| Quick answer An SPV mortgage Ireland lets investors buy property through a limited company typically a Special Purpose Vehicle incorporated solely to hold and rent property. You still need a 30% deposit (70% LTV cap applies), expect a rate uplift of 0.5–1% versus a personal BTL, and the directors will need to sign a personal guarantee. The benefit is tax: rental profits stay inside the company at corporation-tax rates rather than being taxed at your personal marginal rate. |

If you are looking to scale an Irish property portfolio or you are a higher-rate taxpayer trying to make BTL economics actually work, a limited company mortgage also called a special purpose vehicle mortgage is one of the most under-used tools in the market. This pillar guide explains exactly what an SPV mortgage is, how the structure works in practice, when it pays for itself (and when it doesn’t), and how to go from incorporation to drawdown without tripping over the small details Irish lenders care about. At Money Maximising Advisors, we arrange SPV mortgages for investors across Ireland.

| This article sits within our Mortgages hub and supports the cluster pages our SPV clients use most often, including Buy-to-let Mortgages, Mortgage Comparison Advice, Directors Pension, Corporate Investments and Equity Release Mortgages. |

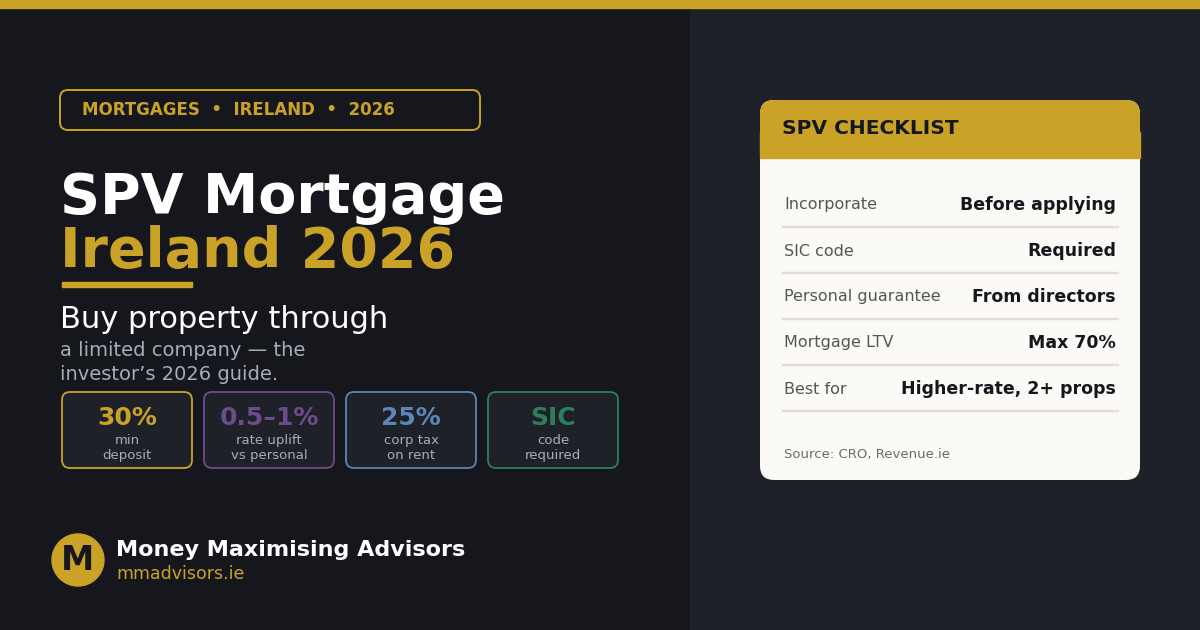

Four parameters that define every SPV mortgage application in Ireland.

Quick answers: six questions every Irish SPV investor asks

What is an SPV mortgage in Ireland?

An SPV mortgage is a buy-to-let mortgage issued in the name of a Special Purpose Vehicle a limited company incorporated specifically to hold and let investment property. The company owns the property; you own the company’s shares as a director and shareholder.

How do limited company mortgages work in Ireland?

