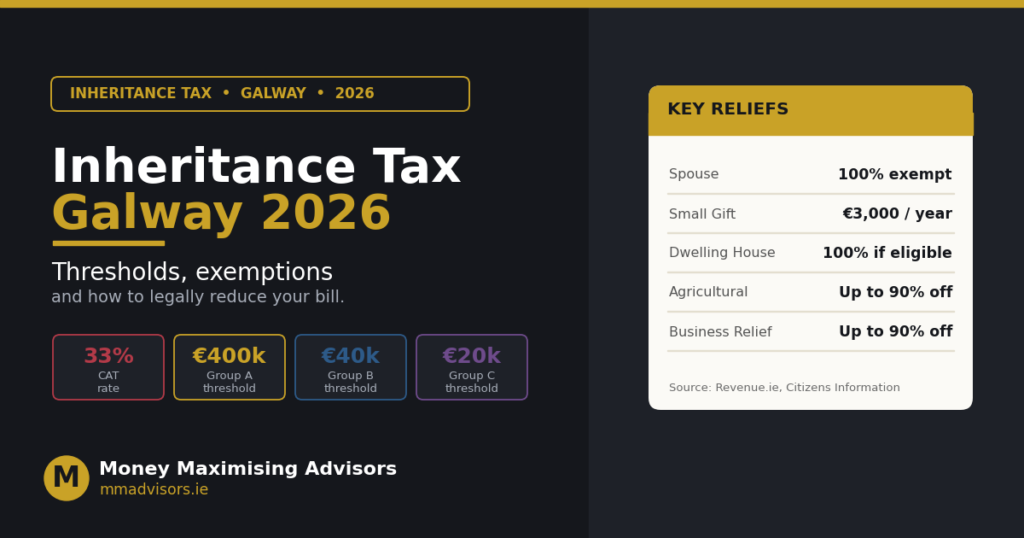

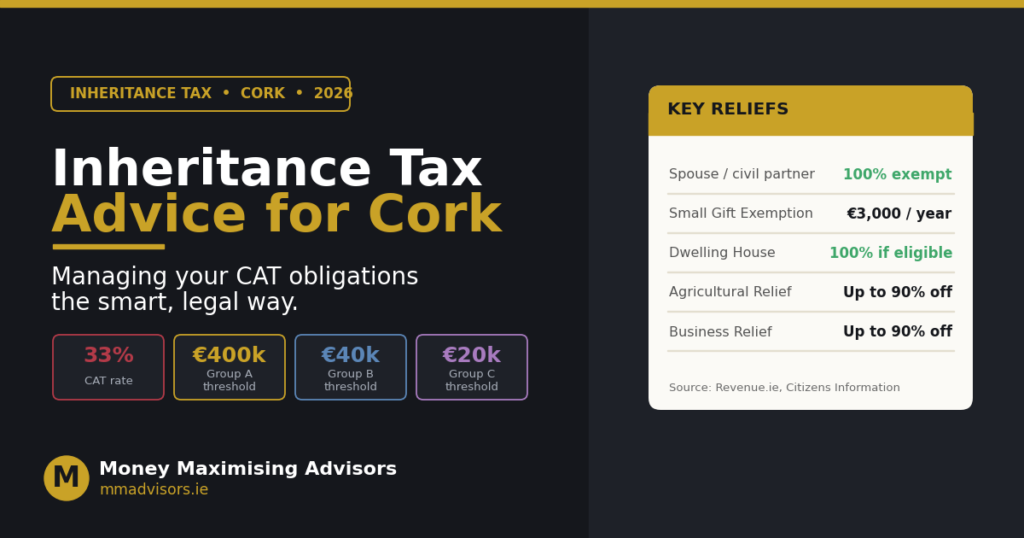

Inheritance and Estate Planning: Critical Considerations for 2026

One area that deserves special attention in your Irish tax year 2026 planning is inheritance and estate planning. Ireland’s Capital Acquisitions Tax (CAT) regime can significantly impact wealth transfer between generations if not properly managed.

Current CAT thresholds determine how much you can inherit tax-free depending on your relationship to the person giving the gift or inheritance. Group A (parent to child) currently allows for the most generous threshold, but careful planning can help maximise what you can pass on or receive.

For comprehensive guidance on minimising inheritance tax exposure, consider reading our detailed article on Inheritance Tax Advice In Ireland: How to Avoid Paying Inheritance Tax in Ireland?

Strategic gifting, proper use of annual exemptions, and timing of transfers can all play a role in Irish tax planning services focused on estate preservation. Additionally, understanding how life insurance policies can be structured to cover potential inheritance tax liabilities is an essential component of comprehensive planning.

For more specific strategies, our article on Inheritance Tax Advice In Dublin, Ireland: How can I Reduce My Inheritance Tax in Ireland? provides actionable insights tailored to Irish residents.

Common Tax Planning Mistakes to Avoid in 2026

Even well-intentioned taxpayers can make costly errors when it comes to tax planning. Here are some pitfalls to watch out for:

Failing to keep proper records: Without adequate documentation, you may miss out on legitimate expense claims or face difficulties if Revenue requests information.

