| Quick answer An equity release mortgage Ireland; also called a lifetime mortgage lets homeowners aged 60+ unlock tax-free cash from their home without selling it. You typically release up to 30% of the property value (depending on age), the rate is fixed at 6.95%, no monthly repayments are required, and the No Negative Equity Guarantee means your estate never owes more than the home is worth. Spry Finance is currently the sole provider in the Irish market. |

For Irish homeowners in their 60s and 70s sitting on a substantially appreciated property, home equity release Ireland has become a serious financial planning tool; whether to help a child onto the property ladder, fund a long-overdue retrofit, supplement pension income or simply enjoy retirement without selling the family home. This pillar guide explains exactly how an equity release Ireland arrangement works in 2026, who qualifies, how much you can release equity from house Ireland lenders allow, what an equity release calculator Ireland actually estimates, and the safeguards that protect you and your family. At Money Maximising Advisors, we work with clients across Ireland on Equity Release Mortgages as part of broader retirement-income planning.

| This article sits within our Mortgages hub and supports the cluster pages our later-life clients use most, including Retirement Planning Advice, Approved Retirement Funds (ARF), Inheritance Tax Advice, Small Gift Exemption Savings Plan and Section 72 Policies. |

The four parameters that define every Irish Lifetime Mortgage in 2026.

Quick answers: six questions every Irish equity-release customer asks

What is equity release in Ireland?

Equity release is a way for homeowners aged 60 or over to convert some of the value of their home into cash without selling or moving. The most common form in Ireland is a lifetime mortgage Ireland, where you take a lump sum (or staged drawdowns) secured against the home. No monthly repayments are required; interest rolls up onto the loan balance, which is repaid when the home is eventually sold or after the borrower’s death.

How does a lifetime mortgage work in Ireland?

You borrow a lump sum against your home at a fixed interest rate. The interest is added to the loan each year (compounded monthly) rather than repaid monthly. The loan plus accumulated interest is repaid when the house is sold, normally either when you move into long-term care or after you pass away. You continue to own and live in the home throughout.

