The Irish property market has undergone significant transformation over the past few years, leaving many prospective investors wondering whether buy-to-let Ireland opportunities remain worthwhile in 2026. With shifting regulations, fluctuating mortgage rates, and evolving tenant protections, the landscape for property investment Ireland has become increasingly complex. At Money Maximising Advisors Limited, we understand the challenges Irish investors face when navigating the current real estate market. Whether you’re based in Dublin, Galway, or elsewhere across Ireland, understanding the viability of buy-to-let Ireland investments is crucial before committing your capital. This comprehensive guide examines the current state of residential buy-to-let Ireland, analyses rental yield trends Ireland, and helps you determine whether property investment remains a sound financial strategy in 2026.

The Current Irish Real Estate Market Outlook

The Irish real estate market outlook for 2026 presents a mixed picture for property investors. Whilst demand for rental accommodation continues to outstrip supply—particularly in urban centres like Dublin and Galway—investors face mounting pressures from regulatory changes and taxation policies.

Recent data indicates that property prices have stabilised somewhat compared to the rapid increases seen in previous years. However, the cost of buying rental property remains substantial, with entry barriers particularly high in Dublin’s competitive market. For those considering property investment Ireland opportunities, understanding these market dynamics is essential.

The residential buy-to-let Ireland sector continues to experience a supply shortage, with many landlords exiting the market due to increasing compliance costs and tax burdens. Paradoxically, this creates opportunities for well-informed investors who can navigate the regulatory environment effectively.

Understanding Rental Yield Trends Ireland

Rental yield trends Ireland vary significantly depending on location, property type, and market conditions. Dublin, whilst commanding the highest rental prices, often delivers lower percentage yields due to elevated property purchase costs. Conversely, regional cities and towns may offer more attractive investment property returns Ireland despite lower absolute rental income.

Current average rental yields across Ireland range from approximately 4% to 7%, with variations based on:

- Property location: City centre versus suburban areas

- Property type: Apartments versus houses

- Market segment: Student accommodation, professional tenants, or family homes

- Property condition: Turnkey versus renovation projects

Investors should conduct thorough due diligence on local rental markets before committing to any buy-to-let Ireland investment. Understanding vacancy rates, tenant demographics, and local employment trends provides crucial context for projected returns.

Related Reading

For more detailed information on financing your investment, explore our guide on Buy-to-let Mortgages Ireland: How Much Can You Borrow for a Buy-to-Let?

Mortgage Rates and Financing Challenges

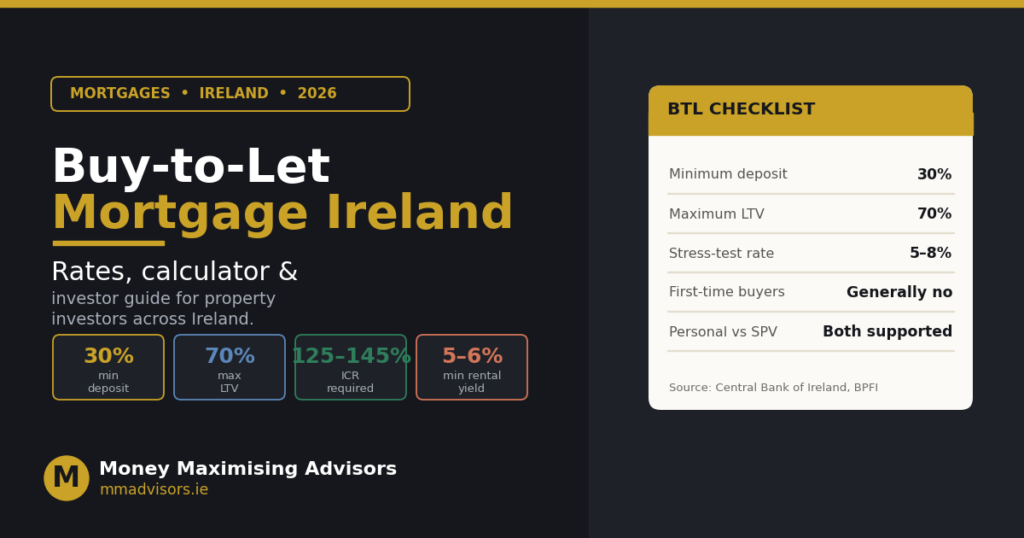

Irish mortgage rates have fluctuated considerably, directly impacting the viability of buy-to-let investments. Lenders typically require larger deposits for investment properties—often 30% or more—and charge higher interest rates compared to owner-occupier mortgages.

