When it comes to planning for the future, inheritance tax in Ireland can feel like a daunting topic. With the right knowledge and strategies, however, you can navigate this complex landscape with confidence. Understanding how inheritance tax works is crucial not only for safeguarding your wealth but also for ensuring that your loved ones are taken care of after you’re gone.

Many people overlook key aspects of Irish inheritance tax legislation or make common mistakes when it comes to their estate planning. But fear not! There are effective approaches available that can significantly reduce your tax burden and maximise the value passed on to heirs.

Whether you’re just starting to think about inheritance or already have plans in place, this guide will help illuminate essential strategies and tips you need to know. Let’s explore how you can minimise taxes while securing financial peace of mind for both yourself and those you cherish most.

Understanding Inheritance Tax in Ireland

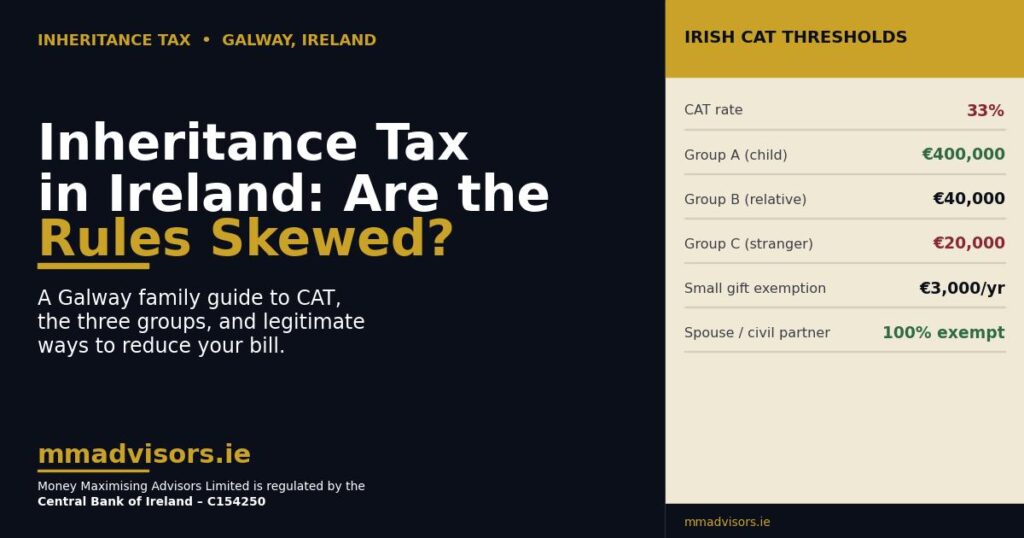

Inheritance tax in Ireland, also known as capital acquisitions tax (CAT), applies when you receive assets from a deceased person’s estate. This can include cash, property, and investments. Understanding the rate at which this tax is charged is crucial for effective financial planning.

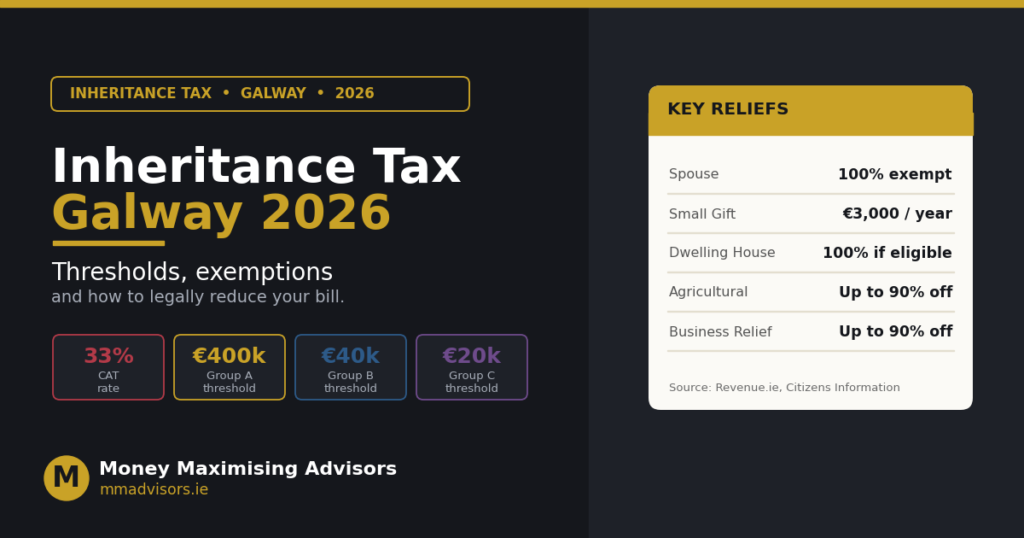

The standard inheritance tax rate stands at 33%, but exemptions may apply depending on your relationship with the deceased. For instance, inheritances between parents and children enjoy a higher threshold compared to siblings or distant relatives.

It’s important to be aware of the thresholds that dictate how much you can inherit before triggering this tax obligation. Knowing these limits allows individuals to strategise effectively and minimise their liabilities.

Navigating through various regulations might seem overwhelming, but taking the time to grasp these principles lays a solid foundation for smart inheritance planning in Ireland.

Common Mistakes to Avoid When Planning for Inheritance Tax

Many people underestimate the importance of timely planning. Waiting until it’s too late can lead to unnecessary tax burdens. Procrastination is a common pitfall that can be easily avoided with proactive measures.

Another frequent mistake is failing to take stock of all assets. Many individuals overlook specific properties, investments, or sentimental items that could significantly impact their inheritance tax liability.

Ignoring available exemptions and reliefs also poses a challenge during estate planning. A lack of awareness about these options means families often miss out on potential savings.

Inadequate communication among family members can complicate matters further. Not discussing wishes openly may result in disputes and misinterpretations down the line.

Relying solely on online resources without professional guidance might lead to misunderstandings about current laws and regulations regarding Irish inheritance tax.

Engaging a qualified tax advisor in Ireland ensures you receive tailored advice suited to your unique circumstances.

Strategies to Reduce Your Inheritance Tax Burden

One effective strategy to reduce your inheritance tax burden is gifting assets during your lifetime. This approach allows you to pass on wealth while taking advantage of lower tax thresholds.

Another method involves making use of the annual gift exemption. Each year, you can give a certain amount without triggering any tax liability. By planning and spreading gifts over several years, you can significantly lower the estate’s value subject to taxation.

Consider investing in life insurance policies that provide liquidity for heirs. These funds can help cover potential taxes, ensuring that beneficiaries receive their intended inheritance intact.

Ensure your property is valued accurately. Overvaluing assets could unnecessarily increase your inheritance tax exposure. Engaging professionals who understand the nuances of Irish inheritance tax will help optimise your strategy effectively.

Contact Money Maximising Advisors Now – Get personalised advice on how to protect more of your assets for your loved ones.

Utilising Exemptions and Reliefs

When navigating the landscape of inheritance tax in Ireland, understanding exemptions and reliefs can be a game-changer. These provisions allow beneficiaries to reduce their taxable estate significantly.

One notable exception is the Group Threshold. It sets limits on how much an individual can inherit from different family members without incurring taxes. Each group—Class A (children), Class B (nieces and nephews), and Class C (others)—has its threshold.

Besides thresholds, specific reliefs exist for agricultural properties and business assets. If you’re inheriting farmland or a family-owned business, these reliefs can lead to substantial savings.

Leveraging these exemptions requires careful planning. Familiarising yourself with current thresholds is essential as they are subject to change over time. This knowledge empowers you to maximise your benefits effectively while minimising liabilities related to Irish inheritance tax.

Setting up Trusts for Inheritance Planning

Setting up trusts can be a smart move in inheritance planning. A trust allows you to control how your assets are distributed after your passing. This provides peace of mind for both you and your beneficiaries.

There are various types of trusts available, each serving different purposes. A discretionary trust offers flexibility, allowing trustees to decide how much each beneficiary receives based on their needs. Alternatively, a fixed trust specifies the amounts allocated to each individual.

Creating a trust also has potential tax benefits. By placing assets in a trust, you may reduce the overall value of your estate subject to Irish inheritance tax limits.

However, it’s crucial to understand the legal implications involved in setting up a trust properly. Engaging with an experienced financial advisor like Money Maximising Advisors or tax professional is essential for navigating this complex area effectively.

Working with a Financial Advisor or Tax Professional

Navigating inheritance tax in Ireland can feel overwhelming. This is where a financial advisor or tax professional becomes invaluable.

These experts understand the intricacies of Irish inheritance tax laws and can tailor strategies to your specific situation. They will help you identify potential liabilities and opportunities for savings that you may overlook.

A good advisor will also assist in setting up trusts, ensuring compliance with regulations while maximising benefits. Their knowledge extends beyond just numbers; they bring clarity to complex legal jargon.

Moreover, working with a professional allows for ongoing support as family circumstances change over time.

With their guidance, you’ll be better positioned to make informed decisions about your legacy, ultimately preserving more wealth for future generations.

FAQs About Inheritance Tax

What is the current inheritance tax limit?

As of now, there’s a threshold that varies based on your relationship with the deceased. Spouses and civil partners generally benefit from higher exemptions compared to distant relatives or friends.

How is the tax calculated?

The value of assets inherited over this limit is subject to a flat rate of 33%. This means careful valuation is essential for accurate calculations.

Are gifts considered under this tax?

Yes, certain gifts within three years before death can also be taxed, so it’s wise to keep track of any significant transfers you make.

Can I contest an inheritance tax bill?

You can appeal if you believe there’s been an error in assessment. Seeking advice from a trained professional like Money Maximising Advisors often helps navigate these processes effectively.

Conclusion

Inheritance tax can be a complex and often daunting topic for many individuals in Ireland. However, with careful planning and the right strategies, it doesn’t have to be overwhelming. Understanding the nuances of inheritance tax is your first step toward effective management.

Avoiding common pitfalls during your inheritance planning will save you money and stress down the line. Implementing strategies to reduce your burden is essential; whether through utilising exemptions or setting up trusts, every little bit helps towards maximising your legacy.

Working with a financial advisor or tax professional can provide invaluable insights tailored specifically to your unique situation. They can help navigate the intricacies of Irish inheritance tax while ensuring that you stay compliant with regulations.

Call Money Maximising Advisors today to speak with our tax experts and start planning to reduce your inheritance tax burden.

related articles [Click now ]

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?