| ⚠ WHY THIS MATTERS NOW Three reasons Irish families are re-opening estate plans this year that were fine two years ago. ▶ CAT thresholds moved in October 2024. Group A jumped from €335k to €400k; Group B to €40k; Group C to €20k, and stayed unchanged in Budget 2026. Any will drafted on the old figures now leaves headroom unused. ▶ Property values kept rising through 2025. Irish house prices are up double-digit percent since 2022, CAT bills that were manageable have quietly moved into six-figure territory. ▶ The 33% rate has not moved in 12 years. Anything inherited above the threshold is still taxed at 33%, which is why every family with a home and pension needs a written plan, not just a will. |

If you own a home in Ireland worth more than €500,000, or a pension pot approaching seven figures, or a business you plan to hand on, estate planning is not an optional exercise. Inheritance tax Ireland (technically Capital Acquisitions Tax or CAT) is charged at 33% on the value of any inheritance or gift above the recipient’s lifetime threshold, and Irish families routinely leave hundreds of thousands of euro on the table by not using the reliefs, exemptions and structures that exist specifically to reduce that bill. This pillar guide covers the current CAT thresholds, the four main relief mechanisms, how to legally reduce inheritance tax in Ireland, and what an estate plan looks like from first meeting to final signed documents. At Money Maximising Advisors, we run written estate reviews for clients across Ireland, with regional partners jcfc.ie in Donegal and moneysense.ie in Kerry.

The 6 questions every Irish family asks about estate planning

What is estate planning?

Estate planning is the deliberate structuring of your assets property, pensions, investments, business interests, so that on your death they pass to the people you want, in the way you want, with the least tax leakage possible. In Ireland, the main tax to worry about is Capital Acquisitions Tax (CAT), but a good plan also covers wills, powers of attorney, and business succession.

How can I reduce inheritance tax legally?

Four main routes:

(1) use the Small Gift Exemption (€3,000 per donor per donee per year) to move money out of the estate before death

(2) qualify for the Dwelling House Exemption where possible

(3) take out a Section 72 life policy to pre-fund the tax bill, and

(4) fund a Section 73 policy to cover gift tax on planned lifetime transfers. Combined intelligently, these can eliminate most CAT bills for typical Irish estates.

What is gift tax in Ireland?

Gift tax is a form of Capital Acquisitions Tax charged on lifetime transfers rather than inheritances. The 33% rate, the group thresholds and the exemptions are all the same as for inheritance tax, you only get one lifetime threshold, which applies to gifts and inheritances combined.

How much money can you gift tax-free in Ireland?

Any donor can give up to €3,000 per year to any donee under the Small Gift Exemption and this doesn’t count against the lifetime CAT threshold. A couple with three children and six grandchildren can move €54,000 per year (€6,000 into each of nine recipients) out of the estate entirely tax-free. Over 10 years, that’s €540,000 gone from the estate legally, no CAT liability.

What is Capital Acquisitions Tax (CAT)?

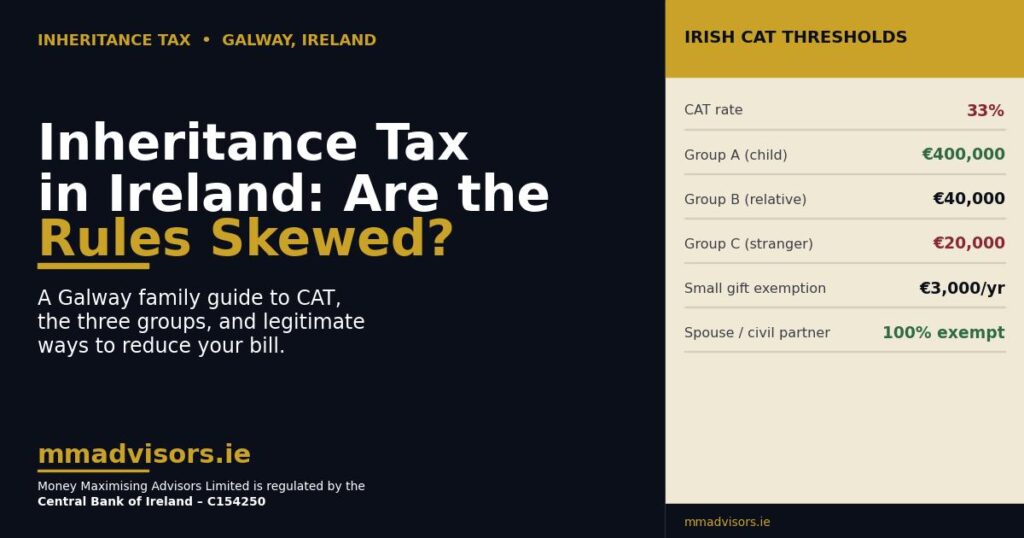

CAT is Ireland’s single tax on gifts and inheritances, charged at 33% on the value received above the recipient’s lifetime group threshold. There are three groups:

