If you have money sitting in a bank account in Ireland right now, the chances are it is not working nearly hard enough for you. Ireland has a well-documented savings culture — with approximately €170 billion held in bank deposits across the country — but our investment culture has not kept pace. The result? Inflation quietly erodes the real value of what you have saved, while better returns remain just out of reach for most ordinary households.

That is changing. A new Irish Savings and Investment Account — a personal investment wrapper being developed by the Department of Finance — is on the way, with the government aiming to have it available from 2027. In the meantime, understanding your existing Savings & Investments options has never been more important.

At Money Maximising Advisors, we work with clients across Dublin, Galway, and beyond to help them make the most of their hard-earned money. In this guide, we walk you through everything you need to know about savings accounts Ireland, the upcoming SIA account, and the broader savings and investment Ireland landscape in 2026.

Why Irish Savers Are Being Left Behind

Here is an uncomfortable truth: most Irish savers are effectively losing money in real terms. With the average Annual Equivalent Rate (AER) on new household term deposits sitting at around 1.86%, and Deposit Interest Retention Tax (DIRT) charged at 33% on top of that, the after-tax return on a typical irish savings account is minimal. Inflation, even at modest levels, can easily wipe out whatever small return you receive.

The data tells the story clearly:

- €170 billion is held in Irish deposit accounts — much of it in zero or near-zero interest current accounts

- Irish households hold only 2.3% of their financial assets in direct investments, compared to an EU average of 7.5%

- Less than half of Irish adults hold any type of investment product

- One in five Irish adults saves more than €120 per month — yet most of that flows into low-yield deposits

The problem is not a lack of willingness to save. It is a lack of suitable, accessible, tax-efficient products that make investing feel safe and worthwhile for ordinary people. That is precisely what the new Irish Savings and Investment Account is designed to address.

What Is the New Irish Savings and Investment Account?

The Irish government is developing a new personal investment wrapper — referred to as a Savings and Investment Account (SIA) or Personal Investment Account (PIA) — which is expected to launch from 2027 as part of Budget 2027 proposals. Tánaiste and Minister for Finance Simon Harris has made this a stated priority for his tenure.

The new account is modelled on successful schemes from across Europe and beyond:

- Sweden’s ISK (Investeringssparkonto): A flat annual tax of around 1% on the total account value, with no CGT on gains and no requirement to track individual trades

- UK’s ISA: Up to £20,000 invested per year with returns entirely free from income tax and CGT

- Canada’s TFSA: Tax-free returns on up to C$7,000 invested annually

Ireland will not directly copy any single model, but is expected to incorporate the best elements of each. Key features expected of the Irish SIA include:

- A simple, low flat-rate annual tax on fund value — removing the need to track gains on every trade

- No capital gains tax on investment returns within the account

- Removal of the eight-year deemed disposal rule that currently penalises long-term investors

- Access through mainstream banks and investment providers

- Annual or lifetime contribution limits to focus benefits on middle-income earners

The legislative framework is expected in late 2026, with accounts available from 2027. Budget 2026 has already taken a first step — cutting exit tax on investment funds from 41% to 38% from January 2026.

Want to understand how these changes could affect your Savings & Investments strategy? Enquire Now and one of our Certified Financial Planners will be in touch.

Best Savings Accounts Ireland Right Now — What Are Your Options?

While the new SIA account takes shape, there are still strong options available through the existing range of savings accounts Ireland. Here is a practical overview of the main choices for Irish savers in 2026:

1. Fixed-Term Deposit Accounts

These offer a guaranteed rate of return over a fixed period — typically one to five years. They are safe and predictable, though returns after DIRT (33%) are modest. The best savings accounts Ireland for pure capital security tend to be fixed-term deposits with Credit Unions or banks offering competitive rates. Always compare the AER rather than the headline rate to understand your actual annual return.

2. State Savings (An Post / NTMA)

State Savings products are backed by the Irish government and offer DIRT-free, income-tax-free returns. They are one of the very few genuinely tax-free irish savings account options currently available. Fixed-term State Savings bonds and certificates offer defined returns over 3, 5, or 10 years. They are ideal for cautious savers who want complete capital security and a tax-free return.

3. Credit Union Savings

Credit unions are a trusted cornerstone of Irish savings culture. Dividend rates vary by credit union, but membership also provides access to low-cost loans and other financial services. Returns are subject to DIRT.

4. Online or Challenger Bank Accounts

A number of European challenger banks and online platforms now offer competitive interest rates on savings — often higher than traditional Irish banks. These are regulated within the EU and eligible for deposit protection up to €100,000 per institution. However, always check FSCS-equivalent protection before opening an account outside Ireland.

For a more detailed comparison of current rates and options, visit our in-depth guide on the best savings accounts ireland for 2025.

