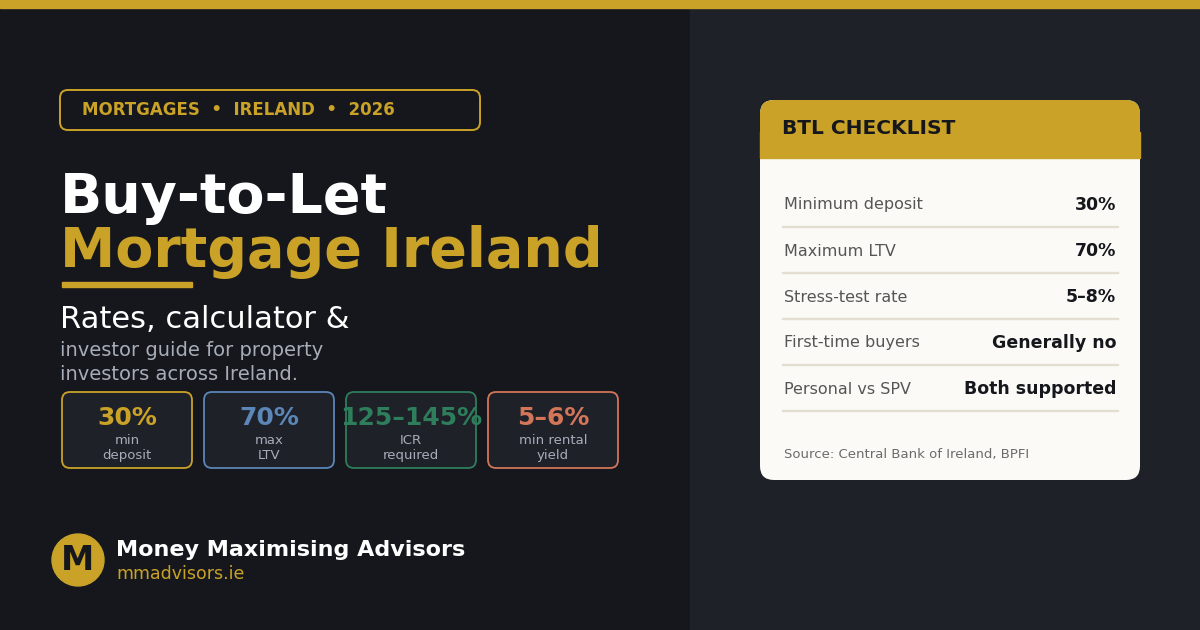

| Quick answer A buy to let mortgage Ireland requires at least a 30% deposit (70% LTV cap) under Central Bank rules. Lenders typically expect a rental yield of 5–6%, an interest coverage ratio (ICR) of 125–145%, and the loan must pass a stress test at 5–8%. First-time buyers generally do not qualify, and you can apply in your personal name or through an SPV — we cover both routes below. |

If you are weighing up an investment property mortgage Ireland in 2026 whether your first BTL or a fifth one for the portfolio, the rules of the road are sharper than they look from the outside. This pillar guide walks you through exactly how a BTL mortgage Ireland is calculated, the deposit and rental-yield bar you need to clear, an honest view of the best buy to let mortgage rates Ireland currently offers, and how to use a buy to let mortgage Ireland calculator the way an actual underwriter does. At Money Maximising Advisors, we arrange BTL mortgages for landlords across Dublin, Galway, Cork and every county in between.

| This article sits within our Mortgages hub and supports the cluster pages our investor clients visit most, including Buy-to-let Mortgages, SPV Mortgages, Mortgage Comparison Advice, Equity Release Mortgages and Public Sector Mortgages. |

The four parameters that decide every Irish BTL mortgage application in 2026.

Quick answers: the six questions every Irish BTL investor asks

What is the minimum deposit for a buy to let mortgage in Ireland?

The Central Bank of Ireland caps BTL lending at 70% loan-to-value (LTV), which means you need a minimum 30% deposit. Some lenders ask for slightly more for non-standard property types or first-time landlords.

Can first-time buyers get a buy to let mortgage in Ireland?

