Inheriting an investment can feel like both a blessing and a challenge. Whether it’s a fixed term product, prize bonds, or cash in deposit accounts, the options stretch as wide as your financial goals. Understanding what to do with inherited funds is crucial for ensuring they work for you rather than sit idly by. If you find yourself pondering over inheritance saving plans in Ireland or exploring various inheritance investment options, you’re not alone. This journey could lead to significant opportunities if navigated wisely.

The right approach requires knowledge about your inherited assets and how each option aligns with your future plans. From managing savings thoughtfully to understanding the tax implications on inherited investments, every decision matters.

Let’s dig deeper into what it means to inherit an investment and uncover strategies that will help you make informed decisions moving forward.

Types of Inherited Investments

When it comes to inherited investments, several types may come into play. Understanding these options can help you make informed decisions.

- Stocks and shares are common forms of investment inheritance. They can offer growth over time but come with market risks.

- Real estate is another popular choice. Inheriting property provides potential rental income or future appreciation in value.

- Fixed term products might also be part of the mix. These often provide stable returns over a set period, making them a safer option for conservative investors.

- Prize bonds present an interesting alternative as well. While they don’t guarantee returns like traditional investments, they offer the thrill of potential winnings without risk to your principal amount.

Each type has its own unique characteristics and implications for your financial future. It’s essential to evaluate them carefully based on your goals and circumstances.

Fixed Term Products

Fixed term products offer a straightforward way to manage inherited funds. These investment options usually come with set terms, typically ranging from one month to several years.

One of the main appeals is their predictable returns. With fixed interest rates, you know exactly what you’ll earn over time. This can help in your inheritance financial planning Ireland by ensuring stability.

However, these products may limit access to your money during the term. If emergencies arise or new opportunities present themselves, those funds are tied up until maturity.

Choose wisely and consider how this fits into your overall strategy for managing inherited savings Ireland. Always assess whether this kind of investment aligns with your financial goals and risk appetite before diving in.

Prize Bonds

Prize bonds offer a unique way to invest inherited funds while holding the allure of potential rewards. When you purchase these bonds, you’re essentially entering a lottery system where your chances of winning cash prizes depend on the numbers drawn.

In Ireland, prize bonds can be particularly appealing for those looking for a low-risk investment option. They carry no risk of losing your initial capital and guarantee that you’ll receive your original investment back if you choose to redeem them.

Additionally, interest is paid in the form of prizes rather than traditional interest rates. This means that each bond gives you an equal chance to win significant sums at various intervals throughout the year.

This blend of safety and excitement makes prize bonds an interesting choice when considering inheritance financial planning in Ireland.

Deposit Accounts

Deposit accounts can be a straightforward option when inheriting funds. They provide safety and easy access to your money. Many people appreciate the peace of mind that comes with knowing their savings are secure.

Typically, these accounts offer modest interest rates. While they may not yield high returns, the stability they offer is appealing. You can withdraw cash as needed without worrying about market fluctuations.

In Ireland, banks often have various deposit account options tailored for different needs. Some might require a minimum balance while others allow regular deposits or withdrawals.

For those new to managing inherited savings in Ireland, this could be an excellent starting point. It’s essential to compare offerings from multiple institutions before deciding where to place your inheritance funds.

Pros and Cons of Inheriting an Investment

Inheriting an investment can bring both benefits and challenges. On the positive side, it may provide a significant financial boost. This could lead to opportunities for wealth growth or help with pressing expenses.

However, managing inherited investments isn’t always straightforward. You might find yourself burdened by complex decisions regarding asset allocation or emotional ties to specific investments.

Furthermore, there’s the potential for tax implications that could reduce your inheritance’s overall value. Understanding these intricacies is crucial.

Additionally, while some assets appreciate over time, others may not perform as expected. The need for ongoing management can also add stress if you’re unfamiliar with investment strategies.

Navigating this landscape requires careful consideration of various factors before making any decisions about how to handle your newfound assets effectively.

How to Manage an Inherited Investment

Managing an inherited investment can feel daunting, but taking a structured approach helps.

