This blog explores innovative ways Irish homeowners can use equity release mortgages, from funding home improvements and education to managing debt, aiding family, and investing in property. Through real-life stories, it demonstrates how releasing equity can unlock financial freedom, offering practical solutions for those seeking to maximise their home’s value without selling or downsizing.

Equity Release Mortgages Explained

An equity release mortgage allows homeowners to unlock the value built up in their property. By borrowing against home equity, individuals can access funds while continuing to live in their homes. This option is ideal for those who want financial flexibility without selling or downsizing.

The concept is straightforward: you release cash tied up in your home, usually through a loan secured against it. The value available depends on factors like property worth and remaining mortgage balance.

Many find this appealing—whether for home improvements, debt consolidation, or funding retirements. Regulations ensure safety and clarity in this process. Working with reputable equity release mortgage lenders ireland helps ensure transparency and support throughout the journey of accessing the equity locked within your property.

Benefits of Equity Release Mortgages

- Financial Flexibility: With an equity release mortgage, you can access the wealth tied up in your home. This opens doors to various possibilities, whether it’s funding a passion project or managing unexpected expenses.

- No Monthly Repayments: Many plans offer this feature. It reduces financial stress and allows you to focus on what truly matters—your lifestyle and well-being.

- Tax-Free Cash: The money you receive is tax-free. This makes it easier to use the funds as needed without worrying about additional costs.

- Stay in Your Home: You don’t have to move out. Enjoy the comfort of familiar surroundings while benefiting from the value of your property.

Equity release gives many people peace of mind. Knowing they have options for their finances can be incredibly empowering as they navigate retirement or plan for future needs.

What Can You Use the Funds For?

There are many approved reasons to release equity from your home.

Imagine transforming your living space. Home improvements can elevate both comfort and value. Whether it’s a new kitchen or an extension, the funds offer endless possibilities for enhancement.

Consider medical expenses or education fees. Life’s costs add up, but now you have options to address these needs without dipping into savings.

Perhaps you’re thinking of helping a loved one with a deposit for their own home. This could turn dreams into reality for family members looking to step onto the property ladder.

Equity release isn’t just about luxury; it extends to practical applications too—like managing inheritance tax liabilities after a significant event or covering separation-related costs during tough times.

It’s also ideal for those wanting to buy another property as a second home or holiday retreat elsewhere, offering flexibility that adapts to evolving lifestyles and aspirations.

Some homeowners use this pathway to buy out their ex-partner’s share of the house during a divorce or separation, ensuring stability and continuity amidst personal transitions.

You might also like our post on Top Up Mortgage & Equity Release In Ireland – 2025 Guide.

Others might see it as an opportunity to consolidate short-term loans into one manageable payment, reducing monthly repayments significantly while simplifying their financial landscape.

Using equity release creatively ensures your hard-earned equity works for you at every stage of life. This strategy not only supports your goals but can also provide peace of mind as you navigate life’s transitions.

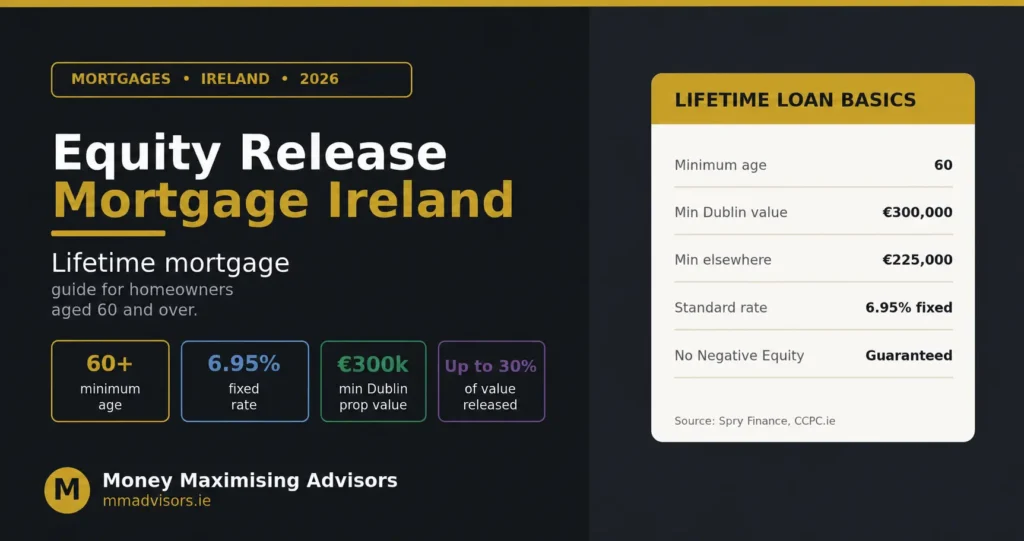

Key Criteria to Qualify for Equity Release

Understanding the key criteria for equity release mortgages is crucial.