- Group A: Parent to child €400,000 lifetime threshold

- Group B: Between relatives (sibling, aunt/uncle, niece/nephew, lineal ancestor) €40,000

- Group C: Everyone else, including friends and unrelated recipients €20,000

Thresholds are lifetime cumulative, the first €400,000 a child receives from any parent across their lifetime is tax-free, but every euro above that is taxed at 33%.

Who pays inheritance tax in Ireland?

The recipient, not the estate. In Ireland, CAT is levied on the person receiving the gift or inheritance, not on the deceased’s estate as a whole. This is different from the UK, where inheritance tax is a charge on the estate. Recipients file Form IT38 with Revenue by 31 October of the year following the inheritance/gift once they cross 80% of their lifetime threshold.

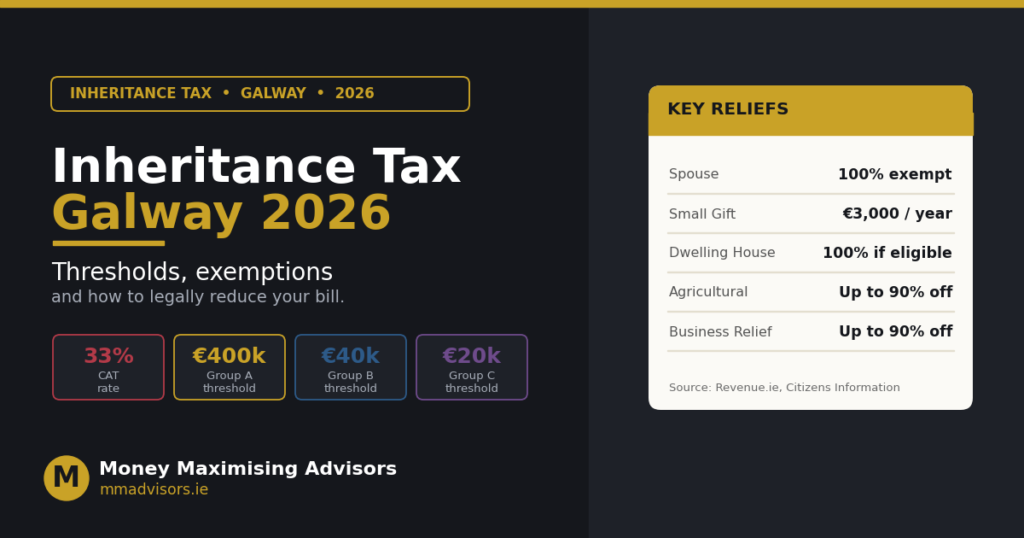

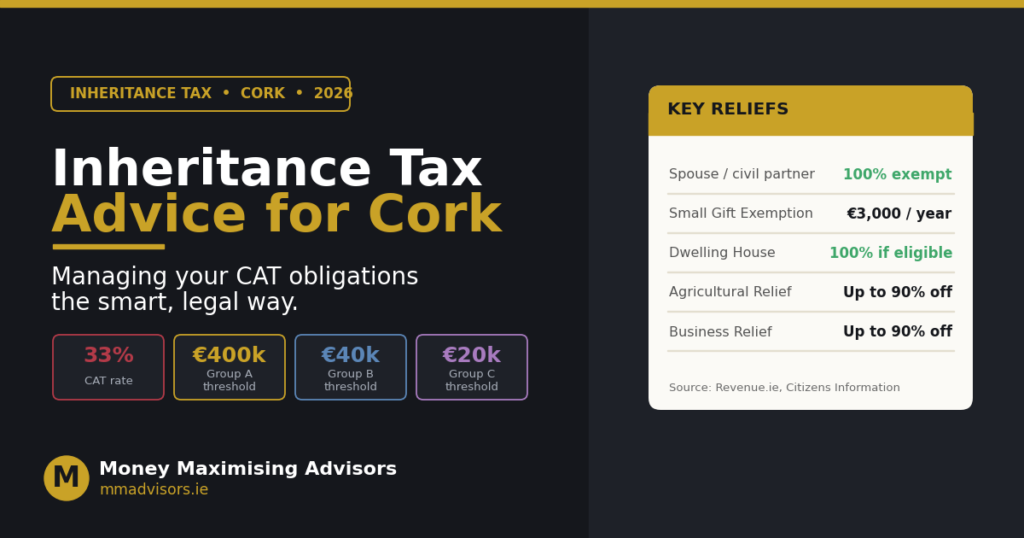

The four legal ways to reduce your CAT bill

Ireland’s four most-used inheritance and gift tax planning tools, compared.