- Start by assessing the value of the asset. Understand what you’ve received—whether it’s stocks, bonds, or real estate. This knowledge will guide your next steps effectively.

- Consider your financial goals. What do you want from this inheritance? Short-term gains, long-term growth, or perhaps security? Aligning these objectives with your inherited assets is crucial for smart decisions.

- Research options available to you. You could liquidate some investments for cash flow or hold onto them to benefit from potential appreciation in value.

- Don’t forget about diversification. Spreading investments across different asset classes can help mitigate risk and enhance returns over time.

- Keep track of performance regularly and adjust your strategy as life changes occur or markets fluctuate. Staying informed puts you in control of managing inherited savings wisely.

Speak with our expert advisors to explore strategies that protect your wealth and boost returns. Schedule your free consultation now!

Tax Implications of Inherited Investments

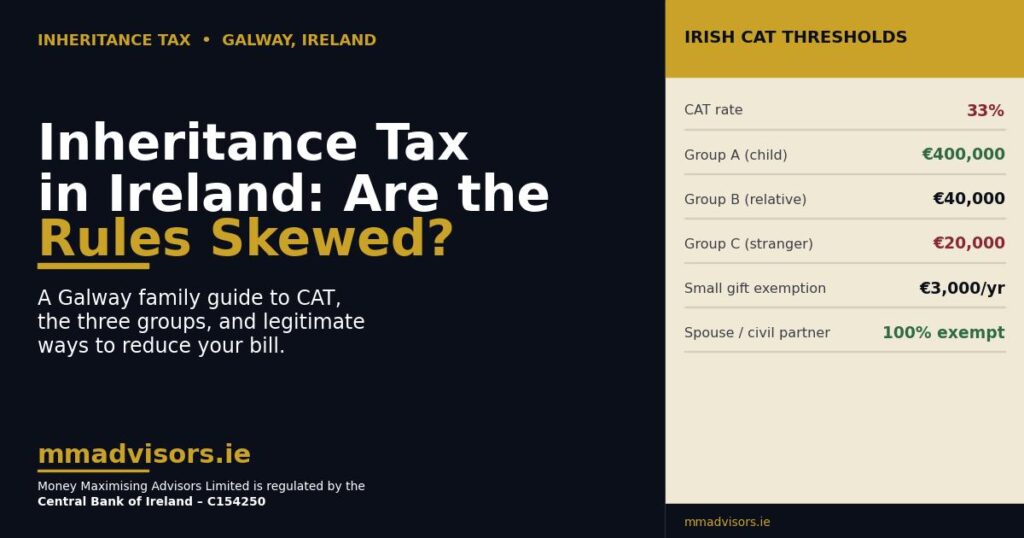

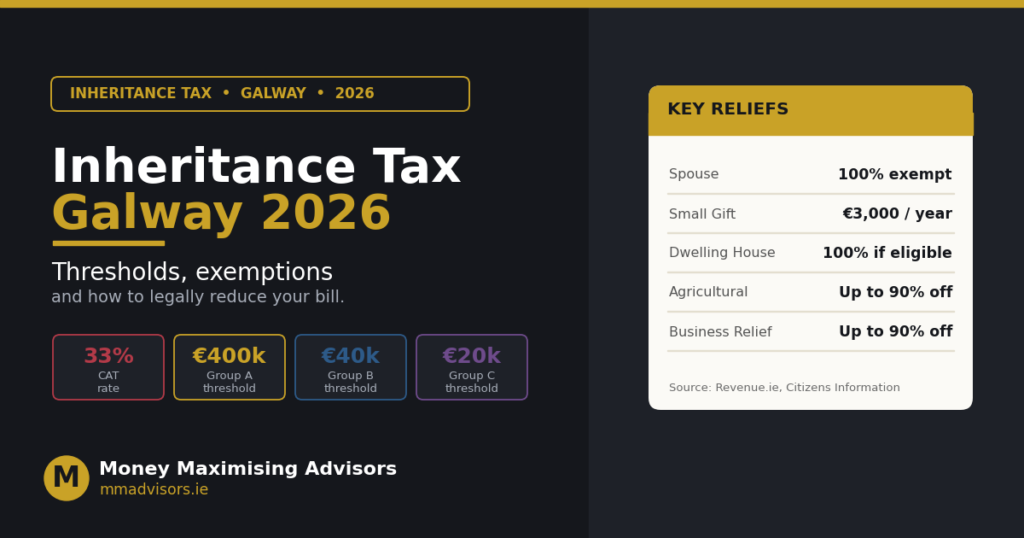

When dealing with inherited investments, understanding tax implications is crucial. In Ireland, the tax on inherited assets falls primarily under Capital Acquisitions Tax (CAT). This means you may owe taxes based on the value of the investment received.

There’s a threshold known as the Group Thresholds, which sets limits depending on your relationship to the deceased. Spouses and children benefit from more favourable thresholds than distant relatives or friends.

It’s essential to keep records of all documentation regarding the inheritance’s market value at the time it was transferred. Failing to accurately report can lead to penalties down the line.

Consider consulting a financial advisor knowledgeable about inheritance planning strategies in Ireland. They can provide tailored advice based on your circumstances and help navigate any complexities related to taxes and investments. Understanding these nuances ensures you’re better prepared for managing your newfound wealth effectively.

Seeking Professional Advice from Money Maximising Advisors

When you inherit an investment, navigating the complexities can be daunting. This is where professional guidance from Money Maximising Advisors becomes invaluable.

Our experts specialise in inheritance financial planning in Ireland. We help you understand your options and provide tailored advice that suits your unique situation. Our insights can illuminate paths you may not have considered on your own.

Investments vary significantly, and so do the associated risks and rewards. A Money Maximising Advisor will assess your inherited funds to ensure optimal management strategies are in place.