Current challenges facing property investors include:

- Stricter lending criteria: Banks scrutinise rental income projections more carefully

- Stress testing requirements: Investors must demonstrate ability to service loans even if rental income drops

- Limited product availability: Fewer lenders offer competitive buy-to-let products

Despite these hurdles, securing appropriate financing remains achievable with proper preparation and professional guidance. Understanding the full scope of Buy-to-Let Mortgage Costs in Ireland: Full Breakdown for 2025 helps investors budget accurately.

Ready to explore your financing options? Enquire now to speak with our mortgage specialists.

Tax Implications Buy-to-Let Ireland: What’s Changed?

The tax implications buy-to-let Ireland investors face represent one of the most significant challenges in 2026. Landlord tax Ireland regulations have become increasingly onerous, with several key considerations:

Income Tax: Rental income is taxed at your marginal rate (up to 40%), plus PRSI and USC, potentially resulting in a combined rate exceeding 50% on rental profits.

Mortgage Interest Relief: Unlike previous years, mortgage interest is no longer fully deductible against rental income in the year incurred. Instead, it’s treated as a credit against tax liability, significantly reducing its benefit.

Local Property Tax (LPT): Annual property tax based on property valuation, though generally modest compared to other costs.

Capital Gains Tax (CGT): Upon sale, investors face 33% CGT on profits, though certain reliefs may apply depending on circumstances.

Stamp Duty: Higher rates apply for non-primary residences, adding to acquisition costs.

These tax implications substantially impact net returns, making professional tax planning essential. Many investors now explore structures like SPV (Special Purpose Vehicle) companies to optimise their tax position. Learn more in our article: Everything You Need to Know About Using a SPV Company for Buy-To-Let Property

Regulatory Landscape for Irish Landlords

Beyond taxation, landlords face extensive regulatory requirements that impact property investment Ireland viability:

RTB Registration: All tenancies must be registered with the Residential Tenancies Board within one month of commencement.

Rent Pressure Zones (RPZ): In designated areas, annual rent increases are capped at 2%, limiting income growth potential.

Minimum Standards Regulations: Properties must meet specific energy efficiency and safety standards, potentially requiring substantial retrofitting investments.

Tenant Protections: Enhanced security of tenure and notice periods protect tenants but reduce landlord flexibility.

Planning Permission: Some local authorities impose restrictions on short-term letting, limiting Airbnb-style opportunities.

These regulations, whilst protecting tenants, add complexity and costs that investors must factor into their calculations. Understanding What is a Buy-To-Let Mortgage? What Do You Need to Be Eligible? provides essential foundational knowledge.

To discuss how these regulations affect your specific investment plans, book now for a personalised consultation.

Property Price Forecast Ireland: What Lies Ahead?

The property price forecast Ireland for 2026 and beyond suggests continued moderate growth, though regional variations persist. Economic factors influencing projections include:

- Employment trends: Strong job markets in technology and pharmaceutical sectors support Dublin and Cork

- Population growth: Immigration and natural increase sustain housing demand

- Supply constraints: Planning delays and construction costs limit new housing delivery

- Interest rate environment: European Central Bank policies affect mortgage affordability

- Government interventions: Help-to-Buy schemes and housing targets influence market dynamics

Whilst predicting exact price movements remains impossible, most analysts expect continued upward pressure on prices, albeit at more modest rates than seen during previous boom periods.

For regional investors, cities like Galway, Cork, and Limerick present interesting opportunities with potentially better yields than Dublin. Explore competitive rates in our guide: Buy-to-Let Mortgages in Ireland: Find our Best Rates

Strategic Considerations for 2026 Investors

Successfully navigating property investment Ireland in 2026 requires strategic thinking beyond simple buy-and-hold approaches:

Location Selection: Focus on areas with strong employment prospects, good transport links, and undersupplied rental markets.

Property Type: Consider demand drivers—student accommodation near universities, family homes in commuter towns, or apartments near employment hubs.

Value-Add Opportunities: Properties requiring modernisation or conversion may offer superior returns despite higher initial investment.

Portfolio Diversification: Spreading investments across multiple properties or locations reduces concentration risk.

Professional Structure: Evaluate whether personal ownership, partnership, or SPV company structure optimises your tax position.

Long-Term Perspective: Property investment typically requires 5-10 year horizons to achieve meaningful returns after costs and taxation.