Not sure whether a savings account or an investment product is right for you right now? Book Now for a no-obligation conversation with one of our advisors.

Related Posts

Best Savings Account Ireland 2025 – Where to Get the Highest Rates

Looking for an Alternative Home for Your Savings Ireland?

4 Smart Ways to Start Saving for Your Child’s Education Today in Ireland

Best Savings Accounts in Ireland for Long-Term Financial Growth

Savings vs Investment Ireland — What Is the Difference and Which Is Right for You?

One of the most common questions we hear from clients is: “Should I save or invest?” The honest answer is — usually both, depending on your goals and timeline. Here is a straightforward comparison:

| Feature | Savings Account | Investment Product |

| Risk | Very low (FSCS protected up to €100k) | Low to high depending on product |

| Returns | Low (avg. AER ~1.86% on term deposits) | Potentially much higher (market-linked) |

| Tax on returns | DIRT at 33% on interest earned | Exit tax 38% or CGT 33% on gains |

| Access | Immediate or fixed term | Medium to long term (5+ years ideal) |

| Best for | Short-term goals, emergency fund | Long-term wealth building |

As a general rule of thumb, money you might need within the next one to two years belongs in a savings account. Money you are confident you can leave untouched for five years or more is a strong candidate for investment — where the potential for higher long-term returns more than compensates for the added risk.

Investment Options Ireland — Making Your Savings Work Harder

Alongside the new SIA coming in 2027, there is already a strong range of investment options ireland available through Money Maximising Advisors. These are designed to suit different risk appetites, time horizons, and financial goals:

- Regular Saver Investment Plans: Invest from as little as €100 per month into a diversified fund. Benefit from euro cost averaging and the power of compounding over time. Ideal for building wealth steadily alongside your monthly budget.

- Lump Sum Investments: If you have a significant sum in a low-yield deposit account, a lump sum investment can dramatically improve your potential long-term return. A typical deposit might earn 1.86% AER; a diversified equity fund has historically returned closer to 7–10% over the long term.

- Capital Protected Investments: For cautious investors who want market exposure without risking their original capital. These products offer participation in market growth while providing a floor that protects your principal.

- Corporate Investments: If you are a business owner in Dublin, Galway, or elsewhere in Ireland with retained profits sitting in a current account, a corporate investment plan can generate better returns in a tax-efficient structure.

- Pension Investments: Still the single most tax-efficient savings and investment ireland vehicle available. Contributions receive income tax relief at your marginal rate (up to 40%), and growth within the pension is entirely tax-free.

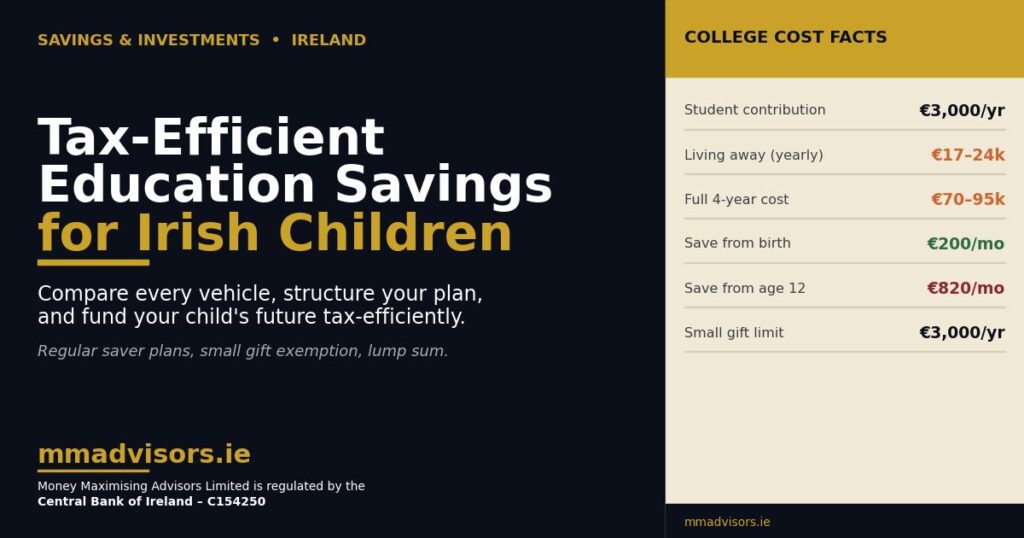

- College Education Savings Plans: With Irish third-level costs rising, dedicated education savings plans help families build a ring-fenced fund in a tax-efficient wrapper.

