| Quick answer In Ireland, mortgage protection insurance Ireland is mandatory for principal-residence mortgages under the Consumer Credit Act 1995. It is normally a decreasing-term life policy that pays off the mortgage if you die during the term. A healthy non-smoker in their mid-30s typically pays from around €15–30 per month for €250k of cover; and most Cork homeowners locked in years ago save 30–50% by switching providers without changing cover. |

If you bought your home in Cork five, ten or fifteen years ago, there’s a strong chance you took out mortgage protection insurance Ireland at the same time; often the lender’s default policy, signed in the last week before drawdown, and never touched since. Premiums in the Irish market have moved significantly since then, and the same cover from the same insurer can cost meaningfully less today. This pillar guide explains exactly what mortgage protection in Ireland is, why it’s mandatory, how it differs from broader life insurance for mortgage Ireland plans, what the typical mortgage protection cost Ireland looks like in 2026, and how Cork homeowners can find the cheapest mortgage protection Cork providers are quoting right now. At Money Maximising Advisors, we review mortgage protection for clients across Cork and the rest of Ireland; the switch usually takes 15 minutes and saves real money.

| This article sits within our Protection hub and supports cluster pages our Cork clients visit most, including Mortgage Protection, Life Insurance, Serious Illness Cover, Income Protection and Mortgage Comparison Advice. |

The four numbers every Cork homeowner should sanity-check on their mortgage protection policy.

Quick answers: seven questions every Cork homeowner asks about mortgage protection

Is mortgage protection mandatory in Ireland?

Yes, the Consumer Credit Act 1995 requires anyone taking out a mortgage on their principal private residence in Ireland to have a mortgage protection policy in place at drawdown. There are limited exceptions (such as borrowers aged 50 or over, or where cover would be impossible to obtain), but for the vast majority of homeowners it is a legal requirement.

What is the difference between mortgage protection and life insurance?

Mortgage protection is decreasing-term; the cover shrinks alongside the falling mortgage balance and pays out only if you die during the mortgage term. Life insurance is level term; the cover stays the same throughout, and you choose the amount based on what your family needs, not just what the bank requires.

How much does mortgage protection cost in Ireland in 2026?

Indicative monthly premiums for a healthy non-smoker on a €250,000 policy over 30 years: around €15–30 per month at age 30, €20–40 at 35, and €30–60 at 40. Smokers typically pay 50–80% more. Joint policies (most common for couples) usually cost slightly less than two single policies. Existing health conditions, family medical history and term length all move the number.

Can I switch my mortgage protection policy without changing my mortgage?

Yes, mortgage protection is independent of the mortgage itself. You can switch insurer at any time without touching the loan. The new policy is assigned to the lender (as the old one was), and the lender simply updates its records. There is no impact on your mortgage rate, term or repayments. Most switches save 30–50% on premiums.

What is decreasing term insurance and why is it used for mortgages?

Decreasing term insurance is a life policy where the sum assured falls over time in line with a typical mortgage repayment schedule. Because the cover reduces as your debt reduces, premiums are cheaper than level-term life insurance of the same starting amount. That makes it the cheapest way to meet the lender’s requirement.

Should I add serious illness cover to my mortgage protection in Cork?

Adding serious illness cover mortgage Cork homeowners often regret skipping later; it pays a lump sum if you’re diagnosed with a specified serious illness (cancer, heart attack, stroke and many others), which can be used to clear or reduce the mortgage. It typically costs an additional €20–40 per month and is a genuinely useful addition for most working-age homeowners with dependants.

What’s the cheapest mortgage protection in Cork right now?

The cheapest mortgage protection Cork buyers can access changes regularly because Irish insurers reprice across their books quarterly. Royal London, Irish Life, Aviva, Zurich and New Ireland are the main active providers in Ireland in 2026; the cheapest provider for a 30-year-old non-smoker can be different from the cheapest for a 45-year-old smoker. We run live quotes across the full panel for every client at no cost.

Mortgage protection vs life insurance the right product for the right job

Two different products. Most Cork families should consider having both, not one or the other.

The confusion between mortgage protection vs life insurance Ireland homeowners face is among the most common we see in advice meetings. They’re not interchangeable ; they solve different problems.

Mortgage protection insurance Ireland exists to clear the mortgage debt if you die during the term. The cover decreases alongside the mortgage balance, the lender is named as the beneficiary, and the pay-out covers the lender first; it doesn’t leave your family any cash to live on beyond having a debt-free home.