The mechanics are similar to a personal BTL: 30% deposit, 70% LTV cap, ICR of 125–145% and a 5–8% stress test. The key differences are that the company is the borrower (not you personally), the directors sign a personal guarantee, the lender pool is smaller, and rates run roughly 0.5–1% higher than equivalent personal BTL pricing.

Is an SPV mortgage cheaper than a personal BTL?

On the headline rate, no SPV rates are usually a notch higher. On the total after-tax return, however, an SPV can be substantially cheaper for higher-rate taxpayers because rental profits stay inside the company at corporation-tax rates rather than being hit by 40% income tax plus USC and PRSI.

What deposit do I need for an SPV mortgage in Ireland?

Minimum 30% deposit the Central Bank’s 70% LTV cap on buy-to-let lending applies regardless of whether the mortgage is in personal or company name. Some specialist SPV lenders price more keenly at 65% LTV (i.e. 35% deposit).

How is rental income taxed inside an SPV?

Rental profits inside an Irish SPV are taxed at the corporation-tax rate that applies to passive income (typically 25%, not the 12.5% trading rate). If profits are retained inside the company rather than distributed, a close company surcharge can apply. Extracting profits to you personally then triggers additional income tax, USC and PRSI. The structure works best when profits are reinvested into more property.

Can I move existing properties into an SPV?

Yes, but it is a sale and re-purchase between you and the SPV, which triggers stamp duty (and potentially CGT on the personal side). It is rarely worth doing for a single existing property, but can make sense as part of a wider portfolio restructure always model the full tax cost before committing.

What is a Special Purpose Vehicle (SPV) and when should you use one?

A Special Purpose Vehicle is a private limited company incorporated for a single defined purpose in this context, holding and renting property. The company has at least one director and one shareholder (often the same person), a registered office in Ireland, and Articles of Association. The SIC code used at incorporation must reflect property ownership and letting; the wrong code can prevent lenders from approving a mortgage.

Where the structure earns its keep:

- Higher-rate taxpayers. If your marginal income tax rate is 40% plus USC and PRSI, the personal route can cost you over half of every rental euro. An SPV defers and reduces that hit.

- Portfolio investors. Two, three or more properties under one company give cleaner accounts, ringfenced liability and easier inter-property cashflow.

- Family planning. Shares in the SPV can be transferred or gifted using the same tools that work for any private trading company we model this with our Inheritance Tax Advice team.

- Reinvestment-focused investors. If profits will be ploughed back into more property rather than extracted, the SPV is almost always the better wrapper.

Where it doesn’t pay:

- Single property held for the long term. Setup costs, annual filings and a higher rate often outweigh the tax saving on one property.

- Lower-rate taxpayers. The tax gap between personal and SPV ownership narrows considerably.

From SPV setup to mortgage offer, the 7-step process

With the right broker and clean documentation, this can move from incorporation to AIP inside a week.

1. Incorporate the SPV with the correct SIC code

Register a private limited company through the Companies Registration Office (CRO). Most lenders require the company to be incorporated before you apply, not on the same day.

2. Open a business bank account in the company’s name

Standard requirement for receiving rental income and paying the mortgage.

3. Pull together documentation

Personal income evidence, ID, credit checks, and details of the company and target property. Meeting BTL mortgage requirements early is the single biggest determinant of speed.

4. Shortlist SPV-friendly lenders

Not every Irish lender writes SPV mortgages, working with a broker who knows the live panel is essential. Our Mortgage Comparison Advice team maintains a current list of active SPV lenders.

5. Submit the application with directors’ personal guarantee

Almost all SPV lenders require the directors and substantial shareholders to sign a personal guarantee. This means that despite the company being the borrower, the directors remain liable if payments are missed.

6. Lender values the property, runs ICR + stress test, issues Approval in Principle

With clean paperwork, AIP can come through in a matter of days; some lenders issue a formal offer within the same week.

7. Drawdown and RTB registration

Solicitor completes the conveyancing, drawdown is processed, the tenancy is registered with the Residential Tenancies Board within 30 days of the lease start. Welcome to the landlord life.

| Looking to set up an SPV and arrange a mortgage in the same week? Book Now for a free consultation, or Enquire Now and we will be in touch within one working day. |

Tax: SPV vs personal ownership

Indicative comparison on €10,000 of net rental profit for a higher-rate Irish taxpayer.

