When a loved one passes away, the emotional burden can be overwhelming. In addition to grief, there are often legal and financial responsibilities that surface. One of these is inheritance tax, which sometimes catches heirs off guard. Understanding how this tax works in Ireland is crucial for anyone dealing with an estate or considering their own legacy planning.

Inheritance tax in Ireland isn’t just about numbers; it’s about navigating a complex landscape of rules and regulations that can significantly impact what you receive from your loved ones. Whether you’re an heir trying to make sense of your obligations or someone looking to plan ahead for future generations, having a solid grasp on Irish inheritance tax laws will empower you.

Join us as we delve into the intricacies of inheritance tax in Ireland—dissecting its rules, calculations, and potential pitfalls so you can approach this sensitive topic with confidence and clarity.

What Is Inheritance Tax in Ireland?

Inheritance tax, known as Capital Acquisitions Tax (CAT) in Ireland, is a tax imposed on individuals who receive assets from a deceased person’s estate. This includes cash, property, and various types of investments.

The intent behind this tax is to ensure that wealth transfer contributes to public finances. It’s important for beneficiaries to understand their responsibilities under these rules.

When someone passes away, the value of the inherited assets may trigger this tax depending on several factors such as relationship to the deceased and overall asset value.

Each case can be unique, presenting different circumstances and obligations for heirs. Familiarising oneself with how inheritance tax operates plays a crucial role in financial planning during what can already be an overwhelming time.

Who Has to Pay Inheritance Tax?

Inheritance tax in Ireland, officially known as Capital Acquisitions Tax (CAT), primarily affects those who receive assets from a deceased person’s estate. But not everyone inherits the same way.

If you are a beneficiary of property or money left to you, it’s essential to understand your potential tax obligations. The amount you’ll owe depends on the value of what you inherit and your relationship with the deceased.

Close relatives like children and spouses benefit from higher thresholds before any tax is applied. In contrast, distant relatives or friends might find their inheritance taxed at lower thresholds, making it crucial for them to be aware of their financial responsibilities.

Moreover, timing plays a role; if you’re set to inherit soon, staying informed about current rates and exemptions can save significant amounts down the line. Always consult professionals when navigating these waters for tailored advice specific to your situation.