Life insurance for mortgage Ireland homeowners take alongside the mortgage protection is a separate level-term (or whole-of-life) policy. The cover stays the same throughout, you choose the amount and the beneficiary, and the pay-out goes to your family directly. It is what replaces lost income, pays for childcare and education, and buys the family time to grieve without selling the house.

For Cork families with young children, our standard recommendation is both products in combination: mortgage protection at the level the lender requires, plus a separate Life Insurance policy at a level chosen to cover the family’s actual income needs. The combined cost is normally still less than €60 per month for a healthy couple in their 30s.

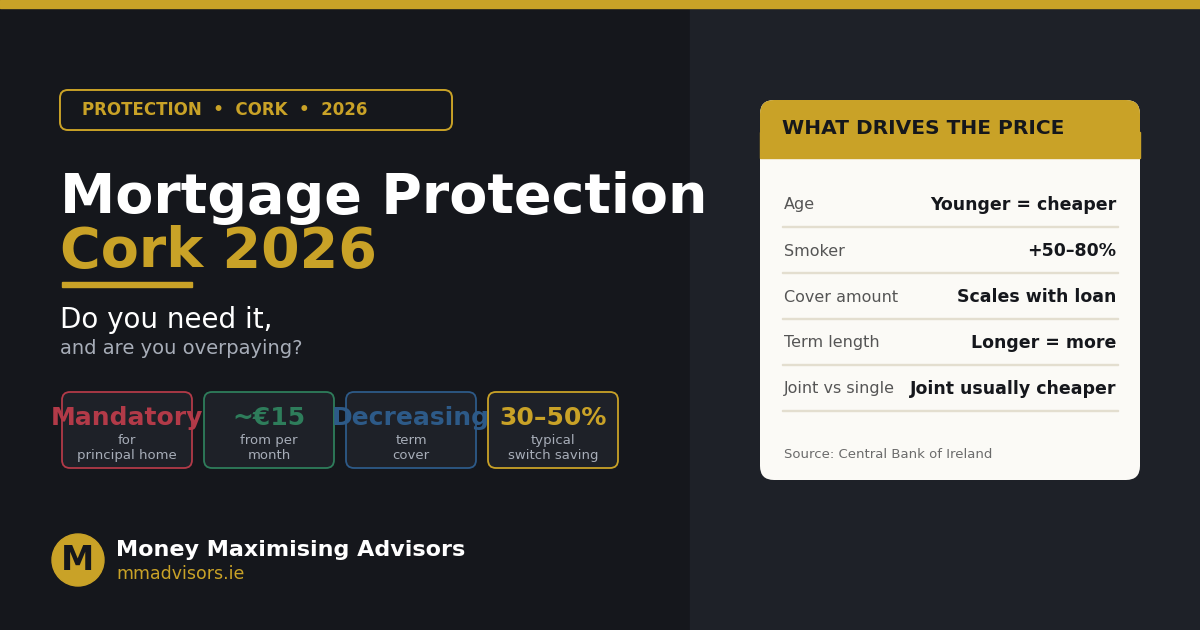

What drives your mortgage protection premium

Six factors that move your monthly cost up or down — some you can’t change, but some you absolutely can.

Age — the biggest single factor

Every year you wait costs you noticeably more. A 30-year-old can lock in a 30-year term at a price a 40-year-old can no longer access. If you’re weighing it up, get a quote now, you can always cancel within the cooling-off period if you change your mind.

Smoker status

Smokers pay around 50–80% more than non-smokers on otherwise identical cover. Insurers re-rate former smokers after 12 months tobacco-free. If you’ve stopped smoking for over a year, ask for a fresh quote, the savings are usually substantial.

Health history

Pre-existing conditions (diabetes, high blood pressure, mental health treatment, family history of heart disease or cancer) can drive the premium up or trigger specific exclusions. Honest disclosure at application is non-negotiable, mis-stated medical history is the single most common reason a claim is contested years later.

Cover amount and term length

Premiums scale roughly linearly with the cover amount and rise modestly with term length. A 30-year term costs only marginally more per month than a 25-year term on the same cover; it’s often worth taking the longer term to give yourself more flexibility.

Joint vs single life basis

Most couples take a “joint life, first death” policy; the cover pays out on the first death, then ends. It is normally cheaper than two single policies, but it only pays out once. For couples with significant cover needs, two separate single-life policies can sometimes work better, particularly where one earner has dependants from a previous relationship.

| Want a 15-minute mortgage protection review for your Cork home? Book Now for a free quote comparison across all the main Irish insurers, or Enquire Now and we will be in touch within one working day. |

Are you overpaying? How to check and switch

Three signs that you’re probably overpaying on your Cork mortgage protection:

- Your policy is more than three years old. Pricing has moved across the Irish market since you signed up.

