If you own investment property or you’re thinking about growing your portfolio, there’s genuinely exciting news for the Irish property market. A new buy-to-let mortgage Ireland lender has entered the scene — and it’s specifically targeting experienced landlords with lower, more competitive rates. Here at Money Maximising Advisors Limited, we’re helping landlords across Dublin, Galway, and nationwide take full advantage of this development.

For too long, the buy-to-let lending landscape in Ireland has lacked real competition. A handful of lenders dominated the market, leaving property investors with limited choices and often frustratingly high borrowing costs. That’s starting to change — and savvy landlords should be paying close attention.

What Is a Buy-to-Let Mortgage in Ireland?

A buy-to-let mortgage Ireland is a mortgage product specifically designed for properties you intend to let rather than live in. Unlike a standard home loan, a buy-to-let lender Ireland will assess your application primarily based on the expected rental income the property can generate, alongside your personal income and financial track record.

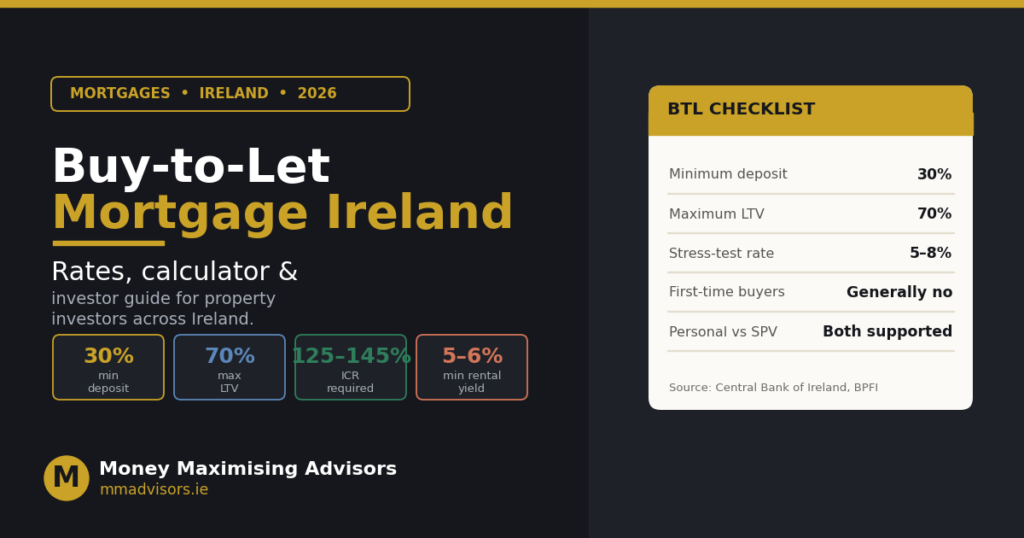

Investment property mortgage Ireland products also typically carry higher interest rates and require a larger deposit compared to residential mortgages — usually at least 30% of the purchase price. This reflects the greater risk lenders associate with investment lending.

Why a New Buy-to-Let Lender in Ireland Changes the Game

The arrival of a new player in the buy-to-let lender Ireland market is significant for several reasons. Most importantly, it introduces genuine competition — which historically drives rates down and improves product quality across the board.

What makes this particular lender stand out is its approach to experienced landlords. Rather than applying a one-size-fits-all rate structure, this lender rewards those with a proven track record. If you’ve been managing rental properties successfully for several years, you may now qualify for preferential buy-to-let mortgage rates Ireland that simply weren’t available before.

Key Features of the New Lender’s Offering:

- Lower buy-to-let mortgage rates Ireland for landlords with proven rental history

- Tailored criteria recognising the lower risk profile of experienced investors

- Potential for higher loan-to-value ratios for qualifying applicants

- A more streamlined application process for those with existing portfolio experience

If you’re comparing structures for your investment, our guide on Buy-to-Let Mortgage Rates vs SPV Mortgage Rates in Ireland: A Complete Comparison is a must-read.

Can Experienced Landlords Get Lower Mortgage Rates in Ireland?

Yes — and this is exactly why this development is so meaningful. Traditionally, a landlord mortgage Ireland product offered little to no incentive for experience. A seasoned investor with a well-managed portfolio of ten properties was often quoted the same rates as someone purchasing their first rental unit.

With this new buy-to-let lender Ireland, that’s no longer the case. Experienced landlords can now potentially access:

- Reduced interest rates compared to standard buy-to-let products

- Better terms based on your rental income history and portfolio performance

- More competitive overall borrowing costs, improving your net rental yield

Which Banks Offer Buy-to-Let Mortgages in Ireland?

Until recently, the market for landlord mortgage Ireland products was dominated by a small number of banks and specialist non-bank lenders. The limited competition made it difficult to negotiate and left many investors paying over the odds.

