Whether you’re an individual, a company, or want to leverage your pension for property investment, Buy-to-Let mortgages in Ireland give you the means to build wealth through property ownership and rentals. Explore flexible options designed for investors across all backgrounds.

Buy-to-Let Mortgages in Ireland

Introduction to Buy-to-Let

Start or enhance your property portfolio with a Buy-to-Let Mortgage. These loans are designed for individuals, companies, or pension schemes looking to purchase residential properties for rental purposes. With flexible options tailored to various borrower types, you can find the perfect fit for your investment goals.

Three Types of Buy-to-Let Mortgages

There are three main types of Buy-to-Let Mortgages available:

- Individual Buy-to-Let: For personal investments

- Company Buy-to-Let: For businesses and Special Purpose Vehicles (SPVs)

- Pension Buy-to-Let Mortgage: Using retirement funds for property investment

Individual Buy-to-Let

This type allows private investors to purchase properties solely for rental income. It’s ideal for those starting their journey into property investment in Ireland.

Company Buy-to-Let

This option is suited for companies or SPVs focusing on property portfolios. It offers unique benefits tailored to business needs.

Pension Buy-to-Let Mortgage

Leveraging pensions can be advantageous, offering tax efficiencies and long-term growth opportunities within your retirement plan.

BUY TO LET: INDIVIDUALS/JOINT APPLICANTS

If you love the idea of building your property portfolio, you’ve probably heard about Buy-to-Let mortgages. These are designed specifically for individuals looking to invest in properties they can rent out.

As an individual or joint applicant, applying for a Buy-to-Let mortgage lets you tap into the potential of rental income while benefiting from property appreciation over time. It’s a great way to start your journey toward financial independence.

The process is quite straightforward. You’ll need to meet specific criteria regarding income and credit scores. Lenders want assurance that you’re capable of managing both the loan repayments and any associated costs with maintaining a rental property.

You might also like our post on Everything You Need To Know About Using A Spv Company For Buy To Let Property.

This option opens doors not just for seasoned investors but also newcomers eager to explore the world of real estate investment. With various options available, it’s essential to research thoroughly and choose what aligns best with your goals.

BUY-TO-LET MORTGAGES FOR SPECIAL PURPOSE VEHICLES (SPVs/Companies)

Buying property for rental can be a lucrative investment, especially when using a Special Purpose Vehicle (SPV). An SPV is essentially a company created solely to manage properties. This approach streamlines the process and can offer significant tax benefits.

One major advantage of using an SPV is that it separates your personal finances from your property investments. This structure protects you from potential risks associated with buying rental properties.

When applying for buy-to-let mortgages through an SPV, lenders will assess the business’s financial health rather than your personal income. This can make securing funding easier if you have multiple properties or are expanding your portfolio.

Many investors are now turning to SPVs as they navigate the complex landscape of rental property investment. It’s worth exploring if you’re serious about growing your real estate assets in Ireland.

PENSIONS MORTGAGE

Pensions mortgages are becoming an intriguing option for those looking to invest in property. This type of mortgage allows you to use your pension fund as a way to secure financing.

Related read: Your Guide To Buy To Let Mortgages In Ireland: Options For Individuals.

With a pension buy-to-let mortgage, you can potentially grow your retirement savings while benefiting from rental income. It’s an appealing alternative for individuals who want more control over their investments.

This option is particularly attractive if you’re thinking about diversifying your portfolio. By leveraging your pension, you can enter the real estate market without dipping into other assets.

Ready to start your property journey? Book a consultation and get personalised guidance.

However, it’s important to understand the specific regulations around this product. Not all pensions will qualify, and there may be restrictions on what types of properties can be purchased through this scheme.

Want to maximise your property investments? Enquire now and discover your options.

Engaging with a knowledgeable broker or financial advisor is crucial here. They can help navigate the complexities involved and ensure that this route aligns with your long-term goals.

APPROVED RETIREMENT FUND (ARF) PENSION BUY TO LET MORTGAGE

The Approved Retirement Fund (ARF) pension buy-to-let mortgage is a unique option for those looking to invest in property through their retirement savings. This approach allows individuals with an ARF to use their funds as a deposit for purchasing rental properties.

Using your ARF can offer significant advantages, such as potential tax efficiencies. This can make it an attractive choice for older investors aiming to diversify their income streams during retirement.

Recommended: Buy To Let Mortgages In Ireland: Find Our Best Rates.

However, navigating the application process can be complex. Lenders may require specific documentation and have particular criteria regarding the property involved.

This type of buy-to-let mortgage opens up avenues that weren’t previously accessible for retirees interested in real estate investment. It’s essential to understand both the benefits and limitations before diving into this opportunity.

INDIVIDUAL OR COMPANY BUY TO LET MORTGAGE: WHICH BEST SUITS YOU?

Deciding between an individual or a company buy-to-let mortgage can feel overwhelming. Each has its unique advantages, depending on your circumstances and goals.

An individual buy-to-let mortgage is often simpler to arrange. It’s ideal if you’re just starting out in property investment. You will manage the property under your name, which can make tax filing straightforward.

On the other hand, a company or Special Purpose Vehicle (SPV) approach might suit seasoned investors. By setting up an SPV, you separate personal finances from rental income. This structure may offer certain tax benefits as well.

Buying through a company could also appeal if you plan to build a larger portfolio in Ireland. Lenders view applicants differently based on their approach—so understanding these nuances is crucial before making your choice.

You might also like our post on Equity Release Calculator For Buy To Let Mortgages.

BUY TO LET INDIVIDUAL/JOINT APPLICATION MORTGAGE CRITERIA

When applying for a Buy to Let mortgage as an individual or joint applicant, there are specific criteria you need to meet. These requirements ensure borrowers can successfully manage their investment.

