Inheritance can be a beautiful thing, and also a complicated pain. Yet along with it can come responsibilities: namely, inheritance tax. For many in Ireland, this complex world can be overwhelming. Perhaps you’re thinking of stretching these unplanned costs out over payments or wondering how you can possibly afford it.

We take a closer look at how inheritance tax in Ireland works and whether or not installment payments make sense. As you do, you’ll learn practical advice about being proactive while inheritance tax planning to protect the future of those you love and to minimise your liabilities.

Either way, whether dealing with an estate or simply just wanting to know more about inheritance tax savings plans for children in Ireland we have you covered. So, Let’s understand this topic in detail!

What is Inheritance Tax in Ireland?

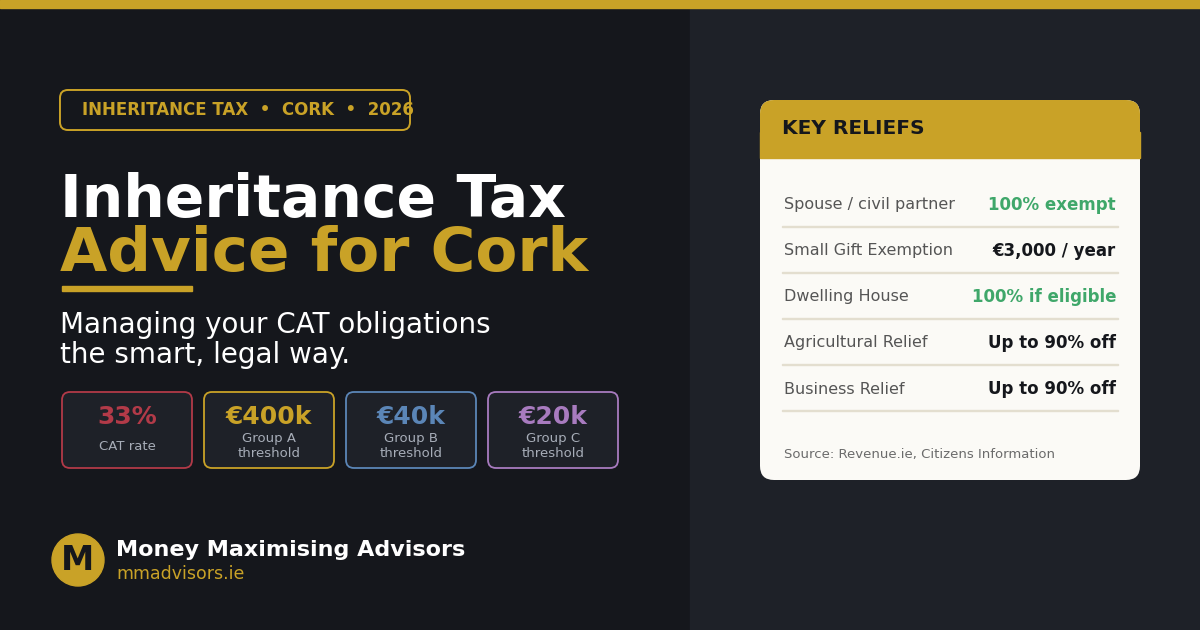

Inheritance tax, also known as Capital Acquisitions Tax (CAT) is a tax on the value of gifts and inheritances received by a person in Ireland. This tax is applicable not only to inheritances but to gifts received during a person’s lifetime.

The current rate of inheritance tax is 33% and this can hit people by surprise when they receive an unexpected inheritance. But there are limits based on your relationship with the deceased that determine how much you will owe.

For instance, if you are a child who has inherited from a parent, you have a higher threshold than distant relatives or friends. Knowing this is crucial to a successful estate plan and to making sure your loved ones are ready when it happens.

What is the Process for Calculating Inheritance Tax in Ireland?

Inheritance Tax Ireland, also referred to as Capital Acquisitions Tax (CAT) is calculated relating to the value of property or other benefits received by the inheritor. That rate is now 33%, levied on anything above a tax-free threshold.

This limitation fluctuates according to the status of the deceased and the heir. So, for example, children are the recipient of a greater exemption than that afforded to siblings and other distant relatives. That is, close relatives can inherit more before they must pay taxes.

All assets (real estate, bank accounts, investment accounts, personal property) must be valued. After you find these values and subtract any debts the estate owes, what’s left is a taxable amount.

It is therefore imperative that accurate records be kept throughout to facilitate transparency and fulfilling legal obligations, while helping to make the best provision for your inheritance tax savings plans for children in Ireland.

Contact Money Maximising Advisors today and find out how you can lawfully space your Inheritance Tax liability out.

Can You Pay Inheritance Tax in Installments?

Inheritance tax can weigh heavily on your finances. A lot of people are curious whether they can repay that debt in increments.

The Irish Revenue Commissioners have a facility for payment of inheritance tax in instalments in certain circumstances. This is especially useful for large debts which require more time to pay back and for which immediate payment may be difficult.

You’ll need to apply to Revenue if you wish to pay in installments. They’re going to look at your situation and decide if you fit them.

