Unlock the value of your property with equity release mortgages in Ireland. Learn about the qualifying criteria, loan options, and how much you can access. Explore scenarios where equity release can transform your financial situation, from home improvements to supporting family or investing in property.

Unlock Your Home’s Potential: Equity Release Mortgages in Ireland

At Money Maximising Advisors, we specialise in helping homeowners and property investors unlock the wealth hidden within their homes. Equity Release Mortgages Ireland are a powerful tool, allowing you to access the funds tied up in your property without the stress of selling or the burden of moving out. This financial solution is particularly valuable for those looking to make home improvements, invest in a second property, or manage inheritance tax bills—essentially putting your hard-earned equity to work for you. Our team understands the fluctuating rates and complex criteria that come with RBSA lending and remortgaging options. We ensure that our clients are well-informed about the interest rates on equity release in Ireland and guide them through the process seamlessly.

Equity Release Mortgages in Ireland Explained

Equity Release Mortgages Ireland have become a vital option for homeowners looking to access the value tied up in their properties. At Money Maximising Advisors, we see this trend reflected in our daily interactions with clients who wish to unlock funds without selling their homes. The process involves leveraging the equity built up over years of homeownership. This approach allows individuals to address immediate financial needs—whether it’s paying off debt, funding renovations, or supporting loved ones—while retaining ownership of their cherished home. Many clients inquire about how much they can get from equity release in Ireland. The answer varies based on factors like property value, existing mortgage balance, and individual lending criteria. Our role is to facilitate informed decisions by clarifying these variables and providing tailored advice on options available through reputable lenders. We ensure that every client understands the nuances of equity release mortgage rates in Ireland. Our comprehensive support enables property owners to navigate this landscape confidently, transforming potential challenges into opportunities for growth.

Benefits of Using Equity Release on Your Home

Unlocking the value tied up in your property can be a game-changer. For many homeowners, Equity Release Mortgages Ireland offer an immediate source of liquid assets. With these funds, you can renovate your home to increase its value or cover unforeseen medical expenses. Imagine transforming that seldom-used attic into a vibrant home office or gym without dipping into your savings. Moreover, equity release allows for personal investments. You could fund a new business venture or support your children’s educational pursuits. This financial flexibility ensures that you remain in control of your assets while catering to pressing needs. Another advantage lies in alleviating monthly burdens through debt consolidation. By releasing equity from your house Ireland, you streamline repayments and improve cash flow—crucial for those seeking peace of mind during uncertain times. Equity release brings financial freedom and empowers homeowners to use their property’s wealth strategically. Whether addressing current obligations or planning future endeavors, leveraging home equity opens doors previously considered unreachable.

What Can You Use the Funds For?

There are numerous reasons you might choose to release equity from your home. One of the most common is renovating or improving your property. This could include anything from updating a kitchen to adding an extension. Many homeowners also use equity release for funding education expenses. Whether it’s paying for college tuition or enrolling in specialized training, having access to these funds can make a significant difference in personal development and career opportunities. Medical expenses are another area where equity release can be beneficial. Unexpected health issues often come with hefty bills that aren’t always covered by insurance. Additionally, supporting loved ones is a growing reason for releasing equity in Ireland. Parents may wish to help their children with a deposit on their first home or assist with financial challenges they face. Others look at equity release as a means of consolidating debt, allowing them to manage monthly payments more effectively. This can provide peace of mind and greater control over financial obligations.

You might also like our post on Unlocking Home Wealth: Expert Guide To Equity Release.