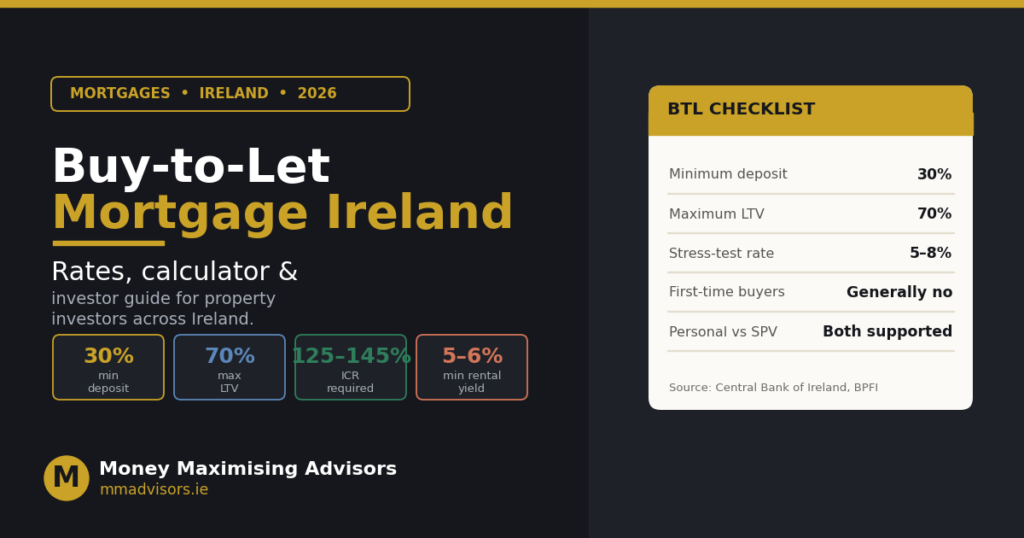

First, the property must be located in an urban area with a population of at least 3,000 and in a habitable condition. Lenders want assurance that tenants will be attracted to the location and that the property is ready for occupancy.

Additionally, up to four applicants are allowed per application. However, at least one must reside in Ireland. Your combined earnings play a significant role; typically, lenders look for evidence of a stable income.

Borrowings usually require a minimum deposit of 30%. This down payment demonstrates your commitment and reduces lender risk. Mortgage terms can vary but often extend up to 25 years.

Thinking about investing with your pension fund? Speak with our specialists—book a consultation now.

Many banks also consider rental income potential. It’s essential that the expected rent covers at least 1.2 times the monthly mortgage repayments. This ratio helps safeguard your finances against market fluctuations.

Curious about Buy-to-Let mortgages in Ireland? Reach out to our experts for tailored advice.

THREE TYPES OF BUY TO LET MORTGAGES ARE AVAILABLE.

There are three ways to apply for a Buy-to-Let Mortgage:

- As an Individual borrower

- Through a Company (SPV)

- With your Pension

Each has specific advantages, so it’s important to explore all three to determine which suits your requirements best.

BUY TO LET MORTGAGE CRITERIA

When exploring buy-to-let mortgages in Ireland, understanding the criteria is essential. Lenders have specific requirements that applicants must meet.

Firstly, the property must be located in an urban area with a population of at least 3,000 people. This ensures a steady demand for renters and reduces vacancy risks.

The property should also be in a habitable condition. Lenders are more likely to approve loans for homes that require minimal immediate repairs or renovations.

For individual or joint applications, each applicant’s financial history will come under scrutiny. They typically allow up to four applicants per application but at least one must reside in Ireland.

Additionally, there’s usually a minimum deposit requirement – often set as a percentage of the property’s value. Borrowers need to prepare for this upfront cost when considering their options.

Recommended: How Releasing Equity From Your Property Can Unlock Financial Flexibility: Mortgage Solutions Explained.

FAQs (Frequently Asked Questions)

- What is a Buy-to-Let mortgage?

A Buy-to-Let mortgage allows you to purchase property specifically for renting out to tenants. It’s designed for investors looking to generate rental income and potential capital appreciation.

- Can I get a Buy-to-Let mortgage as an individual?

Yes, individuals can apply for this type of loan. The process considers your financial situation, creditworthiness, and potential rental income from the property.

- What are the benefits of using my pension for a Buy-to-Let mortgage?

Pension Buy-to-Let mortgages allow you to leverage your retirement savings growth into property investment. This can diversify your income streams in retirement.

- How much deposit do I need for a Buy-to-Let mortgage?

Most lenders require at least a 25% deposit, though this can vary depending on the lender and property value.

- Are Buy-to-Let mortgages available to companies or SPVs?

Yes, Special Purpose Vehicles (SPVs) or companies can secure Buy-to-Let mortgages. This structure may offer tax advantages and streamline property management.

CONCLUSION

Whether you are eyeing your first investment property or seeking new avenues through a pension buy-to-let mortgage, understanding the nuances of this market is crucial. The buy-to-let Ireland scene is vibrant, offering numerous opportunities for individuals, companies, and pensions to acquire property buy-to-let options tailored to diverse needs.

Each type of mortgage—be it individual or joint applications, company-focused loans for SPVs, or those designed around retirement funds like ARFs—caters to specific financial goals. Your choice will depend largely on your circumstances and long-term aspirations in the property sector.

To embark on a successful journey in the buy-to-let landscape, it is essential to understand your investment goals, research the available mortgage options, and seek professional advice tailored to your needs. Money Maximising Advisors can guide you through the complexities of the Irish property market, ensuring you make informed decisions that align with your financial aspirations.

Take the first step towards building a profitable property portfolio by reaching out to Money Maximising Advisors today. Contact us for personalised guidance and expert support on your investment journey.