It should be remembered that interest can add up on the unpaid balance throughout the payment period. So it is all the more important to plan ahead and minimise all surprises in the future.

Who you should ask for advice If you’re not sure, financial advisers like Money Maximising Advisors or legal professionals could help you with what your options are and what you have to pay (if anything) in terms of inheritance tax.

Paying Inheritance Tax By Installments Pros and Cons

Making inheritance tax payments in instalments can have benefits. Its granting is a feasible and good way to organise the repayment of debts without burdening your budget. By making payments over time, you then don’t have to come up with as much cash up front.

On the downside however, there are drawbacks to take into account. Interest will be charged to unpaid portions, and its balance will continue to grow on you. Also, failure to make a payment could result in penalties and legal action.

The second reason is maintaining flexibility on cash flows. Although spreading payments can seem tempting a first glance, it earmarks funds that could be spent on other needed payments or investments.

It’s important to think about the pros and cons before determining if payments over time are right given your overall financial strategy, goals and priorities.

Other Ways to Pay Inheritance Tax in Instalments

Considerations-Other alternatives, if you have to make payments on this inheritance tax, can be very useful to help you meet your financial obligations.

- One effective intervention is gift giving. You can decrease the taxable estate value by transferring assets or cash to beneficiaries while you are still alive. There are also statutory annual gift exemption limits under Irish law, that you should be aware of.

- Trusts can also be useful to have in place. Through trusts, you can move assets beyond your estate, reducing potential taxes. This is a way to have the say-so in how and when heirs are paid their legacy.

- Furthermore, inheritance tax insurance policies tailored to cover inheritance tax can help to alleviate future pressures. These policies trigger a lump sum payment in the event of your passing, which means your heirs are able to access cash to pay any tax debts with ease.

- You can consult with specialists such as Money Maximising Advisors who have experience providing personalised inheritance tax saving plans for families.

Contact Money Maximising Advisors today we can help you instead we installments and decrease any financial stress you might experience.

Critical Points to Consider When Planning Ahead

Inheritance Tax In Ireland Timing is key when considering inheritance tax in Ireland. It is important to know the boundaries. Each beneficiary’s tax-free threshold will vary, depending on the relationship with the deceased.

- Consider gifts in your own life as well. These can lower your taxable estate and help you transfer as much wealth as possible to children or other loved ones.

- A professional such as Money Maximising Advisors can give you personalised advice which suits your funds.

- Accurate record keeping of assets and valuations will facilitate the process down the road. This certainty reduces controversy and is consistent with tax policy.

- Remember to review your estate plan often, especially following major life changes including marriage and the birth of children. Might need to be tweaked to fit your objectives and current Irish inheritance tax laws.

FAQ’S:

What is the current inheritance tax in Carrick Ireland?

The so-called rate of inheritance tax in Ireland is 33%. That also goes for any amount in excess of a specified level, which depends on the relationship between the deceased and the beneficiary.

What are the exceptions for inheritances?

Yes, there are limits to the tax exemption ireland. For instance those who are close kin fare better than distant relatives or strangers. When you’re meeting with an estate planning attorney, it’s important to consider these thresholds.

Can gifts impact my inheritance tax liability?

Absolutely. Gifts can be considered part of your total inheritance and might affect how much you owe in taxes down the line. Maintain Full Inventory Of All Gifts Received – Prevents Unforeseen Surprises In The Future.

Can one challenge an inheritance tax assessment?

Yes, if you think an assessment is out of whack, there’s a formal process for appeal. Securing the guidance of professionals who understand the intricacies of Irish inheritance law is recommended in this process.

Conclusion

Inheritance tax Ireland can be a confusing system, particularly when you have only recently been granted the responsibility of dealing with your loved one’s estate. Knowing how this tax works, and how you can pay it off, is important for successful financial planning.

Investigating options such as inheritance tax saving plans for children in Ireland may provide more palatable routes forward. Establishing these plans early on helps reduce possible liabilities by allowing for future generations to take advantage of sound financial planning.

You need to take advice from professionals with expertise in Irish inheritance tax and money maximising strategies. They can walk you through the ins and outs of gift exemptions, allowances and other vehicles for shrinking your taxable estate.

By weighing up all your choices and planning ahead of time, you have a better chance of negotiating the minefield that is inheritance tax in a way that protects your family’s wealth in the longer term.

Call Money Maximising Advisors at +353 91 393 125 to find out about flexible plans which include paying by instalment and clever tax planning.

- Gift/Inheritance Tax Savings Plans: How Do I Avoid Inheritance Tax on My Savings?

- Inheritance Tax Advice In Ireland: Where Can I Get Advice on Inheritance Tax?

- How to Avoid Paying Inheritance Tax in Ireland?

- How can I Reduce My Inheritance Tax in Ireland?

- What is the Most You can Inherit without Paying Taxes?

- Inheritance Tax Q&A: Get Answers To Your Most Pressing Questions About Protecting Your Family’s Inheritance

- Understanding the Tax Implications of Section 73 Policy in Ireland

- Section 72 Policies in Galway, Ireland: What happens if you can’t pay inheritance tax in Ireland?