- It was the lender’s default policy at drawdown. Lender-arranged cover is rarely the cheapest in the market.

- You’ve stopped smoking for 12+ months. Your premium hasn’t reflected that until you re-quote.

The switching process itself is straightforward and takes about two weeks end-to-end:

- 1. Quote comparison. We run quotes across all main Irish insurers using your exact age, cover, term and health history.

- 2. Application. Complete the new application; the insurer may ask for a short telephone health interview or a GP report depending on disclosures.

- 3. Approval and assignment. Once approved, the new policy is assigned to your lender.

- 4. Cancel the old policy. Only after the new one is fully in force — never leave yourself uncovered, even for a day.

Why work with Money Maximising Advisors on mortgage protection?

| About Money Maximising Advisors Limited is a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland. We hold Multi-Agency Intermediary status across all of the main Irish life insurers; Irish Life, Royal London, Aviva, Zurich and New Ireland; which means we can quote and compare across the full panel rather than push a single provider’s product. Our advisors hold QFA, RPA and FA qualifications and review mortgage protection alongside the wider family protection picture (life insurance, serious illness cover, income protection).Every recommendation we make is documented in a written Statement of Suitability, our regulatory standard. To learn more, visit about us. |

Common mortgage protection mistakes Cork homeowners make

- Taking the lender’s default policy. Convenient at drawdown, almost always more expensive than the open market.

- Setting the term too short. Match the term to your mortgage term — if you extend or top up the mortgage later, you’ll need more cover.

- Skipping serious illness cover. The lump sum on diagnosis can be transformational — most homeowners under-insure here.

- Forgetting to update after major life events. Marriage, divorce, new children, switching mortgages, paying off lump sums — all worth a 15-minute policy review.

- Cancelling the old policy before the new one is in force. Even one day of gap can leave you in breach of the Consumer Credit Act and exposed.

Most-read protection guides

- Mortgage Protection Ireland: A Complete Homeowner Guide

- Serious Illness Cover Ireland: What’s Covered, What’s Not

- Income Protection Ireland: The Cover Most Workers Forget

Frequently asked questions about mortgage protection in Ireland

Can I be turned down for mortgage protection in Ireland?

Yes, insurers can decline cover on medical grounds, or offer cover with exclusions or loadings. If you’re declined, the Consumer Credit Act exempts you from the mandatory requirement, though you may need written evidence of the decline and the lender’s discretion to proceed.

Do I need mortgage protection on a buy-to-let in Ireland?

No, the Consumer Credit Act requirement applies only to mortgages on your principal private residence, not investment properties. Many BTL investors still take out cover voluntarily to ensure the loan is cleared on death, but it’s optional, not mandatory.

Does mortgage protection cover redundancy or income loss?

No, mortgage protection pays out only on death (and sometimes terminal illness). To protect against redundancy or long-term illness keeping you out of work, you need separate Income Protection cover.

Can I keep my old policy even if I switch mortgage lenders?

Yes, your mortgage protection is between you and the insurer, not the lender. If you switch mortgage, the existing policy is simply reassigned to the new lender (a quick administrative step). You only need a new policy if the cover amount or term needs to change.

Does mortgage protection cover suicide?

Most Irish mortgage protection policies exclude suicide within the first 12 or 24 months of cover, then cover it as normal thereafter. The specific period varies by insurer; we flag the exact wording for any client on review.

Ready for a 15-minute mortgage protection review?

Whether you’re taking out cover for the first time on a Cork home or you suspect you’re overpaying on an existing policy, our team will run live quotes across the full Irish insurer panel and walk you through the right level of cover for your family. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

WARNING: If you do not keep up the payments on your mortgage protection policy, your cover will lapse and the lender may require you to take out a replacement policy.

Premium ranges, mandatory cover requirements (Consumer Credit Act 1995) and Central Bank Consumer Protection Code provisions referenced in this article are correct as at June 2026. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland and operates as a Multi-Agency Intermediary across the main Irish life insurers. This article is for general information only and does not constitute financial, tax or legal advice. Insurer underwriting decisions depend on individual circumstances. You should seek personalised advice from a Qualified Financial Advisor before purchasing, switching or cancelling any protection policy.