Generally, no. Almost all Irish lenders require you to already own (or have owned) your principal private residence before approving a BTL mortgage. A small handful of specialist lenders consider exceptions, but the strong default is that first-time buyers should buy their own home first. We can map your specific options as part of a free consultation.

How much can I borrow on a buy to let mortgage Ireland?

Borrowing is driven by rental income, not personal income alone. Lenders run three checks: (1) rental yield must be at least 5–6%, (2) the rent must cover the mortgage payment by an interest coverage ratio of 125–145%, and (3) the loan must stress-test at 5–8%. Pass all three and you can borrow up to 70% of the property value.

What are the current buy to let mortgage rates in Ireland?

BTL mortgage rates in Ireland in 2026 typically sit a notch above standard residential rates because of the higher risk profile. Pricing changes regularly across lenders, we benchmark the live market for every client through our Mortgage Comparison Advice service rather than publish a snapshot that ages within weeks.

Is buy to let property still a good investment in Ireland in 2026?

Irish rental demand remains strong, particularly in Dublin, Galway, Cork and the larger commuter towns, with vacancy rates close to historic lows. That said, BTL is no longer the easy yield play it was a decade ago: higher rates, RTB regulation, increased tax compliance and a 30% deposit have raised the entry bar. For investors with the deposit and a long-term horizon, it can still produce strong total returns when held in the right structure.

What income is required for a buy to let mortgage in Ireland?

There is no specific loan-to-income (LTI) cap for BTL under Central Bank rules, affordability is driven by rental income rather than personal income. That said, individual lenders set their own minimums; Bank of Ireland, for example, will lend up to 3.5× personal income with terms up to 30 years on BTL. Most lenders also expect to see a stable personal income (often €40,000–€50,000+) and a clean credit history before approving you.

How a buy to let mortgage Ireland calculator actually works

Any honest buy to let mortgage Ireland calculator needs to run three sequential checks, the same ones an underwriter applies. We work them through below with a worked example on a €300,000 investment property:

Step 1 — Rental yield check

Divide the achievable annual rent by the purchase price. On a €300,000 property letting at €1,500 a month, that is €18,000 / €300,000 = 6.0%. Most lenders want at least 5–6%; below that, the application generally does not progress.

Step 2 — Stress-test affordability

The lender re-runs your monthly mortgage payment at a higher “stressed” rate (typically the actual rate plus around 2%, often landing at 5–8%). You must still pass affordability at the higher rate, not just the current headline rate.

Step 3 — Interest coverage ratio (ICR)

Divide the gross monthly rent by the stressed monthly mortgage payment. The result must be at least 125% (and 145% for many lenders pricing higher-rate taxpayers or SPVs). If the rent does not cover the payment by this margin, the lender cuts the loan amount until it does.

The simplest way to use these in practice is to walk through them with our Mortgage Comparison Advice team we will run the numbers for your specific target property across multiple lenders in a single call.

Best buy to let mortgage rates in Ireland 2026

Live BTL pricing in Ireland in 2026 changes week to week. The best buy to let mortgage rates Ireland lenders offer right now will almost always come with conditions a higher deposit (some lenders price more keenly at 65% LTV), a fixed-rate term of three to five years, evidence of stable employment alongside the rental income, and a clean two-year personal credit history.

Rather than publish a rate table that goes out of date the moment a lender repositions, we keep a live internal benchmark across the main active BTL lenders including Bank of Ireland, AIB, ICS Mortgages and the specialist BTL providers and run the live comparison live for each client. Our recent blog

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords tracks the latest entrants and their pricing.

| Want a live BTL rate comparison for your specific scenario? Book Now for a free 30-minute consultation, or Enquire Now and one of our advisors will be in touch within one working day. |

Personal name or SPV: two ways to hold an investment property

Personal ownership vs limited-company SPV the right structure depends on tax bracket and portfolio scale.

For a first or second property, personal ownership is usually the right answer. The setup is simpler, lender choice is wider, and the deposit and rate terms are easier to access. Rental profit is taxed at your marginal income tax rate plus USC and PRSI punishing for higher-rate taxpayers, manageable for lower-rate ones.