We Also Provide

| Service | What We Offer |

| Lump Sum Investments | Put a larger sum to work in a managed or market-linked fund |

| Regular Saver Investment Plans | Invest a fixed amount monthly — ideal for steady, long-term wealth building |

| Capital Protected Investments | Market-linked growth with protection of your original capital |

| Corporate Investments | Tax-efficient investment solutions for business owners with surplus cash |

| College Education Savings | Dedicated savings plans to fund your child’s third-level education costs |

| Execution Only Investing | Self-directed investing with professional support in the background |

| Pension Planning | The most tax-efficient investment vehicle available in Ireland |

| Inheritance Tax Planning | Section 72 and 73 policies to protect your estate |

| Life Insurance & Protection | Cover to protect your income and your family’s financial future |

What Is AER in Savings Accounts Ireland?

AER stands for Annual Equivalent Rate. It is the standardised way of expressing the interest rate you earn on a savings account over a full year, including the effect of compounding (where interest earns interest). The AER allows you to make like-for-like comparisons between different savings accounts ireland, regardless of whether interest is paid monthly, quarterly, or annually.

For example:

- An account paying 2% AER will turn €10,000 into €10,200 after one year (before DIRT)

- After DIRT at 33%, your net return would be approximately €134 — leaving you with €10,134

- Compare this to a well-managed investment fund returning 7% annually: the same €10,000 could become €19,672 over 10 years (before exit tax)

The difference in long-term outcomes between a savings account and an investment product can be dramatic. Understanding AER is the first step to making that comparison meaningfully.

Frequently Asked Questions (FAQs)

1. What is the best savings account in Ireland right now?

The best savings accounts ireland right now include State Savings products from An Post (DIRT-free), competitive fixed-term deposits from Credit Unions and banks, and EU-regulated online savings platforms offering higher AER rates. The “best” option depends on your timeline, need for access, and whether you prioritise security or returns. A qualified financial advisor can help you compare the full range of options.

2. Which bank gives the highest interest in Ireland?

Interest rates on savings accounts change regularly, and the highest rate available will depend on the term length and whether you are comparing current accounts, instant access accounts, or fixed-term deposits. As of 2026, some Credit Unions and online European banks are offering more competitive rates than traditional high-street banks. Always compare the AER (Annual Equivalent Rate) rather than the headline rate, and remember that DIRT at 33% applies to interest earned.

3. Are savings accounts safe in Ireland?

Yes — deposits in Irish-regulated banks and credit unions are protected up to €100,000 per institution under the Deposit Guarantee Scheme (DGS), which is backed by the Central Bank of Ireland. State Savings products held via An Post carry the full backing of the Irish government and are considered among the safest irish savings account options available anywhere.

4. How much interest can I earn on savings in Ireland?

The amount of interest you can earn depends on the type of account and the rate offered. As of 2026, the average AER on new household term deposits in Ireland is around 1.86%. However, some fixed-term deposits and State Savings products offer higher rates. Remember that DIRT at 33% is deducted from interest earned on most accounts, reducing your effective after-tax return considerably.

5. What is AER in savings accounts Ireland?

AER (Annual Equivalent Rate) is the standardised interest rate that shows how much you will earn on a savings account over one full year, factoring in compounding. It is the most accurate way to compare savings accounts ireland because it accounts for how often interest is paid and reinvested. When comparing accounts, always look at the AER rather than the headline rate to understand your true annual return.

6. When will the new Irish Savings and Investment Account be available?

The Irish government aims to legislate for the new Savings and Investment Account (SIA) framework in 2026, with accounts expected to be available from 2027. The scheme is being developed as part of a broader “Roadmap for Retail Investment” and is expected to feature a simplified tax structure, no capital gains tax on gains within the account, and accessible entry for everyday Irish savers and investors.

Conclusion

Ireland’s Savings & Investments landscape is changing — and changing fast. The arrival of a new Savings and Investment Account in 2027, combined with the reduction in exit tax already introduced in Budget 2026, represents a genuine opportunity for Irish households to finally make their money work harder. Whether you are looking for the best savings accounts ireland today or positioning yourself for the new investment options coming tomorrow, now is the time to review your financial strategy.

At Money Maximising Advisors, our team of Certified Financial Planners (CFP) and Qualified Financial Advisors (QFA) helps clients across Dublin, Galway, and all of Ireland navigate their savings and investment ireland choices with confidence. From regular saver plans and lump sum investments to pension planning and the upcoming new account — we are here to help you take the right next step.

Ready to put your savings to work? Contact Us today to speak with a specialist, or Book an Appointment at a time that suits you. Your financial future deserves more than a 1.86% AER.

Disclaimer

This article provides general information about savings accounts and investment options in Ireland and should not be considered personalised financial or investment advice. Interest rates, tax rates, and product details are subject to change. The new Savings and Investment Account described in this article has not yet been legislated and final details may differ from those outlined here. Investment returns are not guaranteed and the value of investments can fall as well as rise. Always consult with a qualified financial advisor or tax professional before making significant financial decisions. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland.