| Quick answer In Ireland, Capital Acquisitions Tax (CAT) applies at 33% on any inheritance or gift above your group threshold; €400,000 for a child from a parent, €40,000 for closer relatives, €20,000 for anyone else. Galway families can legally reduce a CAT bill through the spouse exemption, the €3,000 Small Gift Exemption, the Dwelling House Exemption, Agricultural Relief (90% off) and Business Relief (90% off). Returns and payment are due by 31 October following the valuation date. |

If you are a Galway family planning an estate or you have just been told you are inheriting a Salthill property, a Clifden farm or a stake in a family business in Knocknacarra the Irish inheritance tax on property Ireland rules are not what most people expect. The CAT group thresholds Ireland use are generous on paper but tighten quickly once property values are factored in, and the inheritance tax threshold Galway residents face is identical to the national rules under Capital Acquisitions Tax Ireland. This guide walks through every threshold, exemption and relief, with a worked Galway example and the same practical tips we use with our clients. At Money Maximising Advisors, our Inheritance Tax Advice team works with Galway families every week to structure inheritances tax-efficiently.

| This article sits within our Inheritance Tax hub and supports Inheritance Tax Advice, Section 72 Policies, Section 73 Policy Savings Plan, Small Gift Exemption Savings Plan and Retirement Planning Advice. |

The four headline numbers that define every Galway CAT calculation in 2026.

Quick answers: every Galway family’s CAT questions

How much inheritance tax do you pay in Ireland?

