Inheritance tax in Ireland can be a daunting topic. Many individuals and families find themselves grappling with complex regulations and high tax rates when facing the transfer of wealth from one generation to another. The reality is, navigating these waters doesn’t have to feel overwhelming. With some knowledge and strategic planning, you can minimise your exposure to this tax burden while ensuring that your hard-earned assets benefit the ones you love most.

In this guide, we’ll unravel the intricacies of inheritance tax Ireland, explore who needs to pay it, and reveal practical strategies on how to avoid inheritance tax legally. Whether you’re looking for ways to preserve family wealth or seeking guidance on effective estate planning strategies, you’ll find valuable insights here that empower you along the way.

What is Inheritance Tax (CAT)?

Inheritance Tax, officially referred to as Capital Acquisitions Tax (CAT), is a levy imposed on assets inherited from deceased individuals. This tax applies to gifts and inheritances alike, making it essential for anyone involved in estate planning.

The rate of CAT can be significant, impacting the amount heirs receive. It’s crucial to understand how this tax works within the context of Irish law. The value of an inheritance determines if CAT becomes applicable.

Beneficiaries must report their inheritance and pay any due taxes before they can fully access the assets. There are specific thresholds that vary based on relationship proximity; closer relatives enjoy higher exemptions than distant ones.

Awareness of these factors is vital for effective financial planning and minimising potential liabilities related to Inheritance Tax in Ireland.

Who Has to Pay Inheritance Tax?

Inheritance tax is a concern for many, but who exactly has to pay it in Ireland?

Primarily, any individual receiving assets from a deceased person’s estate falls under the umbrella of this tax. This includes family members, friends, or even distant relatives. The relationship between the giver and receiver plays a crucial role in determining potential liabilities.

For instance, children and spouses benefit from higher thresholds compared to siblings or non-relatives. This means that closer connections often face lower tax burdens.

Additionally, those inheriting property or substantial monetary gifts should be aware of their obligations toward Capital Acquisitions Tax (CAT). Proper planning can help mitigate these costs effectively.

Understanding your status within these parameters is vital for effective inheritance tax planning in Ireland. Engaging with financial advisors can further clarify personal circumstances and responsibilities regarding inheritance taxes.

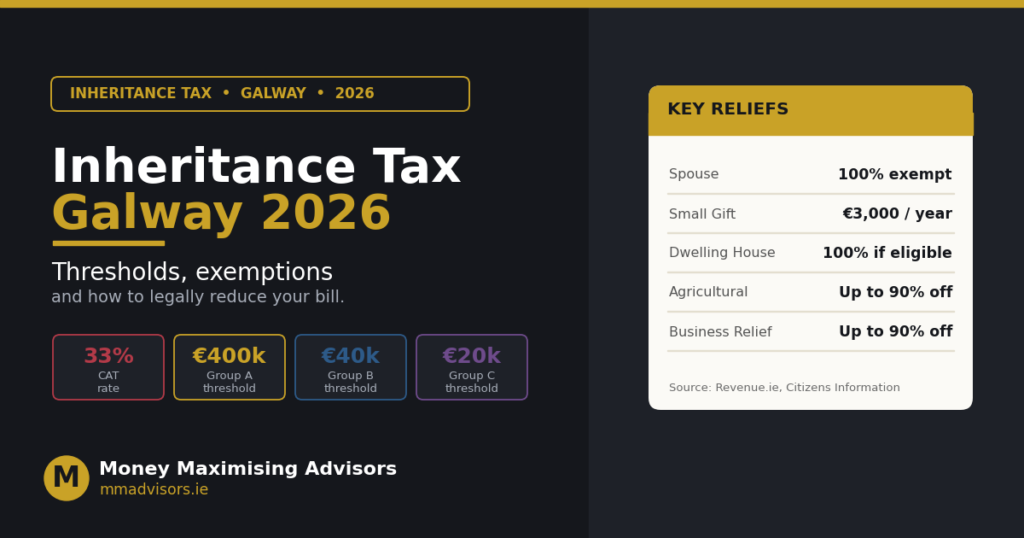

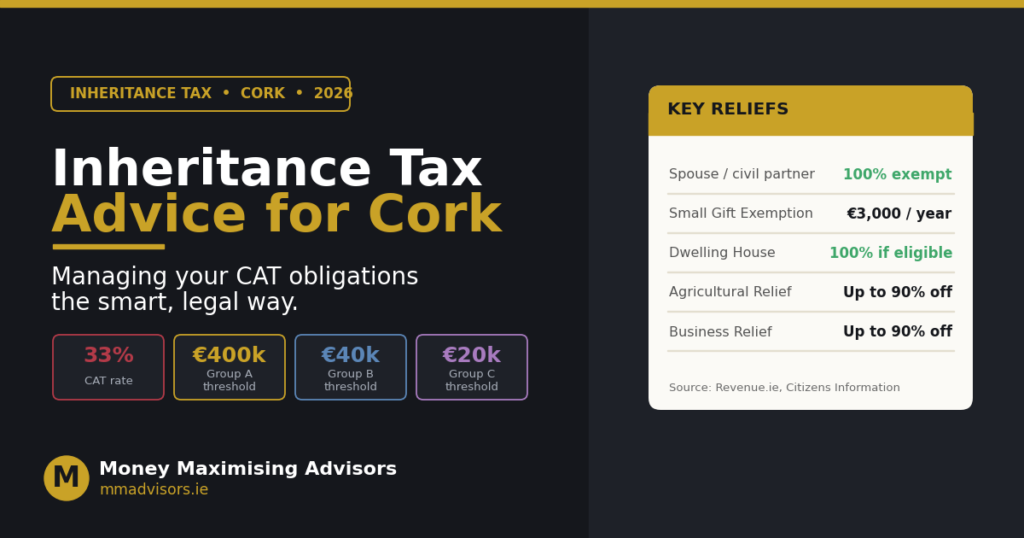

How Much is the Inheritance Tax Rate?

In Ireland, the inheritance tax rate is known as Capital Acquisitions Tax (CAT). It can feel daunting, but understanding it is crucial for effective planning.

The standard rate stands at 33%. This applies to any value received over a certain threshold. The thresholds depend on your relationship with the deceased.

For instance, if you inherit from a parent, the threshold is currently set at €335,000. If you’re receiving an inheritance from someone outside of that immediate circle—like a friend—the threshold drops significantly to just €16,250.

These distinctions highlight why knowing your specific situation matters when considering how much tax may be due after an inheritance. Keeping these rates in mind helps ensure you’re prepared for what lies ahead and allows for better financial strategies moving forward.

Maximise Your Inheritance, Minimise Your Taxes – Schedule Your Free Review with Money Maximising Advisors Now!

Ways to Legally Avoid Inheritance Tax

There are several strategies to legally minimise your inheritance tax liability in Ireland. One effective approach is gift-giving during your lifetime. Utilising the annual gift exemption allows you to transfer assets without incurring immediate tax implications.

Establishing trusts can also be beneficial. By placing assets into a trust, you may protect them from being included in the taxable estate upon death. This requires careful planning but can lead to significant savings.

Consider making use of available reliefs and exemptions as well. Various categories exist, such as agricultural or business reliefs, which can drastically reduce the amount subject to tax.

Regularly reviewing your financial situation with an expert ensures that you’re maximising all available options while remaining compliant with Irish law. Engaging a knowledgeable advisor will help tailor strategies specifically suited for you and your family’s needs.

Gift and Estate Planning Strategies

Effective gift and estate planning strategies can significantly reduce your inheritance tax liability in Ireland. By gifting assets during your lifetime, you can utilise the annual gift exemption. This allows you to transfer a certain amount each year without triggering taxation.

Consider making gifts to family members or loved ones while retaining control over the asset through life interest trusts. This method ensures that beneficiaries receive their inheritance while minimising taxable value.

Another strategic approach is to use joint ownership of property. When shared with a spouse or partner, this can create potential benefits under Irish inheritance tax rules.

Utilising insurance policies as part of an estate plan can also provide liquidity for heirs, allowing them to cover any potential taxes without needing to liquidate assets immediately. Each strategy serves a purpose and can be tailored based on individual circumstances and goals.

Trusts as a Tool for Reducing Inheritance Tax

Trusts can be an effective strategy for managing your assets and minimising inheritance tax in Ireland. By placing your property into a trust, you effectively transfer ownership while retaining control over how those assets are distributed.

- One of the main benefits is that trusts often fall outside the scope of inheritance tax. This allows your beneficiaries to inherit without incurring significant tax liabilities, preserving more wealth for them.

- Different types of trusts serve various purposes. For example, discretionary trusts allow trustees flexibility in distributing income and capital among beneficiaries based on their needs. This adaptability can optimise tax efficiency.

- Additionally, establishing a trust may offer protection against creditors or unforeseen circumstances. It ensures that your hard-earned wealth remains secured for future generations.

- Consulting with professionals who specialise in inheritance tax planning is crucial when considering this approach to ensure compliance with current laws and regulations.

FAQ’s About Inheritance Tax Ireland

Q. Are there any assets that are completely free from inheritance tax?

Yes. Certain gifts and inheritances may qualify for relief or exemptions under specific conditions. It’s important to check the rules to see if your assets qualify.

Q. How much can I inherit before I owe inheritance tax?

Ireland sets specific thresholds for inheritance tax, known as Group thresholds. Knowing these limits is crucial for effective planning, as amounts above the threshold may be subject to tax.

Q. Do tax rates differ based on my relationship to the deceased?

Yes. Inheritance tax rates can vary depending on whether you inherit from a parent, child, sibling, or distant relative. Closer relatives often benefit from higher thresholds and lower taxes.

Q. How can I minimise inheritance tax legally?

Professional estate planning strategies can help reduce your inheritance tax liabilities legally. Consulting with a qualified advisor ensures that your planning complies with regulations while optimising tax relief.

Q. Where can I get advice on Irish inheritance tax?

Financial advisors, solicitors, and tax professionals specialising in Irish inheritance law can provide guidance tailored to your circumstances.

Conclusion

Navigating the intricate world of inheritance tax in Ireland can seem daunting. However, with the right knowledge and strategic planning, you can significantly reduce your liabilities and ensure that more of your wealth is passed on to your loved ones. Understanding how inheritance tax works is crucial; it’s not just about knowing what you owe but also exploring avenues to minimise those costs through effective estate planning.

By utilising trusts, leveraging exemptions, and making informed gifts within thresholds, individuals can steer clear of hefty taxes. The nuances of Capital Acquisitions Tax (CAT) present opportunities for savvy planners to maximise their legacies while adhering to Irish law.

Protect Your Wealth Today – Consult Money Maximising Advisors and Legally Minimise Your Inheritance Tax!

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?