Generally, you must be at least 55 years old. Age matters because lenders want assurance that the funds will serve long-term needs.

Your home’s value plays a significant role. Most providers have minimum property values, often around €115,000. They typically reject properties in poor condition or unusual constructions.

Location can influence eligibility too. Properties in remote areas might not qualify due to potential resale challenges.

Your residency status may impact your application as well. Most lenders require applicants to live in their primary residence on a permanent basis.

Lenders also assess any outstanding mortgage debt—this affects how much equity you can release. You must usually clear existing mortgages before proceeding with new loans based on your home’s value.

Related read: Equity Release In Ireland: What You Need To Know.

These criteria aim to ensure both safety and satisfaction for borrowers exploring this financial option within Ireland’s ever-evolving housing market.

How Much Equity Can You Access?

Knowing how much equity you can access is crucial when considering an equity release mortgage.

Ready to take the next step? Book a consultation with one of our experts to discuss your eligibility. The amount depends on several factors. Primarily, the value of your property and any outstanding mortgage balance play significant roles. Lenders typically use a loan-to-value ratio to determine eligibility. Curious about how much equity you can access? Enquire now to learn more about your financial options. Age also matters. The older you are, the more likely you’ll qualify for a higher percentage of your home’s value. Most lenders allow up to 60% of the property’s current market value. However, some may offer slightly more or less based on individual circumstances.

Using an equity release loan calculator can provide estimates tailored to your situation. This tool simplifies the decision-making process by giving real-time figures based on your specific details—helping you navigate options confidently.

Interest Rates and Fees Associated with Equity Release Mortgages

Understanding interest rates is crucial when considering equity release mortgages in Ireland. Typically, these rates fluctuate based on market trends and lender policies.

The interest rate on equity release usually falls between 3% and 6%. This range can vary, depending on the provider and the type of product you choose. A fixed-rate mortgage may offer stability over time.

Recommended: Senior’S Equity Release: Lifetime Loans In Dublin.

Fees are another consideration. Expect costs such as arrangement fees, valuation fees, and legal expenses. Some lenders might include early repayment charges as well.

It’s essential to shop around for the best options available. Comparing offers from different lenders can help you find favourable terms that suit your needs while keeping overall costs manageable.

Always read through any documentation carefully before committing to ensure there are no hidden surprises down the line.

Financial Requirements to Qualify for Equity Release Mortgages

Principal Private Residence

To qualify for equity release on your principal private residence, you must meet certain financial requirements.

- Income: Lenders will assess your income to ensure you can afford the repayments. This may include pension, employment income, or rental income from other properties.

- Affordability: You’ll need to demonstrate that you can afford the increased mortgage amount. The lender may perform a thorough affordability check, considering your current expenses and potential changes in circumstances.

- Repayment Ability: You must show your ability to repay the mortgage, which may include demonstrating a stable income or savings.

- Minimum Disposable Income: Similar to standard mortgages, you may need to show a minimum disposable income to prove affordability.

Residential Investment Properties

For residential investment properties, the requirements focus more on rental income than personal income.

- Rental Income: The potential market rent for the property must be equal to or greater than 1.2 × the mortgage repayments. This ensures that you can cover the loan with rental income.

- Multiple Properties: If you own more than two residential investment properties, the lender may lower the rental income requirement to 0.85 × the mortgage repayments.

Real-Life Scenarios

How One Couple Unlocked €75,000 from Their Home — Without Touching Their Savings

John and Mary, both teachers in their early 50s, have a combined income of €100,000. They own a home valued at €350,000 and have an existing mortgage balance of €200,000. With the rising interest rates and financial pressures of their twins entering college, they wanted to find a way to manage their cash flow and tap into their home’s appreciation without dipping into their savings.