With a new buy-to-let lender Ireland now active, landlords have a wider pool of options. However, navigating the full market on your own can be time-consuming and complex. That’s where our team at Money Maximising Advisors Limited comes in — we compare the entire market on your behalf to find the best fit.

Exploring company structures for your portfolio? Read: Step-by-Step Guide: How to Get an Investment Property Mortgage in Ireland (Using an SPV).

What Deposit Do I Need for a Buy-to-Let Mortgage in Ireland?

The standard minimum deposit for an investment property mortgage Ireland product is 30% of the property’s value. This is considerably higher than the 10% typically required for first-time buyer residential mortgages, and it reflects the different risk profile of investment lending.

That said, the exact requirement can vary depending on:

- The lender and their specific criteria

- The type of property — house, apartment, or other residential investment

- Your financial profile, income, and existing portfolio

- The property location — Dublin, Galway, or elsewhere in Ireland

With new competition in the market, some lenders — particularly those targeting experienced investors — may offer more flexible deposit thresholds. Always verify the latest criteria with an adviser.

Are Buy-to-Let Mortgages More Expensive in Ireland?

Compared to residential home loans, buy-to-let mortgage rates Ireland have historically been higher. Lenders justify this by pointing to greater risk — rental income can be unpredictable, tenancies end, and maintenance costs can affect cash flow.

However, with increased competition now entering the market, rates are becoming more attractive — particularly for those landlords who can demonstrate a consistent, professional approach to property management. The key is to act promptly and work with an adviser who knows this market well.

Want to understand SPV structures? See: Buy-to-Let vs SPV Mortgage: What Every Irish Property Investor Should Know.

How Do Landlords Qualify for a Buy-to-Let Mortgage?

To qualify for a buy-to-let mortgage Ireland product, lenders will typically assess the following:

Rental Income Coverage

Lenders require that the expected monthly rent covers 125–145% of the monthly mortgage repayment. This stress-test protects against rate increases and rental voids.

Deposit

A minimum 30% deposit is standard, though this can vary.

Personal Income

Your existing income and financial commitments will be assessed alongside the rental income projections.

Property Valuation

An independent valuation is a standard part of the process.

Experience and Track Record

With this new buy-to-let lender Ireland, your experience as a landlord is now a genuine asset — potentially unlocking better rates and more favourable terms that weren’t previously available to you.

Learn more about SPV tax advantages: Ireland SPV Tax Benefits: What Every Real Estate Investor Should Know.

Ready to Explore Your Buy-to-Let Options?

Whether you’re purchasing your first investment property or looking to refinance an existing portfolio, our team is ready to help you access the most competitive buy-to-let mortgage Ireland products on the market.

Get in touch today — Contact Us to speak with an adviser, or Book an Appointment at your convenience.

Also read: Ireland’s Best SPV Mortgage Experts – Money Maximising Advisors.

Frequently Asked Questions

What is the best buy-to-let mortgage rate in Ireland?

The best buy-to-let mortgage rates Ireland currently available depend on your deposit, property type, and experience as a landlord. With a new lender in the market, rates are becoming more competitive. Speak to an adviser for the latest options.

Can experienced landlords get lower mortgage rates in Ireland?

Yes. The new buy-to-let lender Ireland has specifically designed products that reward landlords with a proven track record. Your experience can now directly translate to lower borrowing costs.

Which banks offer buy-to-let mortgages in Ireland?

Several banks and non-bank lenders offer landlord mortgage Ireland products. With a new entrant in the market, there are now more options than ever. A qualified mortgage adviser can compare all available products on your behalf.

What deposit do I need for a buy-to-let mortgage in Ireland?

The standard minimum deposit for an investment property mortgage Ireland is 30% of the property value. This can vary by lender — particularly for experienced investors who may qualify for more favourable terms.

Are buy-to-let mortgages more expensive in Ireland?

Historically, buy-to-let mortgage rates Ireland have been higher than residential rates due to the perceived risk of investment lending. However, with new competition entering the market, this gap is narrowing.

How do landlords qualify for a buy-to-let mortgage?

You’ll need to meet rental income cover thresholds, provide a minimum 30% deposit, pass income and financial assessments, and have the property independently valued. Experienced landlords may now access better terms with the right lender.

Conclusion

The entry of a new buy-to-let lender into the Irish market is excellent news for experienced landlords. With more competitive buy-to-let mortgage rates Ireland now available for those with a proven track record, there’s real opportunity to reduce borrowing costs and improve portfolio returns. At Money Maximising Advisors Limited, our team of expert mortgage advisers is here to help you navigate the full market and secure the best deal for your investment goals.

Disclaimer

This article provides general information about buy-to-let mortgage products in Ireland and should not be considered personalised financial or mortgage advice. Irish mortgage lending criteria and interest rates can change at any time, and individual circumstances vary widely. Always consult with a qualified financial adviser or mortgage broker before making significant property investment or borrowing decisions.