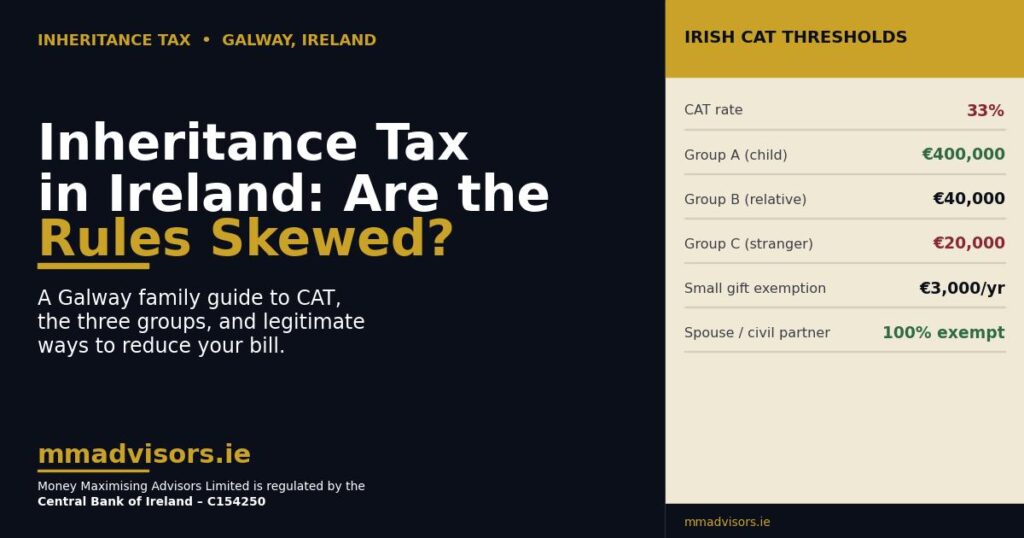

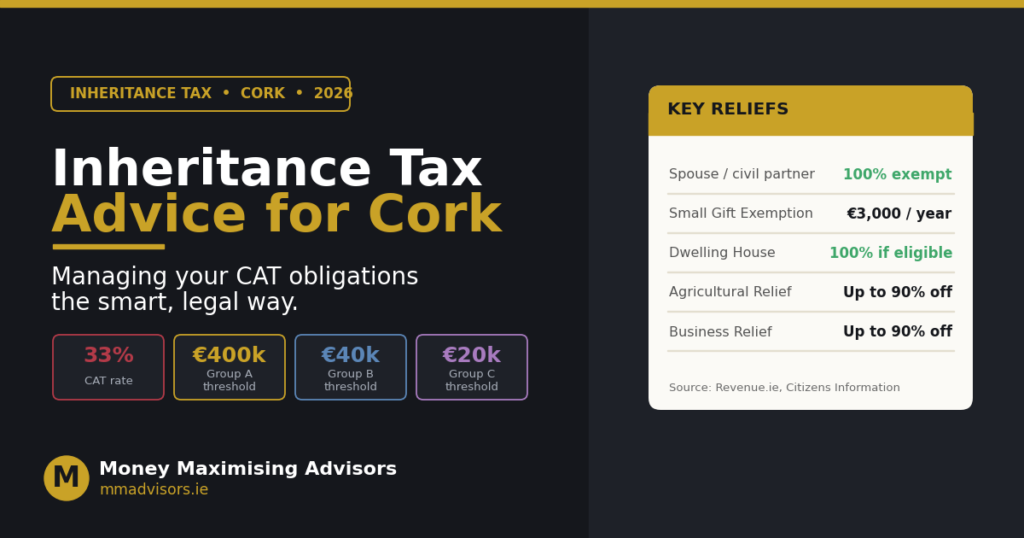

CAT is charged at a flat 33% on the value of any inheritance or gift above your group threshold. Below the threshold, there is no tax.

What is the current Capital Acquisitions Tax (CAT) threshold in Ireland?

Three lifetime thresholds apply, depending on the relationship between giver (the disponer) and receiver (the beneficiary):

- Group A — €400,000: a child receiving from a parent.

- Group B — €40,000: siblings, nieces, nephews, grandchildren and grandparents.

- Group C — €20,000: all other relationships, including unrelated individuals.

These thresholds have applied since 2 October 2024 and were left unchanged by Budget 2026. They are lifetime aggregates — every gift or inheritance received in the same group since 5 December 1991 is added together against the threshold.

How can I reduce inheritance tax legally in Ireland?

Several legitimate routes exist, often used in combination: lifetime gifting via the Small Gift Exemption Savings Plan (€3,000 per giver, per recipient, every calendar year), claiming the Dwelling House Exemption where eligible, claiming Agricultural Relief or Business Relief on qualifying assets, and pre-funding the eventual CAT bill through Section 72 Policies. Most well-planned Galway families use two or three of these together.

Is there a spouse exemption from inheritance tax in Ireland?

Yes; transfers between spouses or registered civil partners are completely exempt from CAT, with no upper limit. A husband can leave the family home and his entire estate to his wife (or vice versa) with no CAT arising at all. This is one of the most powerful features of the Irish system and the foundation many estate plans are built around.

What reliefs are available for agricultural assets in Ireland?

Agricultural Relief reduces the taxable value of qualifying farmland and farm assets by up to 90%. A daughter inheriting a €1,000,000 Galway farm with full relief is assessed on just €100,000; frequently bringing the bill to nil after Group A is applied. The beneficiary must meet Ireland’s strict “farmer” test (broadly, 80% of their assets must be agricultural after the inheritance) and there is a six-year clawback if the conditions are breached.

What is Business Relief for inheritance tax in Ireland?

Business Relief is the equivalent provision for qualifying business assets; typically shares in a genuine trading company, or a sole-trader/partnership business. It also delivers a 90% reduction in taxable value, provided the disponer owned the assets for at least 2 years before an inheritance (5 years before a gift), the business is a real trade rather than a passive investment vehicle, and the recipient holds the assets long enough to clear the six-year clawback (10 years for business development land).

When does inheritance tax need to be paid in Ireland?

CAT runs on a 31 October Pay & File deadline following the relevant “valuation date”; the technical date on which the benefit is treated as received. In broad terms, valuation dates falling between 1 September and 31 August in any year must be filed and paid by the following 31 October. A Form IT38 return is required if the value of all benefits in the same group exceeds 80% of the threshold or if any relief is being claimed.

How CAT is calculated — a worked Galway example

Four steps Revenue takes when assessing CAT on an inherited Galway home.

A daughter living in Salthill inherits a €450,000 family home in Knocknacarra from her father. Earlier in life, she received €100,000 from him in cash gifts. Her CAT liability is calculated as follows:

- Group A threshold: €400,000 (parent → child).

- Aggregate of prior gifts plus current inheritance: €100,000 + €450,000 = €550,000.

- Taxable amount above threshold: €550,000 – €400,000 = €150,000.

- CAT due at 33%: €49,500.

If she is eligible for the Dwelling House Exemption, broadly, she lived in the inherited home with the deceased for three years before the inheritance, has no other property, and continues to live there for six years afterwards — the CAT bill could fall to zero.

| Inheriting in Galway and unsure about CAT? Book Now for a free Inheritance Tax review, or Enquire Now and we will be in touch within one working day. |

The most useful CAT reliefs for Galway families

Five reliefs that, used properly, can take a Galway CAT bill close to zero.

Spouse / Civil Partner Exemption

Unlimited transfers between spouses or registered civil partners are 100% exempt. The cornerstone of every Irish estate plan.

