The blog explores the essentials of buy-to-let mortgages in Ireland for both new and seasoned investors. It highlights key benefits such as rental income, potential capital growth, and entry accessibility. Various mortgage types and lending requirements are explained, alongside rate comparisons and advice on using calculators for informed decisions. FAQs provide further clarity on eligibility, financing options, and building property portfolios.

Buy-to-Let Mortgages in Ireland: Understanding the Essentials

The property investment market in Ireland has seen significant growth in recent years, and buy-to-let mortgages have become an appealing option for many investors. Whether you’re looking to start or enhance your property portfolio, understanding the intricacies of these mortgages is essential. A buy-to-let mortgage allows you to purchase a property with the intention of renting it out, offering a steady stream of income while potentially increasing your capital over time.

In Ireland, the process of securing a buy-to-let mortgage is distinct from obtaining a traditional residential mortgage. Lenders typically have different criteria, interest rates, and policies tailored specifically for investment properties. It’s crucial that potential investors familiarise themselves with these requirements before diving into the property market.

As you embark on this journey, it’s important to stay informed about current market trends and developments that may impact your investment strategy. Whether you’re considering buying your first rental property or expanding an existing portfolio, having a solid grasp of buy-to-let mortgages will help facilitate successful decisions.

Benefits of Buy-to-Let Mortgages

Investing in a buy-to-let mortgage in Ireland offers numerous advantages for property owners looking to expand their portfolios. One key benefit is the potential for consistent rental income, providing a steady cash flow that can help cover mortgage repayments and other expenses associated with property ownership.

Moreover, as property values tend to appreciate over time, investors may enjoy capital growth on their investment. This means that not only can you generate income from renting out your property, but you might also see an increase in its value when it comes time to sell.

Buy-to-let mortgages cater to various types of borrowers—individuals, companies (through Special Purpose Vehicles or SPVs), and even pensions. This flexibility allows investors to choose the structure that best suits their financial situation and long-term goals.

Buy-to-let mortgages empower individuals to invest in property with relatively low initial deposits. This accessibility allows more people to enter the rental market and potentially build a lucrative property portfolio over time.

You might also like our post on Buy To Let Mortgages In Ireland: Find Our Best Rates.

Buy-to-Let Mortgage Options

When considering a buy-to-let mortgage, it’s crucial to explore the various options available tailored specifically for the Irish market. Lenders offer a range of products designed to cater to different types of investors and their unique financial situations.

One common option is the standard buy-to-let mortgage, where you can secure financing based on your potential rental income. This type typically requires a higher deposit compared to residential mortgages but offers flexibility in interest rates.

For those interested in building a property portfolio, some lenders provide multi-property buy-to-let mortgages. These packages allow investors to manage multiple properties under one loan, simplifying finances and administration.

Additionally, there are interest-only buy-to-let options that let landlords pay only the interest during the mortgage term. This can help maintain lower monthly payments while focusing on maximizing rental yields and managing cash flow effectively.

Related read: Everything You Need To Know About Using A Spv Company For Buy To Let Property.

Buy-to-Let Mortgage Calculator

When considering a buy-to-let mortgage in Ireland, utilising a mortgage calculator can be an invaluable tool for prospective investors. This online resource allows you to estimate your potential monthly payments and determine what type of property fits within your budget.

Want to learn more about Buy-to-Let mortgages? Enquire now and get personalised advice tailored to your investment goals.

By inputting variables such as the loan amount, interest rate, and term length, you can quickly visualize your financial commitments. It is essential to factor in additional costs like maintenance fees and property taxes when using the calculator.

Ready to get started? Book a consultation now with one of our mortgage experts and take the first step towards your property investment journey.

This tool empowers you to explore different scenarios, helping you assess whether investing in a buy-to-let property aligns with your financial goals. Calculators also give insight into how changes in interest rates could impact future repayments.

In essence, a buy-to-let mortgage calculator acts as a preliminary step towards making informed decisions about securing financing for your investment property in Ireland.

Buy-to-Let Mortgage Interest Rates in Ireland

Buy-to-let (BTL) property is a significant investment opportunity for individuals looking to enhance their wealth through real estate. With its potential for generating rental income and capital appreciation, BTL properties have become increasingly popular among investors.

Recommended: Equity Release Calculator For Buy To Let Mortgages.

Whether you’re a seasoned investor or new to the market, understanding the fundamentals of BTL property is crucial. It involves purchasing residential or commercial properties with the intention of renting them out to tenants rather than living in them yourself.

The appeal of BTL properties lies in their ability to provide a steady stream of income while potentially increasing in value over time. This dual benefit makes them an attractive option for those seeking financial growth through real estate investments.

Investing in BTL property requires careful consideration of various factors such as location, tenant demand, and ongoing maintenance costs. Proper research and planning can help ensure that your venture into the world of rental properties is both profitable and sustainable.

Buy-to-Let Mortgage Requirements

When considering a buy-to-let mortgage in Ireland, understanding the specific requirements is crucial. Lenders have set criteria that applicants must meet to qualify for this type of loan.

You might also like our post on How Releasing Equity From Your Property Can Unlock Financial Flexibility: Mortgage Solutions Explained.