They decided to explore equity release mortgages. After researching their options and consulting with a broker, they discovered that they could remortgage their home, releasing equity tied up in their property. By doing this, they could access a lump sum to cover upcoming expenses, such as college fees and home renovations, while still enjoying the comfort of their own home.

Here’s how they did it: With a loan-to-value ratio of 80%, John and Mary remortgaged for €225,000, clearing their existing mortgage and freeing up €75,000 in cash. They opted for a fixed-rate equity release mortgage, locking in a competitive interest rate and predictable monthly payments over a term of 20 years.

You might also like our post on How To Remortgage To Release Equity From Your Property.

This strategic move allowed them to unlock their home’s wealth without the need for additional borrowing or sacrificing their lifestyle. With the additional funds, they were able to cover their children’s education, embark on home improvements, and even consider the possibility of investing in a second property. This unlocked door to financial flexibility without any added stress on their finances, giving them peace of mind for the future.

Turning Equity Into Opportunity: A Smart Divorce Settlement Solution

Tommy and Jane had been married for several years, but their relationship had reached a breaking point. With their family home valued at €400,000 and an outstanding mortgage of €100,000, they were facing a daunting situation. Jane, who is a teacher, wanted to stay in the home with their 3 children, but needed to find a way to buy out Tommy’s ownership.

With the help of their real estate broker, Jane explored the possibility of releasing equity from their home to fund her settlement offer. After consulting with a mortgage expert, she discovered that she could release up to €100,000 in equity, allowing her to pay off Tommy’s share while maintaining her own financial stability.

This innovative solution not only resolved the immediate financial challenge but also empowered Jane to take control of her future. By leveraging their home’s value through an equity release mortgage, she was able to navigate through this emotional transition with confidence and clarity. The process involved remortgaging the property for €250,000, with a portion of the funds used to clear the existing mortgage and the remainder used to buy out Tommy’s share. This enabled Jane to preserve the family home for herself and her children, while also providing her with a sense of stability and financial security during a time of significant change.

Remortgage & Consolidate Loans to Reduce Monthly Repayments

James and Elaine, both civil servants in their early 50s, were feeling the financial pinch. With three dependent children and rising expenses, their monthly income was stretched thin. The couple had long made sacrifices for their family, but now they faced mounting stress from juggling multiple loan repayments.

Unlocking the value in your home starts with a conversation. Schedule your free consultation today and start planning your future.

Their home, valued at €350,000, had an outstanding mortgage of €150,000 with monthly repayments totaling €1,500. Additionally, they carried a home improvement loan of €50,000 and a personal loan of €25,000, each with monthly payments of €500 and €250 respectively. The thought of consolidating these debts seemed daunting, but the idea of financial relief was appealing.

Want to explore your options for releasing equity in your home? Reach out today for tailored advice.

After consulting with a broker, James and Elaine discovered the power of equity release. By remortgaging their home and consolidating all their loans into one package, they could significantly reduce their monthly outgoings. The potential to free up more cash each month became an enticing possibility, offering the chance to regain control over their finances and provide a better future for their family.

The result? Their total monthly repayments dropped to €1,850, freeing up €450 in cash flow each month. This newfound financial freedom allowed them to focus on their children’s college expenses, with plans to revisit their mortgage strategy once their children graduate and their finances improve.

Related read: Buy To Let Mortgage Rates Vs Spv Mortgage Rates In Ireland: A Complete Comparison.

Remortgage for a House Extension to Generate Income

Sean and Michelle, both working parents in their late 40s, found themselves constantly fielding requests from students looking for accommodation near their home. Living in a spacious house beside a university, they saw an opportunity to generate additional income.

The couple owned their home outright, which was valued at €440,000, with a remaining mortgage balance of €170,000. The idea of building an extension at the back of the house to create separate living quarters for students seemed enticing. They knew it would require significant funds—a financial hurdle that initially seemed daunting.

Seeking advice from a broker, Sean and Michelle discovered the potential benefits of remortgaging their property. By releasing equity from their home’s value, they could fund the construction without dipping into savings or taking out high-interest loans.

With careful planning and budgeting, Sean and Michelle embarked on their home extension project. The £50,000 increase in mortgage repayments, spread over the course of several years, allowed them to earn a net income of £11,000 annually, making the investment worthwhile.