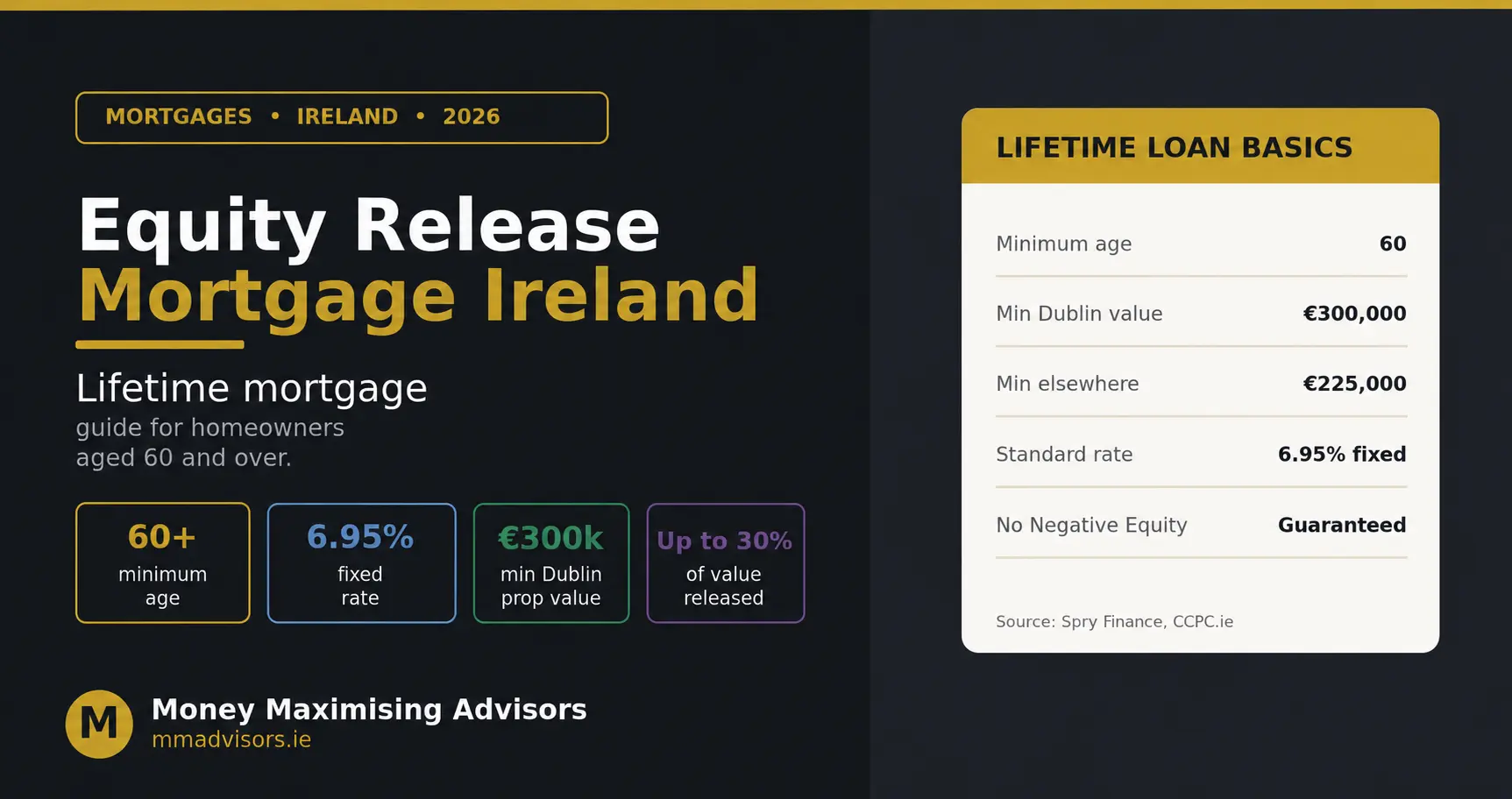

What is the minimum age for equity release in Ireland?

You (or the younger borrower if applying jointly) must be at least 60 years old. Spry Finance, currently the sole provider of full Lifetime Mortgages in Ireland, applies this 60-year minimum, and the property must be of standard construction and located in the Republic of Ireland.

How much equity can I release from my home in Ireland?

Generally between 15% and 30% of the property’s value, depending on age. A 60-year-old can typically release around 15%; an 80-year-old can release closer to 30%. The property must be worth at least €300,000 in Dublin or €225,000 elsewhere in Ireland.

What are the current equity release rates in Ireland 2026?

The headline lifetime mortgage rate is 6.95% fixed for the life of the loan. A lower green rate of around 6.50% is available for homes that meet specific energy-efficiency criteria. The rate is fixed at drawdown and does not move with the broader rate market.

Will my family inherit a debt with equity release?

No. Every Spry Lifetime Mortgage carries a No Negative Equity Guarantee; your estate will never have to repay more than the net sale proceeds of the home, even if the rolled-up loan balance exceeds the eventual sale price. Any equity remaining after the loan is repaid passes to your heirs as normal.

How much can you release? — by age

Indicative loan-to-value bands by age — older borrowers can release a larger share of the property’s value.

The loan-to-value (LTV) you can access on a home equity release Ireland product rises with age. The maths reflects lender expectations of how long interest will roll up before the loan is repaid; a 60-year-old has more years of potential compounding ahead of them than an 80-year-old, so the starting LTV is conservatively lower. For joint applications, the lender works to the younger of the two borrowers’ ages.

As a rough rule of thumb on a €500,000 Irish family home: a 60-year-old might release around €75,000; a 70-year-old around €110,000; an 80-year-old up to €150,000. An equity release calculator Ireland will refine the number for your specific age, joint-borrower position and property valuation.

How interest rolls up over time

Compounding interest on a €100,000 loan at 6.95% fixed — plan for the long view.

This is the single most important thing to understand about a lifetime mortgage Ireland. You do not make monthly repayments, so the interest is added to the loan each month and itself accrues interest the following month. At a 6.95% fixed rate, the loan roughly doubles every ten years. A €100,000 lifetime loan today becomes around €197,000 in ten years, and roughly €275,000 in fifteen. The trade-off is that you have access to that money today, when you can use it, without monthly outgoings.

Two features soften the compounding. First, the No Negative Equity Guarantee means your estate is never on the hook for more than the property is worth. Second, you can make optional voluntary repayments of up to 10% of the original loan amount each year, with no early repayment charge, if you do want to slow or reverse the growth.

| Considering equity release? We will walk you and your family through the numbers together. Book Now for a free consultation, or Enquire Now and we will be in touch within one working day. |

Equity release vs alternative ways to free up cash

Equity release is not the only way to access the wealth tied up in your home. Before deciding, it is worth weighing the alternatives:

- Downsizing. Selling the family home and buying something smaller frees up cash without taking on debt. The trade-off is upheaval, transaction costs and emotional attachment to the existing home.

- Standard mortgage top-up (under 60). If you are under 60 and still have an income, a standard top-up mortgage is often cheaper than equity release. Once you cross into your 60s, lender appetite for standard mortgages drops sharply.