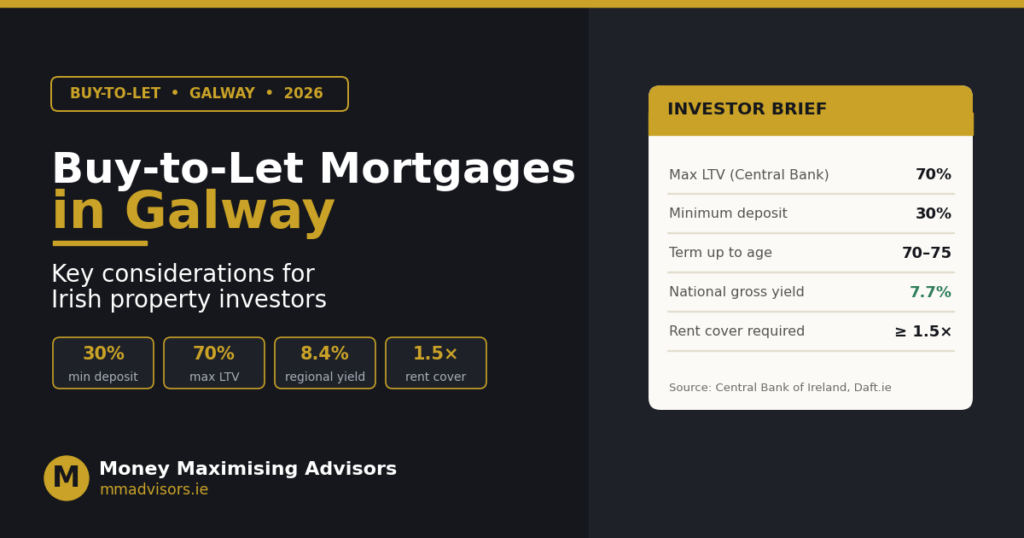

First and foremost, the property you intend to purchase should be located in an urban area with a population of at least 3,000 people. This ensures there’s sufficient demand for rental properties in the region. Additionally, the property must be habitable and hold a minimum value of €115,000.

Applicants can apply individually or as part of a group—up to four people can co-sign on one application. At least one applicant should reside in Ireland or use the property as their primary residence. Together, all income sources must total at least €40,000 annually.

When applying for a buy-to-let mortgage in Ireland, it’s essential to understand the requirements involved. Lenders typically assess your financial stability, including your income and credit history. Most lenders require a minimum deposit, often around 25% of the property’s value. This upfront investment demonstrates your commitment and reduces the lender’s risk.

Secure your property investment future. Schedule a consultation today and explore the best Buy-to-Let mortgage rates Ireland has to offer.

Buy-to-Let Mortgage Rates Ireland

Understanding the current buy-to-let mortgage rates in Ireland is crucial for both seasoned investors and newcomers to the property market.

Curious about Buy-to-Let mortgage options in Ireland? Reach out today to discover how you can start building your property portfolio.

In Ireland, these rates can vary significantly based on several factors. Lenders typically assess your financial stability, loan-to-value ratio (LTV), and the type of property you intend to purchase. Generally, the more substantial your deposit, the lower your interest rate may be.

Related read: How Vacant Property Refurbishment Grants Can Increase Property Value.

Interest rates for buy-to-let mortgages generally range from 3% to 4.5%. This variation depends on individual circumstances such as credit score and financial history.

Lenders also impose different terms based on the length of the loan agreement. Opting for a longer-term mortgage might affect the overall interest paid throughout its duration.

It’s essential to use online tools like a mortgage calculator specific to Ireland. These resources help prospective landlords estimate their monthly repayments under various rate scenarios. Staying informed about current market trends ensures that potential investors make sound decisions when navigating today’s dynamic market environment.

FAQs

1. What is a buy-to-let (BTL) mortgage?

A buy-to-let mortgage is specifically designed for those who wish to purchase property with the intention of renting it out rather than living in it themselves.

Recommended: Unlocking The Path To Homeownership: Demystifying Mortgage Rates In Ireland.

2. What are the different types of buy-to-let mortgages available?

There are several options, including BTL mortgages for individuals, pensions, and special purpose vehicles (SPVs).

3. What are the key requirements for a buy-to-let mortgage in Ireland?

Requirements typically include a minimum deposit, a satisfactory credit score, proof of income, and the property’s rental potential.

4. How do interest rates affect my buy-to-let mortgage?

Interest rates can fluctuate based on the loan type, the lender’s policies, and the borrower’s financial profile.

5. Can I use a buy-to-let mortgage for multiple properties?

Yes, many lenders offer products that allow you to expand your property portfolio under certain conditions.

CONCLUSION

In summary, navigating the world of buy-to-let mortgages in Ireland can seem daunting at first, but understanding the essentials is key to making informed decisions. With various options tailored for individuals, pensions, and companies (SPVs), it’s crucial to do your research before diving in.

The benefits of buy-to-let mortgages are abundant— providing potential rental income alongside property appreciation. Whether you’re a seasoned investor or just starting out, utilising tools like mortgage calculators can help clarify your financial outlook. Remember, interest rates and requirements vary among lenders, so stay updated on current trends.

As you embark on this journey towards property investment success, ensure that you assess your unique situation thoroughly. Consider factors such as location, budget constraints, and market trends when selecting a mortgage option that aligns with your goals. Seek expert advice if needed—after all, choosing the right path could make all the difference in achieving long-term financial growth.

If you’re considering venturing into the buy-to-let market or expanding your existing property portfolio, Money Maximising Advisors are here to help. Our expert team can guide you through the various mortgage options available in Ireland, ensuring you make informed decisions tailored to your financial goals. Contact Money Maximising Advisors today to explore Your Buy-to-Let Mortgage Options!