Small Gift Exemption (Gift Tax Ireland)

The Small Gift Exemption lets you give €3,000 per recipient, per donor, per calendar year, outside the lifetime threshold. Two parents can collectively gift €6,000 to each child each year without touching the Group A threshold. Over twenty years, the same parents can move €120,000 per child; entirely outside the CAT net. Many Galway families use a Small Gift Exemption Savings Plan to invest this annual amount on the child’s behalf, growing it tax-efficiently over time.

Dwelling House Exemption (Galway)

The dwelling house exemption Galway beneficiaries can claim mirrors the national rule: the inherited home passes CAT-free if (1) the beneficiary lived there with the deceased for three years before the death, (2) they don’t own any other dwelling at the date of inheritance, and (3) they continue to occupy it as their main residence for six years afterwards. The conditions are strict but powerful; on a €500,000 Galway home, the exemption can save a beneficiary over €30,000 in CAT.

Agricultural Relief

A 90% reduction in taxable value for qualifying farmland and farm assets. The recipient must meet the “farmer” test; in practice, this means at least 80% of their assets must be agricultural after the inheritance, and they must either farm the land themselves for six years, lease it out for six years on a long-term lease, or hold a qualifying agricultural qualification.

Business Relief

The business-equivalent of Agricultural Relief, with the same 90% reduction. It is most relevant to Galway families with owner-managed businesses being passed down to the next generation. Take detailed advice early; the structure of the business and the timing of transfers both matter.

Why work with Money Maximising Advisors on inheritance planning?

| About Money Maximising Advisors Limited is a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland. We work with Galway families on inheritance tax planning every week; from a single Dwelling House Exemption claim to multi-generational structuring involving Agricultural Relief, family-owned business succession and Section 72 funding. Our advisors hold QFA, RPA and FA qualifications and partner with qualified tax advisors where the situation requires it.Every recommendation is documented in a written Statement of Suitability, our regulatory standard. To learn more, visit about us. |

Common Galway CAT mistakes to avoid

- Forgetting prior gifts. Every gift over €3,000/year since 5 December 1991 aggregates against the lifetime threshold — keep records.

- Missing the 31 October Pay & File deadline. Surcharges and interest accumulate fast.

- Assuming the family home automatically qualifies for the Dwelling House Exemption. The residency conditions are strict and frequently missed.

- Not pre-funding the eventual CAT bill. A Section 72 Policy can pay the bill in full at the right moment, sidestepping forced asset sales.

- Trying to retro-fit Agricultural or Business Relief after the inheritance. These reliefs need to be structured ahead of time — not patched on at the deadline.

Most-read inheritance tax guides

- Section 72 Policies Explained: Pre-Fund Your CAT Bill in Ireland

- Small Gift Exemption Savings Plan: Move Wealth Tax-Free Each Year

Frequently asked questions about Galway inheritance tax

Do I have to pay CAT on the family home in Galway?

Possibly not. If you meet the Dwelling House Exemption conditions; broadly, you lived in the home with the deceased for three years, you own no other property, and you continue to live there for six years after; the home passes CAT-free regardless of its value.

Can I gift my children property in Galway during my lifetime?

Yes, but a lifetime gift uses your Group A lifetime threshold the same way an inheritance would. The recipient may also face stamp duty on the transfer, and you may face CGT if the property has gained in value. Lifetime gifting of property usually needs careful tax modelling first.

How long do I have to pay CAT after an inheritance?

If your valuation date falls between 1 September and 31 August, the 31 October deadline of the following year applies. A short ROS-online extension is typically granted into mid-November. Form IT38 is required if your benefits exceed 80% of the threshold or you are claiming reliefs.

Does the spouse exemption apply to unmarried partners?

Only registered civil partners qualify for the full spouse exemption; unmarried co-habiting partners do not. This is one of the most expensive gaps in Irish estate planning and is worth taking specific advice on early.

Can I reduce my CAT bill using a Section 72 policy?

Yes; a Section 72 Policy is a life insurance policy specifically designed to pay an Irish CAT bill on death without itself being subject to CAT. It is one of the most effective tools for protecting the family home or business from forced sale to meet the tax bill.

Ready to talk to an Irish inheritance tax specialist?

Whether you are planning ahead, dealing with a recent inheritance, or modelling a multi-generational transfer, our team will walk you through every relief, exemption and structure available to you. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

CAT thresholds, the 33% rate, Agricultural Relief, Business Relief and the Pay & File deadline referenced in this article are correct as at June 2026 and are drawn from Revenue.ie and Citizens Information. Thresholds and reliefs can change in future Budgets. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. You should seek personalised advice from a Qualified Financial Advisor and a tax adviser before acting on inheritance planning.