1. The Small Gift Exemption — the tool everyone can use

The Small Gift Exemption lets any donor give any donee €3,000 per calendar year, tax-free, with no impact on the lifetime CAT threshold. It’s the single most under-used estate-planning tool in Ireland because it seems small, but multiplied over multiple donors, multiple donees, and multiple years, it compounds into hundreds of thousands of euro. There is no limit on the total the exemption can shelter over a lifetime; the only limits are €3,000 per donor-donee pair per year.

A Small Gift Exemption Savings Plan structures this into regular, documented transfers, usually into an investment account for a child or grandchild, with the paper trail Revenue expects to see.

2. The Dwelling House Exemption for specific family situations

If someone lives in the property they inherit as their sole or main home for at least three years before the inheritance and continues to live there for six years after, and doesn’t own any other property, the Dwelling House Exemption can make the property inheritance completely CAT-free. It’s most commonly used by adult children who moved home to care for elderly parents, but the qualifying conditions are strict and Revenue enforce them closely.

3. Section 72 policies pre-funding the CAT bill

A Section 72 Policy is a life-of-two lives insurance policy whose proceeds paid on the second death, can be used to pay the CAT bill without the pay-out itself being taxable. Section 72 status must be applied for at Revenue at the time of purchase, and the policy must be maintained until the second death. It’s the go-to tool for larger estates where liquidity, not the tax rate itself, is the real problem (heirs facing a six-figure CAT bill on an inherited farm or house they don’t want to sell).

4. Section 73 policies for lifetime gifting

Where Section 72 covers inheritance tax on death, a Section 73 Policy covers gift tax on lifetime transfers. Structured as an eight-year regular-premium savings plan, the proceeds are ring-fenced to pay CAT on gifts made from the pot. Useful for grandparents planning to gift adult grandchildren above the Group B threshold.

Estate planning across the Irish regions

CAT rules are national, but assets, farms in Donegal, family homes in Dublin, holiday properties in Kerry are stubbornly regional. The MMA group covers the whole country through three complementary brands:

| MMA GROUP | IRELAND-WIDE COVERAGE Same regulated firm, same standards, three brands covering different regions of Ireland. |

FLAGSHIP | NATIONAL mmadvisors.ie Head office Tuam, Co Galway. Full product suite, national coverage. NORTH WEST IRELAND jcfc.ie Joe Coyle Financial Consultants, Mountcharles, Co Donegal. Business-owner and family specialists. SOUTH WEST IRELAND moneysense.ie Money Sense, Killarney, Co Kerry. 40+ years serving Munster families and pre-retirees. |

Estate planning in 5 steps

A structured order of operations, in this exact order for anyone starting an Irish estate plan.

Step 1 — List every asset

Home, holiday property, savings, investment accounts, pension funds, business interests, life insurance, digital assets. Include current market value, not what you paid.

Step 2 — Map recipients against thresholds

Who gets what? For each recipient, calculate the Group A/B/C threshold that applies and estimate how much of it is already used.

Step 3 — Estimate the CAT liability

On the current draft, what will each recipient owe? If the answer is “nothing”, congratulations, your existing plan is efficient. If it’s in six figures, keep going.

Step 4 — Apply reliefs and structures

Layer in Section 72, Section 73, Small Gift Exemption, Dwelling House Exemption, Business Relief and Agricultural Relief where they apply. Model the reduced CAT bill, in most Irish estates, the CAT liability drops by 60–90% with proper structure.

Step 5 — Draft, sign, and review

Update the will. Draft an Enduring Power of Attorney (a solicitor task). Diarise an annual review, estate plans decay quickly when property values and family circumstances change.

| CLIENT STORY How a Galway family reduced a €198k CAT bill to €12k Michael and Ann, both 68, live in Galway. Between them they own a family home worth €820,000, a rental property worth €340,000, pension funds of €410,000 combined, and cash savings of €85,000. They have three adult children. On the original plan (everything split equally on second death, no other structure), each child was projected to inherit approximately €552,000 — €152,000 over their Group A threshold. Each child would owe ~€50,000 in CAT, €150,000 total, climbing to €198,000 once likely growth in property values was modelled. With the plan we structured, they combined: (1) a Section 72 policy covering €120k of projected CAT, (2) Small Gift Exemption transfers of €3k/year from each parent to each child and grandchild (€54k/year), (3) gifted downsizing of the rental property into a family trust structure over 8 years, and (4) an updated will using the higher post-Oct 2024 thresholds. Final projected CAT bill: €12,000 across all three children combined. The Section 72 premium cost them €340/month, a fraction of the tax it will save. |

Common estate-planning mistakes Irish families make

✗ Assuming their will ‘handles it’. A will directs who gets what, it does nothing to reduce the tax they pay.