- Drawing more from your pension. Increasing ARF drawdown or taking an additional tax-free lump sum from a private pension can be cheaper than rolled-up interest at 6.95%. We model this in any Retirement Planning Advice review.

- Section 72 policy. If the goal is helping children with a deposit but preserving inheritance value, a Section 72 Policy alongside lifetime gifting can sometimes work better than equity release.

Tax, inheritance and family considerations

Cash you take out of a lifetime mortgage is tax-free in your hands; it is your own equity, returned to you. Where it becomes interesting is when you use the released funds to gift money to family. Properly structured, gifts to children fall under the parent-to-child Group A CAT threshold of €400,000, and annual gifts of up to €3,000 per recipient sit outside the threshold entirely under the Small Gift Exemption. Done well, equity release can move family wealth across generations in a tax-efficient way.

Where caution is warranted: rolling up 6.95% interest reduces the eventual inheritance to your children, so the conversation needs to involve them. We recommend a family meeting before any application proceeds. Our Inheritance Tax Advice team can model the family-level numbers alongside the loan illustration.

Why work with Money Maximising Advisors on equity release?

| Money Maximising Advisors Limited is a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland. We take a whole-of-retirement view of equity release; looking at pension drawdown, inheritance tax, family gifting and protection alongside the loan itself, rather than selling the lifetime mortgage in isolation. Our advisors hold QFA, RPA and FA qualifications and walk every client (and ideally their adult children) through the long-term implications before any application is made.Every recommendation is documented in a written Statement of Suitability, our regulatory standard. To learn more, visit about us. |

Common equity release mistakes to avoid

- Treating the rate as low. 6.95% compounding doubles a balance every ten years; a serious decision, not a marginal one.

- Skipping the family conversation. Equity release reduces the eventual inheritance; your children deserve to be part of the discussion.

- Releasing more than needed. Take only what you actually need; you can usually draw down again later if the lender’s product permits.

- Ignoring voluntary repayments. 10% of the original loan amount can be repaid each year with no penalty; a powerful tool to slow compounding.

- Not exploring alternatives first. Downsizing, pension drawdown, or a Section 72 policy may achieve the same goal at lower long-term cost.

Most-read later-life mortgage guides

- Equity Release in Ireland: What You Need to Know

- Can You Release Equity on a Buy-to-Let Mortgage in Ireland?

- How to Remortgage to Release Equity from Your Property

- Pay Off Your Mortgage — Do You Immediately Have Equity?

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

Frequently asked questions about equity release in Ireland

Do I still own my home if I take out a lifetime mortgage?

Yes; you remain the legal owner of the property throughout. The lender places a charge against the home (similar to a standard mortgage), but ownership stays with you and your spouse or partner.

Can I move house after taking out a lifetime mortgage?

Yes; most lifetime mortgages are portable, meaning you can transfer the loan to a new property provided it meets the lender’s criteria. If you downsize significantly, you may need to repay a portion of the loan.

What happens to the loan when I die or move into long-term care?

The property is normally sold, the loan plus accumulated interest is repaid from the proceeds, and any remaining equity passes to your estate. The lender typically allows 12 months from the borrower’s death for the property to be sold.

Does equity release affect my State Pension or other benefits?

The State Pension (Contributory) is not means-tested, so it is not affected. Means-tested benefits such as the Non-Contributory pension or Fair Deal can be affected if the released funds remain in your bank account as countable savings; take advice on the means-test implications before drawing down.

What are the fees involved in arranging equity release?

Typical upfront costs include a lender set-up fee of around €1,500 (which includes a property valuation fee), and solicitor fees of €1,350–€2,500 depending on the firm used. Where a Central Bank-regulated broker has an appointment with the lender, the broker’s fee is typically covered by the lender.

Ready to explore equity release?

Whether you are weighing equity release for the first time or comparing it against other retirement-income options, our team will walk you and your family through the full picture; the loan structure, the long-term cost, the alternatives, and how it fits with your pension and inheritance plan. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: A Lifetime Mortgage will reduce the value of your estate.

Interest rates, loan-to-value bands and product features referenced in this article relate to Spry Finance’s Lifetime Mortgage as at June 2026. Rates and terms can change. The illustrative APR on a €75,000 loan over an assumed 15-year term at 6.95% fixed is 7.33% per annum (source: Spry Finance). A Lifetime Mortgage involves the compounding of interest; your loan balance will grow over time. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. You should seek personalised advice from a Qualified Financial Advisor before considering equity release.