Is Buy-to-Let Ireland Still Worth It?

The central question remains: is buy-to-let Ireland still viable in 2026? The answer depends entirely on individual circumstances, investment goals, and risk tolerance.

Arguments in Favour:

- Persistent housing shortage maintains rental demand

- Tangible asset providing inflation protection

- Potential for capital appreciation alongside rental income

- Diversification from traditional pension and stock investments

- Opportunity to leverage capital through mortgage financing

Arguments Against:

- High landlord tax Ireland burden significantly reduces net returns

- Regulatory complexity and compliance costs continue increasing

- Substantial capital requirements create high barriers to entry

- Property management demands time and expertise

- Market liquidity constraints—selling property takes time

For experienced investors with sufficient capital, professional support, and realistic expectations, buy-to-let remains viable. However, it’s no longer the straightforward wealth-building opportunity it once represented.

Conclusion

The property investment Ireland landscape in 2026 presents both challenges and opportunities for prospective landlords. Whilst the tax implications buy-to-let Ireland investors face have increased substantially, persistent housing shortages ensure continued rental demand across Dublin, Galway, and beyond.

Success in buy-to-let Ireland now requires sophisticated planning, thorough market research, and professional guidance to navigate complex regulations and optimise tax positions. At Money Maximising Advisors Limited, our team of Certified Financial Planners and Qualified Financial Advisors provides expert guidance on property investment, mortgage financing, and tax planning tailored to your specific circumstances.

Whether you’re a first-time investor or expanding an existing portfolio, professional advice ensures you make informed decisions aligned with your financial goals. Don’t navigate the complexities of Irish property investment alone.

Contact Us today to discuss your property investment plans, or Book an Appointment with one of our experienced advisors to receive personalised guidance on maximising your investment returns whilst minimising tax liabilities.

Read More:- How Much Money Can You Gift to a Family Member Tax-Free in Ireland?

Frequently Asked Questions

- Is buy-to-let property still profitable in Ireland?

Buy-to-let can still be profitable in Ireland, but returns have diminished due to higher taxes and regulatory costs. Success depends on securing properties with strong rental yields, managing costs effectively, and implementing proper tax planning strategies. Professional advice is essential to determine viability for your specific situation.

2. How have Irish mortgage rates affected buy-to-let viability?

Higher Irish mortgage rates have significantly impacted buy-to-let viability by increasing financing costs and reducing net rental yields. Combined with stricter lending criteria and larger deposit requirements, current rates make achieving positive cash flow more challenging, particularly for highly leveraged investments.

3. What is the average rental yield in Dublin vs other Irish cities?

Dublin typically offers rental yields of 4-5% due to high property prices, whilst regional cities like Galway, Cork, and Limerick may deliver 5-7% yields. However, Dublin benefits from stronger tenant demand, lower vacancy rates, and potentially greater capital appreciation, making total returns more comparable.

4. Are landlords facing new tax changes in Ireland 2026?

Whilst no major new tax changes were introduced specifically for 2026, landlords continue facing the challenging tax environment implemented in recent years, including restricted mortgage interest relief, income tax at marginal rates plus PRSI/USC, and 33% capital gains tax. Staying informed about potential future changes remains crucial.

5. What regulations impact Irish buy-to-let landlords?

Irish landlords must comply with RTB registration, Rent Pressure Zone caps, minimum property standards, enhanced tenant protections, and local authority planning requirements. Non-compliance can result in significant penalties, making professional property management increasingly valuable for ensuring regulatory adherence.

We Also Provide:

Whether you need guidance on pensions, mortgages, or estate planning, we’re here to help:

- Pension Enquiries | Book Pension Consultation

- Mortgage Enquiries | Book Mortgage Consultation

- Protection Enquiries | Book Protection Consultation

- Inheritance Tax Enquiries | Book Inheritance Tax Consultation

- Public Sector Enquiries | Book Public Sector Consultation

- Savings & Investments Enquiries | Book Savings Consultation

- Superannuation Calculations | Book Superannuation Consultation

Disclaimer: This article provides general information and should not be considered personalised financial or tax advice. Irish tax laws and property regulations change periodically, and individual circumstances vary significantly. The information presented reflects the situation as of early 2026 but may be subject to change. Always consult with qualified financial advisors, tax professionals, or legal experts before making significant property investment decisions. Money Maximising Advisors Limited recommends comprehensive professional assessment of your specific financial situation, investment goals, and risk tolerance before proceeding with any buy-to-let investment.