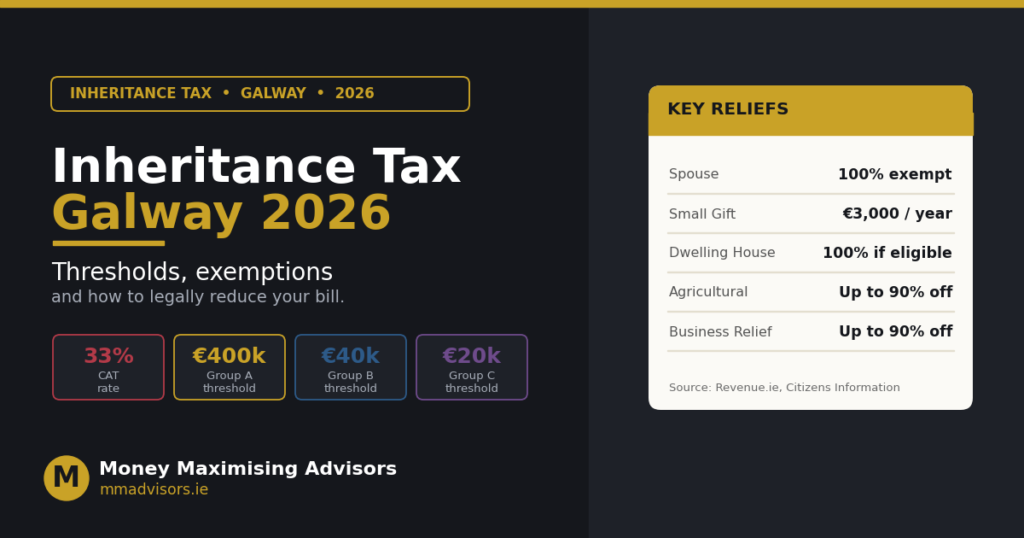

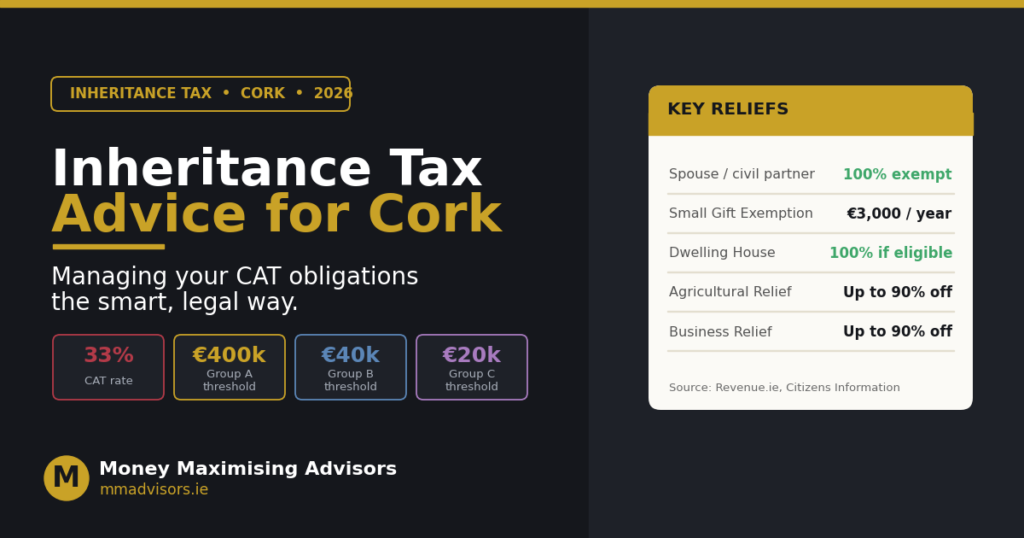

Inheritance Tax Thresholds and Tax-Free Allowances (2025 Update)

Inheritance Tax thresholds and tax-free allowances are crucial aspects of the Irish tax system. As of 2025, these figures have been updated, reflecting the changing economic landscape.

In Ireland, inheritance tax is governed by Capital Acquisitions Tax (CAT). The threshold for gifts or inheritances varies depending on your relationship with the deceased. For example, close relatives like children benefit from a higher threshold compared to distant relatives or friends.

The current thresholds help ensure that smaller estates can pass hands without heavy taxation burdens. Understanding these limits is essential when planning for wealth transfer.

Tax-free allowances exist as well. Certain exemptions apply based on specific criteria, such as receiving a family home under certain conditions. Familiarity with these nuances enables beneficiaries to navigate the complex rules effectively and make informed financial decisions moving forward.

How to Calculate Inheritance Tax in Ireland?

Calculating inheritance tax in Ireland involves several key steps.

- First, determine the value of the assets you’re inheriting. This includes property, money, and personal belongings.

- Next, identify your relationship to the deceased. The rate at which inheritance tax is charged can vary depending on whether you are a Class A (child), Class B (sibling or niece/nephew), or Class C (more distant relatives) beneficiary.

- Once you’ve established this, subtract any applicable tax-free thresholds from your total inheritance amount. These thresholds differ based on your class relationship with the deceased.

- Apply the current inheritance tax rates to calculate what you’ll owe. Keeping detailed records throughout this process will ensure an accurate calculation and help avoid potential disputes later on.

For more precise figures tailored to your situation, consider using an inheritance tax calculator specific to Ireland’s regulations.

Let Money Maximising Advisors guide you through Ireland’s inheritance tax rules and maximise your savings legally.

Common Reliefs and Exemptions

In the realm of Inheritance Tax in Ireland, there are several reliefs and exemptions that can significantly ease the financial burden on heirs.

- One notable exemption is the Group Thresholds, which allows individuals to inherit a certain amount tax-free based on their relationship with the deceased.

- For example, immediate family members such as children and spouses benefit from higher thresholds compared to distant relatives or friends. This distinction is crucial when planning your estate.

- Another important relief is Agricultural Relief. If you inherit farmland or agricultural assets, this can provide substantial reductions in taxable value under specific conditions.