Moreover, we stay updated on tax implications related to inherited investments, helping you avoid pitfalls that could lead to unexpected liabilities. You gain peace of mind knowing a knowledgeable partner is guiding you through this important transition in your financial journey.

FAQ’S:

Q1. What tax obligations apply to inherited investments in Ireland?

When you inherit investments, tax obligations can vary depending on the type of asset. Capital acquisitions tax (CAT) may apply, and it’s important to understand thresholds, exemptions, and filing requirements to ensure compliance.

Q2. Should I keep, sell, or reinvest my inherited funds?

Deciding what to do with inherited investments depends on your financial goals, risk tolerance, and the type of assets you’ve received. Keeping, selling, or reinvesting each has its advantages, and careful consideration is key to maximising returns.

Q3. What investment options are available after inheritance?

Heirs in Ireland can choose from a variety of options, including fixed-term deposits, savings accounts, and prize bonds. Each option has distinct benefits regarding security, liquidity, and potential returns.

Q4. Do I need a financial advisor for inherited investments?

Yes. A professional financial advisor can guide you through complex decisions, minimise tax liabilities, and help you optimise your inheritance for long-term growth.

Q5. How can I plan to safeguard my financial future with inherited funds?

Effective planning involves understanding your options, setting clear financial goals, and using strategies that maximise your inheritance while protecting your wealth. Expert guidance can ensure your inheritance works for you in the long term.

Conclusion

Inheriting an investment can be both a blessing and a challenge. As you navigate through your options, it’s crucial to understand the types of inherited investments available in Ireland. From fixed-term products to deposit accounts and prize bonds, each comes with its unique pros and cons.

The importance of effectively managing inherited savings cannot be overstated. Familiarising yourself with inheritance financial planning strategies will empower you to make informed choices that align with your financial goals. Additionally, understanding the tax implications on inherited investments is vital, as it directly affects your overall returns.

Seeking professional advice from Money Maximising Advisors can provide valuable insights tailored specifically for you. Their expertise in inheritance investment advice in Ireland may help you identify the best inheritance savings plans suited to your needs.

Don’t leave your inherited investments to chance. Connect with Money Maximising Advisors to optimise your portfolio and minimise tax impact. Get started now!

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?