✗ Ignoring the Small Gift Exemption. Ten years of €3k gifts across a family of grandchildren moves half a million out of the estate legally. Most families never use it.

✗ Waiting for the ‘right time’ to do a Section 72. Life-cover premiums rise sharply with age. Every year you wait costs materially more.

✗ Not updating after property value moves. A house that was worth €450k in 2020 may be worth €680k today, the CAT bill quietly tripled.

✗ Skipping the Enduring Power of Attorney. Not strictly a CAT issue, but a huge estate-planning gap. Without an EPA in place, incapacity means Ward of Court proceedings, which are slow and expensive.

✓ Reviewing the plan annually. Thresholds move, property values move, children’s circumstances change. An estate plan reviewed every 12 months is a plan that keeps working.

Reviewed by qualified financial advisors

| REVIEWED BY MONEY MAXIMISING ADVISORS This guide has been fact-checked and reviewed by the advisory team at Money Maximising Advisors Limited, a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland and authorised as a Multi-Agency Intermediary across the main Irish pension providers, life insurers and lenders. Our advisors hold QFA, RPA, FA and Specialist Investment Adviser (SIA) qualifications, maintain annual Central Bank-mandated CPD, and document every recommendation in a written Statement of Suitability. Verify our authorisation on the Central Bank public register at registers.centralbank.ie. Regional partners in the MMA group: jcfc.ie (Donegal / North West) and moneysense.ie (Kerry / South West). |

Related reading

| Related post | Category | Link |

|---|---|---|

| Demystifying Inheritance Tax in Ireland: Rules and Calculations | Inheritance Tax | Read more → |

| How a Section 73 Policy Can Reduce Inheritance Tax in Ireland | CAT Reliefs | Read more → |

| Inheritance Tax Ireland | How To Avoid Legally | Inheritance Tax | Read more → |

| Inheritance Tax Ireland — How to Reduce your Tax Burden | Inheritance Tax | Read more → |

| Gift Tax in Ireland: How Does Gift and Inheritance Tax Work? | Gift Tax | Read more → |

Before you leave — quick FAQ

Do spouses pay CAT on gifts and inheritances between them?

No, transfers between spouses (or registered civil partners) are entirely exempt from CAT under Irish law. That’s why most estate plans focus on what happens on the second death, not the first.

How is CAT calculated on a jointly owned home?

For a couple, the surviving spouse inherits the deceased’s half tax-free. On the second death, the whole property passes to the children (usually as a joint inheritance) with each child using their Group A threshold. Careful record-keeping of past gifts matters, previous transfers reduce the remaining threshold.

Can I make gifts ‘in contemplation of death’ to reduce CAT?

Deathbed gifts made within two years of death are treated as inheritances by Revenue, the CAT treatment doesn’t change. Genuine lifetime gifts, made and documented well ahead of death, are effective. Timing and documentation matter.

Does the Fair Deal scheme affect estate planning?

Yes, Nursing Homes Support Scheme (Fair Deal) charges are calculated against your assets, including your home (with the 3-year cap). Estate planning that ignores potential care costs is incomplete.

Ready for a written estate review?

| Book a no-obligation inheritance tax review Our team will project your CAT bill under current rules and show you the exact combination of reliefs to reduce it. → Enquire Now | → Book an Appointment | → Contact Us |

Important information

Money Maximising Advisors Limited is regulated by the Central Bank of Ireland and authorised as a Multi-Agency Intermediary. All figures, tax thresholds, State Pension rates and regulatory references in this article are correct as at June 2026, based on Revenue.ie, the Pensions Authority and the Central Bank. This article is for general information only and does not constitute financial, tax or legal advice. Individual circumstances vary; you should seek personalised advice from a Qualified Financial Advisor before making any pension, protection, investment or estate-planning decision. CAT thresholds, rates and reliefs are subject to change in Finance Acts. Estate planning must be regularly reviewed. Legal advice from a solicitor is required for wills and Enduring Powers of Attorney; we work alongside your solicitor on the financial-planning side.