- Business Relief offers similar advantages for those inheriting a business. Holding onto operational businesses without incurring hefty taxes helps keep family enterprises thriving through generations.

Understanding these nuances can help beneficiaries navigate their potential liabilities more effectively while maximising what they ultimately retain from an inheritance.

Filing and Paying Inheritance Tax

Filing and paying inheritance tax in Ireland can seem daunting, but understanding the process makes it more manageable. When an individual receives assets from a deceased person’s estate, they typically need to file a return with Revenue.

You must submit your inheritance tax return within four months of the date of death. This is crucial for avoiding penalties or interest charges that could accrue on late payments.

Payment of Irish inheritance tax is due at the same time as filing. Ensure you have calculated the amount owed accurately to avoid surprises later on.

Keep in mind that certain reliefs may apply, potentially reducing your liability significantly. It’s advisable to consult with financial experts or advisors like Money Maximising Advisors who specialise in capital acquisitions tax Ireland for personalised guidance tailored to your situation.

Tips to Minimise Your Inheritance Tax Liability

- Start with gifting to effectively reduce your inheritance tax liability. You can give away a certain amount each year without triggering tax. This can help decrease the value of your estate.

- Consider setting up trusts. They allow you to pass on assets while retaining control during your lifetime. Trusts can be beneficial for both tax relief and asset protection.

- Utilise any available exemptions and reliefs. Certain properties or gifts may qualify for special treatment under Irish inheritance tax rules, so it’s crucial to explore these options.

- Always maintain proper documentation of all transactions and valuations related to gifts or inheritances. Clear records support claims for exemptions or deductions when needed.

- Consult with financial advisors like Money Maximising Advisors who specialise in inheritance planning. Their expertise helps tailor strategies suited to your circumstances, ensuring that you minimise liabilities effectively.

Common Mistakes to Avoid

When navigating inheritance tax in Ireland, several common pitfalls can lead to unexpected liabilities.

- One frequent mistake is failing to understand the relationship between the deceased and the beneficiary. The tax-free thresholds vary significantly based on this relationship, making it crucial to know where you stand.

- Another error is not keeping comprehensive records of all assets. Valuing property inaccurately or overlooking valuable items can inflate your taxable estate unexpectedly.

- Many neglect available reliefs and exemptions that could reduce their liability. Familiarising yourself with options like agricultural relief or business relief can be beneficial.

- Additionally, procrastinating on filing can lead to penalties and interest charges. Timely submission ensures compliance with Irish Inheritance Tax rules.

- Being unaware of changes in legislation is another significant oversight—stay informed about updates in inheritance tax rates and thresholds for 2025 and beyond to effectively plan your estate strategy.

FAQs About Inheritance Tax in Ireland

1. How is inheritance tax calculated?

It’s based on the value of what you inherit, minus your tax-free threshold. The remaining amount is taxed at 33%.

2. Who pays inheritance tax?

The beneficiary (person receiving the inheritance) is responsible for paying the tax, not the estate.

3. Are there any exemptions?

Yes. Spouses, civil partners, and some family homes, farms, or businesses may qualify for full or partial exemptions.

4. When must it be paid?

Inheritance tax is usually due within six months of death or by October 31st of the following year.

5. Do gifts affect inheritance tax?

Yes. Gifts received during a lifetime can reduce your future tax-free allowance, so planning ahead is important.

Conclusion

Understanding inheritance tax in Ireland can seem daunting, but breaking it down into manageable pieces helps demystify the process. The rules surrounding Irish inheritance tax are clear, and knowing who pays, what thresholds exist, and how to calculate your liability is essential for effective financial planning.

With the right information at hand—such as current rates and available reliefs—you can navigate this tax landscape with confidence. Remember that various exemptions may apply based on your relationship with the deceased or specific circumstances surrounding the estate.

To minimise potential liabilities, leverage tax-free allowances effectively while considering professional guidance from experts like Money Maximising Advisors if needed. By avoiding common pitfalls and staying informed about changes in legislation or thresholds, you’ll be better equipped to manage any inheritances wisely.

Speak with Money Maximising Advisors today to reduce your inheritance tax burden and protect your family’s wealth.

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?