The honest answer is that no SPV decision should be made on the headline tax rate alone. The personal route taxes rent at your marginal income tax rate plus USC and PRSI around 51% for a higher-rate Irish taxpayer. The SPV route taxes rental profits at corporation-tax rates (typically the 25% “passive income” rate), with a 15% close-company surcharge potentially applying to undistributed investment income.

That gives an effective in company rate of around 36% if profits are retained still meaningfully better than 51%, particularly for portfolio investors reinvesting profits into the next purchase. When you eventually extract money via salary or dividend, additional personal tax applies on the way out. The structure works best when:

- Profits are reinvested into more property rather than extracted in cash.

- You plan to hold for many years — long enough that the deferral compounds.

- You expect to be a higher-rate taxpayer for most of those years.

Tax planning for an SPV is non-trivial we run the full numbers with clients before they sign anything.

Why work with Money Maximising Advisors on your SPV mortgage?

| About Money Maximising Advisors Limited is a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland. We arrange SPV and personal BTL mortgages for property investors across the country and coordinate the broader tax, succession and protection picture alongside the mortgage. Our advisors hold QFA, RPA and FA qualifications and work daily with the small group of Irish lenders actively writing SPV business in 2026. Every recommendation we make is documented in a written Statement of Suitability, our regulatory standard. To learn more, visit about us. |

Common SPV mortgage mistakes Irish investors make

- Wrong SIC code at incorporation. If the company is registered with a generic trading code, many lenders will not approve the mortgage; sort this first.

- Forgetting the personal guarantee. Limited liability is the headline benefit, but directors’ personal guarantees mean you remain on the hook if the SPV defaults.

- Ignoring the close-company surcharge. Undistributed rental profits can attract a 15% surcharge — model it before assuming a clean corporation-tax win.

- Trying to transfer an existing property in. It is a sale, with stamp duty and CGT consequences. Take advice before moving anything.

- Underestimating the running costs. Annual accounts, CRO filings, an accountant and a separate business bank account are all ongoing overheads.

Most-read SPV & BTL guides

- Limited Company BTL in 7 Days: From SPV Setup to Mortgage Offer

- Buy-to-let Mortgages Ireland: A Complete Investor Guide

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

Frequently asked questions about SPV mortgages in Ireland

1. How long does it take to set up an SPV and get a mortgage in Ireland?

Incorporation can be completed within a few business days through the CRO. With the right broker preparing the file in parallel, an Approval in Principle can follow within a week of incorporation, some experienced clients move from setup to formal offer in the same week.

2. Do I need an accountant for an SPV?

Yes — an SPV must file annual statutory accounts with the CRO and a corporation tax return with Revenue every year. The accountant fee is a recurring overhead and should be modelled into your projected returns from day one.

3. Can my spouse or partner be a director of the SPV?

Yes, and it is commonly done. Joint directors can both sign the personal guarantee, and the share structure can be designed around your wider tax and inheritance planning.

4. Can an SPV mortgage be interest-only?

Some specialist SPV lenders offer interest-only options, particularly for experienced landlords with multi-property portfolios. The criteria are stricter than for personal BTL and the rate premium tends to be larger.

5. What happens if the SPV defaults on the mortgage?

The lender will first look to the property as security and then to the directors’ personal guarantees. “Limited liability” does not insulate directors from the guaranteed amount of the mortgage itself.

Ready to set up an SPV and arrange the mortgage?

Whether you are incorporating your first SPV or refinancing an existing portfolio into one, our team handles the full process — lender selection, application, structure design and coordination with your accountant and solicitor. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: You may have to pay charges if you pay off a fixed-rate loan early.

Central Bank lending rules, corporation-tax rates and the close-company surcharge referenced are correct as at June 2026 and sourced from the Central Bank of Ireland, Revenue.ie and the Companies Registration Office. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. SPV structures involve tax considerations that change with personal circumstances; you should seek personalised advice from a Qualified Financial Advisor and a tax adviser before incorporating an SPV or applying for an SPV mortgage.