Releasing Equity to Buy a Second Property

John, a homeowner in his late 50s with a successful career, found himself yearning for a second property. He had been dreaming of owning a holiday home where he could escape the hustle and bustle of city life. The idea seemed daunting at first, but then he discovered the potential of equity release.

With his current home value at €400,000 and an outstanding mortgage balance of €100,000, John realized he had significant untapped resources. He consulted with his financial advisor to explore options that would allow him to access this wealth without selling his primary residence.

After careful consideration, John opted for an equity release mortgage. This move enabled him to unlock €75,000 from his home’s equity — enough to serve as a deposit on his dream holiday property. The process was surprisingly straightforward, giving John the flexibility he needed while keeping future loans manageable through smart planning and research.

Here’s How an Investor Turned Equity Into Expansion

Pat, a savvy property investor, saw a golden opportunity to expand her portfolio. She owned three buy-to-let properties that had appreciated significantly over the years. These assets provided solid rental income, but she wanted more.

Recommended: Get A Mortgage When Selling Your Home And Buying Another.

Pat set her sights on developing a student apartment block in an up-and-coming neighbourhood. The potential for high returns was enticing. However, securing the necessary funds posed a challenge.

With little hesitation, Pat contacted her financial advisor. Together they explored options for freeing up capital through equity release from her existing properties. Pat successfully unlocked sufficient funds to cover the deposit required for development finance.

This strategic move allowed Pat not only to diversify her investments but also to maintain ownership of her original assets while entering new markets seamlessly.

Frequently Asked Questions (FAQ)

- What is an equity release mortgage?

An equity release mortgage allows you to unlock the value built up in your home without selling or moving. You can access funds for renovations, education, debt consolidation, or to help a loved one with a deposit, while still owning your home. - Are equity release mortgages safe?

Yes, when managed properly through regulated lenders. Brokers assess your eligibility and repayment ability and only recommend equity release if it supports your long-term financial stability. - Is it better to remortgage or release equity?

It depends. Remortgaging can secure a better rate, while equity release provides cash for immediate needs. Often, you can do both. - Can I use home equity to clear debts?

Yes. Many homeowners consolidate high-interest debts like credit cards or personal loans with equity release. - Does it cost money to release equity?

Yes — costs may include valuation, legal, or processing fees. However, competitive terms often outweigh these costs. - Can I release equity as cash?

Yes. You can access up to €100,000 as a lump sum for approved purposes (e.g., renovations, education, helping family). - Can equity release repay an existing mortgage?

Yes. Many use equity release to refinance or clear an existing mortgage. - Can I release equity to buy out a partner’s share?

Yes, it’s common in separation/divorce cases. - What is the LTV for buy-to-let equity release?

Typically up to 70% for loans up to €1 million, and up to 65% for €1–1.25 million. Pension-related buy-to-lets are capped at 50%. - Is a home equity loan a good idea?

Yes — if used strategically. It can unlock capital for reinvestment, debt repayment, or personal financial management. - Can it be repaid early?

Yes. Most lenders allow early repayment, often penalty-free. - Is leveraging equity better than a personal loan?

Often, yes. Equity release generally offers lower rates and larger amounts than personal loans, plus potential tax benefits for investors.

CONCLUSION

In summary, equity release mortgages present a dynamic opportunity for homeowners in Ireland to harness the value within their homes for various needs. Whether you’re seeking financial leverage for home improvements, funding a loved one’s new home, or investing in yourself through education, this option offers versatility and practicality. As highlighted in real-life scenarios, individuals have leveraged equity both creatively and effectively to enhance their lives.

Understanding the benefits, eligibility criteria, and financial requirements is crucial before diving into an equity release mortgage. It’s not merely a tool; it’s a strategic option that can transform how you approach unexpected expenses or long-term goals. With fluctuating market conditions and changing personal circumstances, having access to your home’s equity can provide peace of mind and stability during uncertain times.

Embarking on this journey requires careful consideration of your personal circumstances and goals. For those ready to take the next step towards unlocking their home’s potential, Money Maximising Advisors stands as a valuable partner. Reach out today and let us guide you through this empowering journey with confidence. Let them handle the details while you focus on maximising your financial opportunities.