Missing tax return deadlines: Late filing can result in penalties and surcharges that quickly negate any tax savings you’ve achieved.

Overlooking available reliefs: Many taxpayers fail to claim credits and reliefs they’re entitled to simply because they’re unaware they exist.

Poor timing of income and expenses: Strategic timing of when you receive income or incur deductible expenses can meaningfully impact your tax position, particularly if you’re close to band thresholds.

Not seeking professional advice: Complex tax situations often benefit from expert guidance. The cost of professional tax planning Ireland services is typically far less than the potential savings they uncover.

If you’re unsure where to turn for reliable guidance, our article Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax? can point you in the right direction.

Gift Planning and Family Wealth Transfer in 2026

Gift planning remains an effective tool for Ireland tax planning strategies, allowing you to transfer wealth to family members while managing your tax exposure. Understanding the small gift exemption (€3,000 per donor per recipient annually) and how it interacts with CAT thresholds is essential for multi-year planning strategies.

For detailed information on this topic, see our comprehensive guide on How Much Money Can You Gift to a Family Member Tax-Free in Ireland?

Strategic gifting can be particularly effective when combined with other planning techniques such as pension contributions, investment in qualifying assets, and proper use of exemptions and reliefs.

Taking Action: Your Next Steps for Effective Tax Planning

Effective tax planning Ireland isn’t a one-time event—it’s an ongoing process that requires regular review and adjustment as your circumstances change and tax legislation evolves.

Here’s how to get started:

- Gather your financial information: Compile records of all income sources, expenses, investments, and assets.

- Review your current tax position: Understand where you stand now and identify areas for potential optimisation.

- Explore available reliefs and credits: Ensure you’re claiming everything you’re entitled to.

- Consider your long-term goals: Effective tax planning aligns with your broader financial objectives, including retirement, education funding, and wealth transfer.

- Seek professional guidance: Working with qualified advisors ensures you’re making informed decisions based on current legislation and best practices.

Conclusion

The Irish tax year 2026 presents both challenges and opportunities for Irish taxpayers. With updated thresholds, enhanced credits, and evolving legislation, staying informed and proactive is essential to optimising your tax position.

At Money Maximising Advisors Limited, we’re committed to helping individuals and businesses across Dublin, Galway, and throughout Ireland navigate the complexities of the tax system. Our expertise in tax planning for individuals Ireland, corporate tax planning Ireland, and comprehensive financial planning positions us to deliver tailored solutions that align with your unique circumstances and goals.

Don’t leave your tax planning to chance. Whether you need guidance on pension contributions, inheritance strategies, property tax reliefs, or comprehensive financial planning, our team is here to help.

Contact Us today to discuss your specific situation, or Book an Appointment for a comprehensive review of your tax planning opportunities in 2026 and beyond.

Frequently Asked Questions

1. What is tax planning and why is it important in Ireland?

Tax planning is the strategic analysis and arrangement of your financial affairs to minimise tax liability legally while achieving your financial goals. In Ireland, where tax rates can be significant, effective planning helps you retain more of your income, maximise available reliefs and credits, and build wealth more efficiently.

2. How does tax planning work in Ireland?

Tax planning in Ireland works by utilising legitimate reliefs, credits, exemptions, and allowances available under Irish tax law. This includes strategies like maximising pension contributions, claiming all eligible tax credits, timing income and expenses strategically, and structuring investments and gifts tax-efficiently. Professional advisors help identify opportunities specific to your circumstances.

3. What are the basic tax planning strategies for individuals in Ireland?

Basic strategies include maximising pension contributions for tax relief, claiming all applicable tax credits, utilising property-related reliefs like Rent-a-Room Relief, claiming medical expense relief, timing capital gains strategically, and using annual gift exemptions effectively. Keeping accurate records and filing returns on time are also fundamental to effective tax management.

4. What tax reliefs and credits are available in Ireland?

Ireland offers numerous reliefs including personal tax credits, employee tax credits, earned income credits, home carer’s credit, medical expenses relief, tuition fees relief, pension contribution relief, rent-a-room relief, and various property-related allowances. Investment incentives like the Employment and Investment Incentive (EII) and generous small gift exemptions for wealth transfer are also available.

5. How can I legally reduce my tax bill in Ireland?

You can legally reduce your tax bill by maximising pension contributions, claiming all eligible tax credits and reliefs, strategically timing income and deductible expenses, utilising property tax reliefs if applicable, making charitable donations that qualify for relief, and structuring investments tax-efficiently. Working with qualified financial advisors ensures you identify all legitimate opportunities without risking non-compliance.

(Disclaimer: This article provides general information and should not be considered personalised financial or tax advice. Irish tax laws change periodically, and individual circumstances vary significantly. Tax planning strategies that work well for one person may not be appropriate for another. Always consult with qualified financial advisors or tax professionals at Money Maximising Advisors Limited before making significant financial decisions. While we strive for accuracy, tax legislation can change, and this article should not be relied upon as the sole basis for financial decisions.)