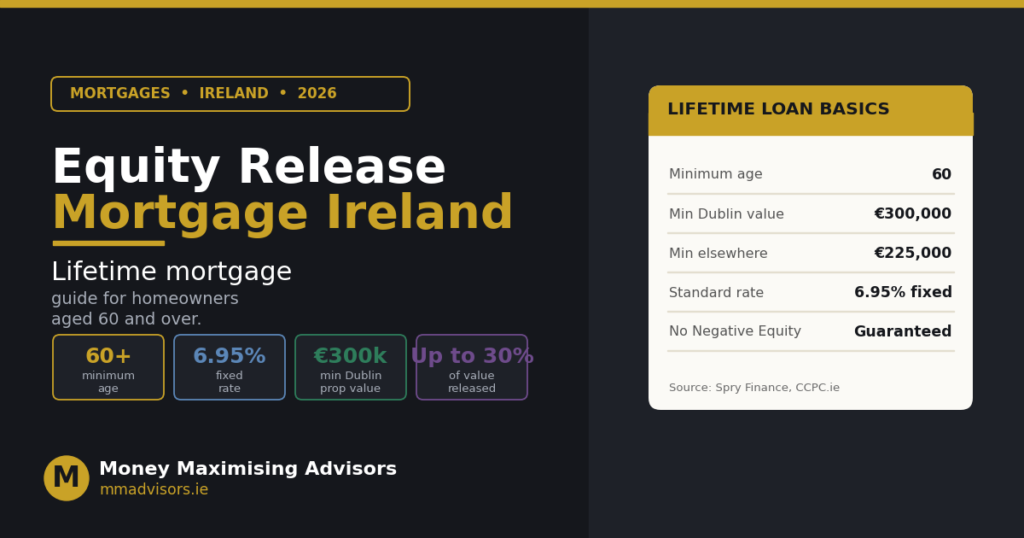

Key Criteria to Qualify

Understanding the key criteria for Equity Release Mortgages Ireland is essential. Not everyone qualifies, so it’s vital to be informed. First and foremost, you must own your home outright or have a significant amount of equity in your property. This forms the basis for what lenders will assess. Residency also plays a crucial role. Most schemes require that the property is your main residence. Some options are available for buy-to-let properties, but the qualifications can differ. Age matters too; typically, applicants need to be at least 55 years old. The reasoning is simple—lenders want assurance that their investment aligns with life expectancy and financial stability. Your credit score and income verification may come into play depending on the type of equity release product you’re considering. Each lender has unique requirements, so consulting with experts like Money Maximising Advisors can help clarify these details.

Property Requirements

When considering equity release on your property, understanding the property requirements is crucial. Lenders often have specific criteria that must be met to qualify. The condition of your home plays a significant role. Typically, properties should be in good repair and well-maintained. This ensures that the lender’s investment is secure. Location also matters. Most lenders prefer prime residential areas with strong market values. If your property sits in a less desirable area, it might impact the amount you can release. Additionally, there are minimum value thresholds to consider. Properties generally need to meet or exceed a certain market value for eligibility. The type of accommodation can influence options available through equity release schemes. While traditional homes are widely accepted, some lenders may hesitate with unique or multi-unit properties. Lastly, check for restrictions on leasehold arrangements versus freehold ownership, as this could affect approval rates. Always consult professionals like Money Maximising Advisors for tailored advice specific to your situation.

Ready to take the next step? Book a consultation.

Related read: Equity Release In Ireland: What You Need To Know.

Loan Amounts

Understanding the loan amounts available through equity release is crucial. The sum you can borrow largely depends on your home’s value and the percentage of equity you’ve built up. Lenders typically assess both current market conditions and individual circumstances to determine eligibility. For those considering this option, it’s essential to be realistic about how much you can actually access. While some homeowners may dream of unlocking significant funds, lenders often have caps based on various risk factors. Typically, borrowers can access anywhere from a modest portion to a more substantial chunk of their home’s value. The amount isn’t arbitrary; it reflects an intricate balance between risk management for lenders and financial opportunity for borrowers. Consulting with us at Money Maximising Advisors will help clarify your options. We ensure that our clients understand not just the potential benefits but also any limitations tied to their unique situation regarding loan amounts.

Need tailored guidance? Enquire now.

Recommended: Equity Release Calculator For Buy To Let Mortgages.

Terms

Understanding the terms of an equity release mortgage in Ireland is crucial. These terms can significantly impact your financial planning and long-term strategy. Typically, equity release products come with fixed or variable interest rates. Fixed rates offer stability, while variable options may provide lower initial rates but can fluctuate over time. The loan’s duration is another key aspect. Most plans allow for a flexible repayment schedule, tailored to your needs and circumstances. This flexibility can be particularly advantageous if you anticipate changes in income or expenses down the line. Additionally, it’s essential to consider any fees associated with the process. Some lenders might charge arrangement fees or early repayment penalties that could affect your overall cost. We at Money Maximising Advisors ensure you fully understand all these elements before proceeding. Transparency reduces future headaches and ensures informed decision-making throughout your journey into leveraging home equity.

How Much Can You Access?

How much equity can you unlock from your home in Ireland? This is a common question homeowners have when considering Equity Release Mortgages. The answer isn’t one-size-fits-all. It depends on factors like the value of your property and how much mortgage you still owe. Most lenders use a loan-to-value ratio to determine eligibility. Typically, this ratio allows you to access a percentage of your home’s current market value—usually up to 70% for standard properties. However, buy-to-let and pension-related homes may be limited to lower amounts. The type of repayment plan you choose also plays a role. Whether opting for interest-only or capital plus interest repayments will influence what’s available to you. Consulting with us at Money Maximising Advisors can provide clarity on specific numbers tailored to your unique circumstances.