For higher-rate taxpayers or anyone building a portfolio of two or more properties, an SPV (Special Purpose Vehicle), a limited company incorporated specifically to hold property often makes more sense. Profits stay inside the company at a lower corporation-tax rate, can be reinvested without leakage, and the structure is friendlier to scale. The trade-off is more setup complexity, a narrower lender pool and a small rate premium. We cover the full structure decision in our dedicated SPV pillar.

Why work with Money Maximising Advisors on your BTL mortgage?

| About Money Maximising Advisors Limited is a Qualified Financial Advisor (QFA) firm regulated by the Central Bank of Ireland. We work with property investors across Ireland from first-time landlords in Galway to portfolio investors in Dublin and Cork sourcing the right BTL mortgage product from a panel of active Irish lenders. Our advisors hold QFA, RPA and FA qualifications and stay current with Central Bank lending rules, Revenue tax updates and lender criteria changes.Every recommendation is documented in a written Statement of Suitability, our regulatory standard. To learn more, visit about us. |

Common BTL mistakes Irish investors make

- Treating BTL as passive income. RTB registration, tax filings and tenant management all take work budget for it.

- Buying the cheapest property regardless of yield. A €180,000 property at 4% yield will fail an ICR check that a €300,000 property at 6% would pass.

- Going variable just because the headline rate is lower. BTL stress-test rates are punishing, fixed rates often unlock more loan capacity.

- Ignoring the structure decision. Personal vs SPV makes a material difference once you hold two or more properties.

- No protection in place. Lenders will insist on Mortgage Protection at drawdown, arrange it early, not the week before signing.

Most-read mortgage guides

- New Buy-to-Let Lender in Ireland: Lower Rates for Experienced Landlords

- Can You Release Equity on a Buy-to-Let Mortgage in Ireland?

- Irish Mortgage Market 2026: Rates, Rules, and What’s Changed

- How to Choose the Best Mortgage Lender in Ireland

Frequently asked questions about BTL mortgages in Ireland

1. Can I switch my current home into a buy to let mortgage if I move out?

Yes, this is called a “consent to let” arrangement or, more commonly, a switch to a formal BTL mortgage. You will need to notify your existing lender, who may require you to refinance at BTL rates with the appropriate 30% equity in the property.

2. Are buy to let mortgages available with interest-only repayments?

Some Irish lenders offer interest-only BTL options for part of the term, particularly to experienced landlords or for portfolio cases. The full term will typically include a repayment phase, and you must show a credible plan for the capital. We model both options for clients during the comparison stage.

3. Do I need to register with the RTB before drawdown?

Yes, every Irish residential tenancy must be registered with the Residential Tenancies Board (RTB) within one month of the start date. Your solicitor will typically coordinate this around closing.

4. How long does it take to arrange a BTL mortgage in Ireland?

Approval in Principle within a week is realistic with the right paperwork in place. From AIP to drawdown usually takes another 6–10 weeks, depending on the lender, the valuation and conveyancing speed.

5. Can a couple apply jointly for an Irish BTL mortgage?

Yes, joint applications are common and often help with affordability. Both applicants must usually already own (or have owned) a principal private residence.

Ready to talk to a Buy-to-Let mortgage broker?

Whether you are sizing up your first investment property or your fifth, our team will run the numbers across active Irish BTL lenders, structure the application properly (personal or SPV), and shepherd the application end-to-end. Book Now for a free consultation, or visit Money Maximising Advisors to learn more.

Important information

WARNING: Your home is at risk if you do not keep up payments on a mortgage or any other loan secured on it.

WARNING: You may have to pay charges if you pay off a fixed-rate loan early.

Buy-to-let lending rules, LTV caps, ICR requirements and rates referenced in this article are correct as at June 2026 and are sourced from Central Bank of Ireland, BPFI and Bank of Ireland public lending criteria. Money Maximising Advisors Limited is regulated by the Central Bank of Ireland. This article is for general information only and does not constitute financial, tax or legal advice. Lending criteria, terms and conditions apply. You should seek personalised advice from a Qualified Financial Advisor before making any financial decision.