You might also like our post on Senior’S Equity Release: Lifetime Loans In Dublin.

Interest Rates Available

Interest rates are a crucial factor when considering an Equity Release Mortgage in Ireland. These rates can vary significantly based on several factors, making it essential to stay informed and shop around. The current market offers a range of interest rates tailored to different needs and circumstances. For homeowners looking to release equity from their houses, understanding these options is vital. Fixed-rate mortgages provide stability, allowing you to lock into a rate for a specified period. On the other hand, variable-rate options may offer lower initial rates but come with the risk of future increases. Each type has its advantages depending on your financial goals and risk tolerance. It’s important to compare offers across various lenders. An experienced mortgage broker can help guide you through this process, ensuring you secure the best possible deal that aligns with your long-term plans.

Ready to take the next step? Book a consultation.

Related read: How To Remortgage To Release Equity From Your Property.

Financial Requirements to Qualify

The financial requirements to qualify for an equity release mortgage in Ireland are crucial. Lenders will closely assess your income, debts, and credit history. At Money Maximising Advisors, we help clients navigate these essential criteria with ease. One primary factor is your ability to repay the loan. This often involves a thorough review of your current financial situation. Applicants must demonstrate that they have sufficient income to cover monthly repayments comfortably. Your credit score plays a significant role as well; higher scores generally indicate lower risk for lenders. Additionally, you’ll need documentation supporting consistent earnings—such as payslips or tax returns can be beneficial during this assessment phase. Lenders also consider other outstanding debts you might have. A high debt-to-income ratio could impact your eligibility positively or negatively depending on the lender’s policies. Understanding these nuances ensures that you’re better prepared when applying for an equity release mortgage in Ireland. Partnering with experts like Money Maximising Advisors can make the journey smoother and more successful.

Need tailored guidance? Enquire now.

Principal Private Residence

Understanding the Principal Private Residence (PPR) is crucial when considering Equity Release Mortgages Ireland. The PPR refers to your main home where you reside most of the year. This property serves as the primary collateral for securing a mortgage. When releasing equity from your house in Ireland, lenders often assess the value and condition of your PPR. This ensures that their investment is protected while providing you with necessary funds. The process typically involves an appraisal to determine how much equity can be unlocked. Each lender has different criteria, making it essential to consult with experts who understand local regulations and market trends. The amount you can access significantly depends on factors such as your age, income, and current mortgage balance. It’s not just about unlocking cash; it’s about leveraging a valuable asset without having to move or sell your beloved home. By working together, we empower homeowners like you to make informed decisions regarding home equity loans and potential financial opportunities lying right within your front door.

Recommended: How Releasing Equity From Your Property Can Unlock Financial Flexibility: Mortgage Solutions Explained.

Residential Investment Properties

Investing in residential properties can be a smart way to build wealth. When considering equity release mortgages Ireland, these investments offer another layer of opportunity. By leveraging the value built up in your investment properties, you can access funds for further real estate ventures or personal financial goals. Many landlords and property owners are unaware that equity release options exist specifically tailored to them. This allows individuals to unlock cash from their properties without selling, maintaining rental income streams while gaining liquidity. The process is straightforward but requires careful consideration of terms and market conditions. Loan-to-value ratios generally play a significant role; most lenders cap this around 70%. Understanding these nuances ensures you make informed decisions that align with your investment strategy. When exploring how much you can get from equity release Ireland on residential investment properties, partnering with experienced advisors like Money Maximising Advisors provides clarity and confidence throughout the journey.

Real-Life Scenarios

- How One Couple Unlocked €75,000 from Their Home — Without Touching Their Savings

John and Mary, both teachers with a combined income of €100,000, own a home valued at €350,000. With a mortgage balance of €200,000, they had €150,000 in equity. By remortgaging for €225,000, they cleared their existing loan and freed up €75,000 in cash.They can now renovate their home, support their children’s education, help with a second property purchase, or reduce debt — all without dipping into savings. - Turning Equity Into Opportunity: A Smart Divorce Settlement Solution

Tommy and Jane recently decided to divorce. Their family home is valued at €400,000 with an outstanding mortgage of €100,000. Jane is staying in the home with their 3 children, while Tommy will leave ownership if he receives €100,000 as part of the settlement. Jane remortgaged the property for €250,000 using equity release. With this, she cleared the old mortgage, paid Tommy his €100,000, and used the remaining €50,000 to renovate the home. - Remortgage & Consolidate Loans to Reduce Monthly Repayments

James and Elaine, civil servants in their early 50s with 3 dependent children, were struggling with cash flow due to loan repayments and college fees. Their home is valued at €350,000 with €150,000 outstanding on the mortgage (€1,500/month repayments). They also had: A home improvement loan (€500/month) A personal loan (€250/month) Their total monthly repayments were €2,250. By remortgaging and consolidating into one loan, their monthly outgoings reduced to €1,850 — freeing up €450 monthly to ease cash flow until their children finish college. They plan to restructure again later to clear their mortgage earlier. - Remortgage for a House Extension to Generate Income

Sean & Michelle own a home valued at €440,000 with €170,000 remaining on their mortgage. Living beside a university, they were constantly asked about accommodation. They decided to build an extension at the back of their house to rent to students. The extension cost €75,000. They released equity to fund it, increasing their mortgage repayments by €250/month (€3,000 annually). However, they now earn €14,000 annually from student rent — a significant net gain. - Releasing Equity to Buy a Second Property

John owns a home valued at €400,000 with €100,000 left on the mortgage. He wanted to buy a second property but lacked the 30% deposit. He remortgaged his home for €175,000, unlocking €75,000 in equity — which became the deposit for a buy-to-let. He now owns a second income-generating property, an appreciating asset, and achieved this without touching his savings. - Here’s How an Investor Turned Equity Into Expansion

Pat, a property investor, owns 3 buy-to-let properties worth €1 million, generating solid rental income. She wanted to develop a student apartment block and needed a 30% deposit for development finance. Instead of selling assets, she released equity from her existing portfolio. The funds covered the entire deposit, allowing her to move forward without dipping into savings or investors. Pat retained ownership of her properties, secured a new revenue stream, and scaled her portfolio using equity — not cash.

FAQ’S:

- What is an equity release mortgage?

An equity release mortgage allows you to unlock the value built up in your home without selling or moving. You can access funds for renovations, education, debt consolidation, or to help a loved one with a deposit, while still owning your home. - Are equity release mortgages safe?

Yes, when managed properly through regulated lenders. Brokers assess your eligibility and repayment ability and only recommend equity release if it supports your long-term financial stability. - Is it better to remortgage or release equity?

It depends. Remortgaging can secure a better rate, while equity release provides cash for immediate needs. Often, you can do both. - Can I use home equity to clear debts?

Yes. Many homeowners consolidate high-interest debts like credit cards or personal loans with equity release. - Does it cost money to release equity?

Yes — costs may include valuation, legal, or processing fees. However, competitive terms often outweigh these costs. - Can I release equity as cash?

Yes. You can access up to €100,000 as a lump sum for approved purposes (e.g., renovations, education, helping family). - Can equity release repay an existing mortgage?

Yes. Many use equity release to refinance or clear an existing mortgage. - Can I release equity to buy out a partner’s share?

Yes, it’s common in separation/divorce cases. - What is the LTV for buy-to-let equity release?

Typically up to 70% for loans up to €1 million, and up to 65% for €1–1.25 million. Pension-related buy-to-lets are capped at 50%. - Is a home equity loan a good idea?

Yes — if used strategically. It can unlock capital for reinvestment, debt repayment, or personal financial management. - Can it be repaid early?

Yes. Most lenders allow early repayment, often penalty-free. - Is leveraging equity better than a personal loan?

Often, yes. Equity release generally offers lower rates and larger amounts than personal loans, plus potential tax benefits for investors.

CONCLUSION

In summary, equity release mortgages in Ireland offer an excellent opportunity for homeowners to unlock the value in their properties. Whether your goal is to fund a major renovation, consolidate debts, or simply access cash for personal use, this financial product can provide significant benefits. Understanding the various criteria and options available will empower you to make informed decisions tailored to your specific needs.

Remember that every situation is unique. The examples provided show how versatile equity release can be across different scenarios—from supporting families through transitions like divorce to enabling investments in additional real estate. It’s about making your home work for you while maintaining financial security and peace of mind.

To maximise the potential of your equity release experience, consult with a knowledgeable mortgage broker who can guide you through the process.

Start your journey towards unlocking your financial potential today! Contact Money Maximising Advisors now to discuss how you can make the most of your home’s equity.